Most people are minimally impacted by Obamacare as they already get their insurance through an employer, through the government or have solid individual coverage. The next largest group of Americans are impacted by Obamacare as they’ll be gaining access to coverage. They’re better off. Then there are two small groups. The first is a group who has decent individual coverage but may or may not be better off with the improved coverage mandates of Obamacare. These situations will vary by individual income and thus subsidy status, state and health status. The other group are the clear losers of the policy changes. They have individual coverage that is being cancelled and Exchange coverage is more expensive.

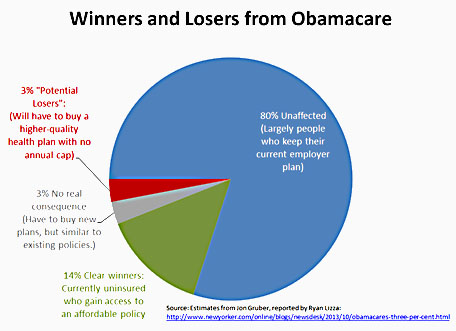

So what types of plans are in the “Potential Loser” bucket?

So what types of plans are in the “Potential Loser” bucket?

Let’s go back to a post on Premium Bullshit for a quick review:

Arkansas: $26 per month for a $25,000 deductible 23% applicants denied. 28% uprated.

Ohio: $25,000 deductible, 19% denied, 17% uprated.

Let’s look at a the Arkansas plan in some more detail, as we go to page four to see what is not covered. I’ll highlight some of the more unusual things that are not covered.

- Maternity coverage on the base plan.

- Maternity coverage or pre-natal care within the first twelve months of purchase of the maternity/pregnancy rider.

- Any pre-exisiting condition for an adult within the first twelve months of purchase

A similar plan on the same information sheet has additional limitations. The HSA plan does not cover mental health treatments or prescriptions.

This is an extreme example. The Ohio plan in the link above is similar in that it excludes maternity care and pre-exisiting conditions but it does cover mental health needs.

Individuals with these types of plans, or basically any individual product that is medically underwritten, excludes maternity care and has a deductible over $10,000 is almost guaranteed to face sticker price rate shock as these plans don’t even come close to meeting minimal Obamacare standards of insurance. If the person facing sticker price rate shock for a basic Bronze or a Catastrophic plan is making under 250% of Federal Poverty Line, they’ll probably break about even as they move into an Exchange Bronze or Exchange Catastrophic plan. If they make more than 250% FPL, they most likely are getting much better coverage (that they individually probably don’t need as they demonstrated no history of medical need) at a significantly higher post-subsidy price. And for the individuals in this bucket who make more than 400% FPL, they are guaranteed to face rate shock.

agrippa

That breakdown is what I expected. It looks to me that the law was, first of all, intended to provide access to insurance for the uninsured.

I bet that the 3% ‘potential losers’ will end up with better insurance at a higher price.

greennotGreen

“(that they individually probably don’t need as they demonstrated no history of medical need)”

And I individually didn’t need my great insurance plan either as I had always been quite healthy…until I got cancer. It’s almost like saying you can just use a tarp for a roof since the wind doesn’t often blow hard. Sometimes it does.

Ahh says fywp

So these ‘unlucky’ ones are playing medical russian roulette, using tge medical tax exemption as a cap gains tax dodge, and whrn they do have a problem theyll belly up to the federal trough like Trent Lott & all of his rich neighbors snarfing up fema insurance.

Btw, I still don’t understand why federal disaster ins is a ‘ first shall stay first, last shall stay last program’.

David M

I’ll be paying a little more for coverage next year for my wife and I, both on individual HSA policies. She has a $2000 deductible and a $5000 max out of pocket and I have a $3500 deductible and the same $5k max out of pocket. Together we were paying $390/mo for coverage, and roughly equivalent plans on the exchange will cost about $465.

We’re not eligible for subsidies, and will not be using the maternity care, so there isn’t an immediate benefit to the exchange plans. Overall we’re much, much better off after the Obamacare reforms, but yes, my premiums are going up a little.

Anna in PDX

After reading Roy at Alicublog and now this, I feel like I have great talking points to counter all the crap about people’s rates going up. Gee you had crap insurance and now you are forced to have decent insurance and pay more. Sucks to be you. I hope nothing but the best for you but if something did go wrong with your health, you’d suddenly realize that paying more for better insurance was worth the extra costs.

David M

One thing to consider on the “rate shock” is whether the state allowed people to be denied coverage during underwriting and ran their own high risk pool for people that were denied coverage. For some healthy people that could make it through underwriting, I’d expect they had decent rates and really will be facing slightly higher premiums.

And not all of those people will have had “junk” insurance, even if it wasn’t ACA compliant. Of course the tradeoff for their lower rates in the past was excluding people that needed coverage from the individual market, so I’d argue those past rates were artificially low.

Guy

The “80% unaffected” group which includes me is unaffected only as long as we have our current jobs. I compared what COBRA would cost if I got laid off to ACA compliant plans offered by NC BCBS and found several that are significantly cheaper (higher deductible but otherwise similar benefits). I call that little extra peace of mind a win considering I am no longer young and in perfect health.

Citizen_X

@Anna in PDX: Plus, if they get all huffy about having to buy (better) insurance, you can go negative: “Hey, when people like you had to go to the Emergency Ward, my rates went up. Pay your way, ya freeloader!”

pseudonymous in nc

The whining from men about a standard package including maternity coverage is pretty telling.

“Risk pooling, what is it?”

These are people who basically want a dedicated risk pool for angry selfish white men, and would then complain that premiums rise on account of the abnormal prevalence of rage-induced aneurysms.

NobodySpecial

Eh, I’m not one of the 3%, I’m one of the 14% who just happens to be a bit cash strapped. If I wasn’t paying off a car loan, premiums wouldn’t be much of a problem….but I am for the next 18 to 24 months. Not to mention the Illinois plans that I’ve encountered on healthcare.gov are 90% of the ‘huge deductible, approaching out of pocket cap’ variety, which in essence means that actually taking care of my health problems will put me in the poor house just as quick as not having insurance, the only difference is how deep the hole is.

I’ve held off on signing up for a plan in favor of going into my local hospital (where all the networks will be going anyways) and getting some more expert advice before even thinking about signing up for a plan. Yeah, insurance is better than no insurance, and Obamacare* is miles beyond, say, Starbridge, but being two steps from impoverishment still sucks.

* – I know the current thinking is that calling it Obamacare is a perjorative, but I disagree. I love reminding rednecks exactly where their insurance will be coming from and whom they have to thank for it around their gritted tooth.

LanceThruster

I HATE buying 100 year flood insurance when I only plan to live to 99!

Anna in PDX

@Guy: Yes! I was thinking about all the COBRA horror stories I had heard from laid-off or retired-too-early-for-Medicare friend and former co-workers, and how much I worried about that as one of the main horrible consequences of being laid off – now I feel much less worried about that single aspect of it. Anything that decreases my anxiety is good. After all that is the whole idea of why have insurance at all.

FlipYrWhig

@Anna in PDX: I don’t understand why anyone would want to continue in a plan that consists of you paying money per month for jack squat, rather than one that consists of you paying somewhat more money per month for, like, actual insurance.

Mnemosyne

@David M:

It’s worth taking a look at the preventative screenings and medications that are now covered at no cost, especially if you’re getting up towards the age where they start wanting you to be screened for colon cancer etc. Not having to pay for those (even if it did go towards your deductible before) might help make up for the premium increase.

@NobodySpecial:

They probably have a healthcare navigator at the hospital, or can at least refer you to one. It looks like this state website may also be able to help with questions.

Mnemosyne

@FlipYrWhig:

I was saying down below that I think there is a not-insignificant number of people who’ve never had decent insurance, so they honestly don’t know what it’s supposed to look like. As Kay was pointing out, even major corporations have been offering their employees crappy rip-off insurance.

Once people figure out what it’s like to have real insurance that actually covers them when they’re sick, they’re never going to let it go, which is why conservatives are so desperate to prevent people from signing up.

Anna in PDX

@FlipYrWhig: I do understand this a little.

First there are people who are paying very little for very crappy health insurance because they have very little money, like “Nobody Special” above. That makes sense, and I am sorry that it will be difficult for them to be forced to pay more. (I totally hear that car payment thing. I am trying like heck to pay off my car right now because it has made my life that much more paycheck-to-paycheck.)

Second there are the people who have enough disposable income, but are used to *choosing* to pay very little for crap insurance because they are very healthy/young and this has worked out for them so far. I am not as sorry for them, because as others pointed out, assuming anything ever does happen to them, we insured people all pay for it because of their driving up the ER costs. They can be maybe reached by pointing out that they are socializing their risk to the rest of us, and this is just correcting the system so that they can’t do that. (As Citizen X pointed out above.)

FlipYrWhig

@Mnemosyne: Definitely. But then I think about things like this: what do these people do when they pick a cell phone plan? Do they just pick the cheapest one and then complain about overages every time, or do they eventually figure out that paying more per month might spare them from having to handle the overage drama?

kc

@pseudonymous in nc:

That is annoying. Do those dumb shits think they’re not already paying for maternity care, one way or another?

On the other hand, I’m one of those people who will actually have to buy insurance under the ACA (newly self-employed). Just tried to create an account on the website was unable to even do that, let alone shop for a plan. I thought after a month they’d have their shit together. I guess not.

kc

@NobodySpecial:

Eh, I’m not one of the 3%, I’m one of the 14% who just happens to be a bit cash strapped

I’ve detected a distinct lack of sympathy in certain quarters for people like that. The attitude seems to be “It’s Obamacare or the government trough, so suck it up and pay, you moocher!”

An odd approach to people we’re ostensibly trying to help.

FlipYrWhig

@Anna in PDX: Even so, if you just think about it as health care spending over a period of length X, the decision about what to pay for insurance each month is only a subset of that. If the insurance isn’t actually reducing your health care spending, you’re paying more in total, just on separate bills.

Ahh says fywp

Why do old men bitch abt maternity coverage? If it was the problem old ppl would be charged 1/3 of youngs, but its vice versa.

Mnemosyne

@kc:

Two possible ideas:

Try a different browser — as with so many things, it sounds like Microsoft Explorer is not compatible, so you may want to try Firefox or Chrome.

Create a new email address and try to create a fresh account with that.

The one persistent problem I’ve seen is that if people are naturalized citizens or permanent residents rather than natural-born citizens, there are a bunch more hoops that have to be jumped through and usually can only be solved with a phone call.

And I wouldn’t call the 14% “whiners.” I would encourage them to look at the list of preventative care that’s now included in the price — especially birth control — and work through the numbers since it’s entirely possible that they will be saving money in those areas. If you’re not having to pay $30 a month for birth control because it’s now included at no extra charge, you haven’t increased your expenses since you’re saving money somewhere else. I’m guessing that the immunization coverage is going to be a huge cost-saver for parents with young children, who won’t have to pay a doctor’s fee or copay every time.

ETA: Also, three, if you’re in a state that set up its own exchanges, go directly to their website rather than trying to go through Healthcare.gov first. Here in California, you can go straight to coveredca.com without having to navigate through healthcare.gov first, and our state website is working just fine, thankyewverymuch.

(Fixed Covered California website address)

Omnes Omnibus

@kc: It is quite possible that the amounts of subsidies and/or the income level at which they kick in will need to be adjusted.

Mnemosyne

@Omnes Omnibus:

There also seem to be some weird loopholes that are hitting unmarried couples with kids since only one of them can claim the kids but their household income may be more than they “should” have if they’re claiming to be a single parent.

FlipYrWhig

@Ahh says fywp: Old men are the last people who should be complaining about anything involving bills for medical treatments. All they do is go to the doctor for various ailments. Someone else is paying for that. By design. They’re making out like bandits! If we went all in on this come as you are approach, no one would ever want to insure an old dude, because they’re expensive as hell.

David M

@Mnemosyne:

My wife is probably coming out even or ahead on premiums, most of the increase is in mine. The equivalent policy costs $60 more a month, and has a slightly higher deductible and out of pocket max. If we were paying $390/mo this year, I’d expect to pay $430/mo next year for the same two policies while the ACA policies are $465/mo.

Again, we’re much better off after all the reforms are considered, my example was just to show that premium increases were possible for some people in the individual market.

I do think the examples of people where their insurance rates are going from $100 to $750 are complete BS, but the individual insurance market had over 10 million people, so some of them were probably getting a good deal before that is no longer available.

Mnemosyne

@David M:

I’m starting to think that those are examples of people being ripped off by their insurance companies under the guise of Obamacare made me do it! — the insurance companies are moving people to gold or even platinum plans that they may not need and claiming that they don’t have any choice … oh, and don’t look behind the curtain at Healthcare.gov because it won’t do any good.

kc

@Mnemosyne:

I’m going to give it another try on the weekend, if I can get in front of the computer long enough. If it doesn’t work then, I guess I’ll try a different browser.

I’m not too worried about it yet; I don’t have all my shit together wrt income, so I was just going to look around and get a general idea of what I’ll be paying.

I can see how this would be really aggravating to people, though.

kc

@Mnemosyne:

ETA: Also, three, if you’re in a state that set up its own exchanges, go directly to their website

Bwahahaha, no, I’m in South Carolina. My state’s general attitude towards the likes of me is “fuck off and die.”

Mnemosyne

@kc:

From what other people have said, the more private/anonymous you keep your browser (refusing all cookies, etc.), the more problems you’ll have with the website. So you may have to temporarily turn off a bunch of security stuff in order to get it to work.

Richard Mayhew

@FlipYrWhig: But the difference between good cell phone plan and good health insurance plan is the cell phone plan failings are easily visible to a high proportion of people who are stuck in a crappy plan and they can easily/reasonable margin increase in cost do something to change things.

For someone who is reasonably healthy/young and broke, most years they won’t need the good insurance plan while they need/strongly desire the good cell phone plan as they are reasonably healthy and young.

People suck at statistical thinking (that is the only thing that keeps me gainfully employed)… instead people adapt recency and social network biases plus a bit of directed wishful thinking that X got sick/$15,000 medical bill because they’re a bad person who did something to deserve it while I’m good…

Gex

@Anna in PDX: I have done that. In fact, I went so far as to ask a person complaining about the “tax” what they would prefer? Paying that tax and having access to emergency services OR having people die at the doors of ERs as the emergency room has to run the financials to make sure the person can pay for an unspecified amount of treatment once admitted. Because either the ERs make sure someone can pay or they pass the costs on to others if the patient can’t pay. And then I called that person a freeloader. And I concluded with, “It is amazing to watch conservatives get angry that Obamacare is asking people to pay for services they get rather than freeload off of taxpayers.”

Gex

And a pox on those who have been demanding that birth control not be covered and then go on to complain about maternity coverage. Women and children can just FOAD I guess. Can you feel the family values?

azlib

The rate shock is really comparing apples and oranges. It is like leasing a YUgo and then getting a notice that the Yugo is no longer available and the leasing company is offering you a lease on a Chevy Cruz. It costs more, but you are getting a much better car that meets the current safety standards and may actually protect you in a crash and save your life!

Patricia Kayden

@kc: I thought you could also call a phone number to enroll through the ACA as well since the website is still screwed up.

catclub

@LanceThruster: Of course, when we had three or so 1 in 500 year floods in the region, i decided that the flood insurance might pay for itself.

Mnemosyne

@azlib:

Actually, I think the insurance companies are up to their old tricks and telling their customers that since their Yugo is no longer available, the insurance company is forced — forced, I tell you! — to put them into a Mercedes they don’t want or need, and some percentage of those customers will believe them and not go to the exchanges, where they would discover that they can afford the Chevy Cruze coverage.

Shorter me: I call shenanigans, but the media isn’t reporting that part of the story (except Michael Hiltzik in the LA Times).

FlipYrWhig

@Richard Mayhew: Good point. I suppose insurance is a weird product anyway, in that your fondest wish is for all the money to be completely wasted: if you could never get sick and live forever, you’d be giving up a cut of your income for nothing all that time too. No one says, “Woohoo! Insurance, baby! I’m going out to get injured and sick TONIGHT!”

The Raven on the Hill

My guess is that the people who are being heard on this are relatively healthy people 50-65 years old, making a bit too much money for a subsidy but squeaking by, and discovering that the new plans available cost from an eighth to a quarter of their income.

The subsidy shuts off at too low an income level for people over 50.

Now, these aren’t the people hurt worst by the ACA implementation–those are working poor with incomes at 100-133% of FPL in states that have not implemented the Medicaid expansion. (There’s a million people in Texas who are going to be left out in the cold by the failure to expand Medicaid.) They aren’t even the group that’s hurt second worst; that would be the people who are just over 133% FPL who can barely make ends meet as it is and for whom even subsidized coverage is going to hurt–will probably make some of them homeless. But the group I mentioned in my first paragraph is middle class and predominantly white, and they get airtime.

The unambiguous winners of the system ordered by the PPACA are the health insurance companies, big pharma, and the medical device manufacturers. The rest of us, some are winners, some are losers.

And when the next elections come around, we know who’s going to be angry. Thanks, Obama.

Stella B

My flu vaccine was free this year. Our COBRA payment is $0-$400 more than available O’care plans. Since we are quite comfortable, I’m trying to convince the spouse that we should sign up for Bronze and pocket the extra. That would be nearly $5000 per year. Damn that Obama! That’s a lot of money to spend! We are 54 and 55.

Stella B

@FlipYrWhig: I’m quite happy when I think about all the tax money I’ve “wasted” on the fire department, the police department, and homeowner’s insurance, too

David M

@Mnemosyne:

I also agree the insurance companies are trying to take advantage of their existing customers. My current insurance company isn’t on the exchange and the increase they quoted me was from $390/mo to $575/mo. And I do consider the two ACA compliant plans they offered me to be substantially worse than the plans I’m on now, we’re talking significant increases in both the deductible and max out of pocket costs.

So based on the letter, I would have been majorly ripped off if I did nothing. Going to the exchange made things much more tolerable. Thankfully the Washington State exchange is working.

The Raven on the Hill

@Stella B: Beware of windfalls that will take you off the subsidy. When you cross that line, your insurance costs shoot up hugely. (And the IRS will want its money back.)

Beyond that, if you are 54 and 55, you’re probably better off going for a silver plan; it’s likely when you add up your medical expenses for the year the very high coinsurance rates will eat up any premium savings.

Upper West

From someone at a small firm to me:

Our group plan was terminated. Under the new plan, I will go from $868 out of pocket per mo. to $1070 per mo. Plus a $5700 deductible I didn’t have before. The insurance consultant I spoke with said that as a result of ACA, approx. 2/3 of small employer plans would be voided by the end of the year.

This sounds fishy — is it really related to the ACA? Is it because of the delay of the mandate?

BillinGlendaleCA

@Mnemosyne: I saw Hiltzik on Tweety yesterday, he’s doing good reporting on this(I remember his name from when I used to take the Times). On your earlier point on birth control, just a quibble. I’m not sure where you could get birth control for $30, the kid was looking at least $70 before her VA benefits started.

The Raven on the Hill

@Upper West: has your contact checked out the exchange yet?

Stella B

@The Raven on the Hill: we’re very, very far from ever qualifying for a subsidy and I couldn’t be happier about that either.

Stella B

@Upper West: that sounds fishy to me, too. Here’s what someone in the industry says:

http://theincidentaleconomist.com/wordpress/where-is-the-outrage-over-employer-sponsored-coverage-in-the-rate-shock-debate/#comment-89999

Matt McIrvin

@Mnemosyne:

The website problems (and publicity for same) made it much easier to do that, of course. People are probably assuming they won’t even be able to check prices, maybe even in states that don’t use the federal website.

Matt McIrvin

@Stella B: Oh, man, check out the comment from “Jimbino” there.

And then he goes on to recommend the Rush Limbaugh loophole.

Which, apparently, actually exists… sort of. If you can arrange to never have the IRS owe you money ever again in your life, and the government doesn’t bother to sue you.

schrodinger's cat

OT Does anyone who has a WP blog know how to stop someone from following your blog.

Anna in PDX

@FlipYrWhig: Exactly. What we are paying for is peace of mind. I feel that is worth a lot. This is why I think people in higher-tax countries that have more security regarding health, retirement, etc. are better off than I am even if I have more disposable income. They just don’t have the risks that I obsess about.

cleek

@schrodinger’s cat:

in what sense?

if you can find a user’s IP address and you are running WP on a host of your own (ie. not on wordpress.com) you can use cPanel to block that IP address. (assuming your host uses cPanel, or some equivalent admin interface). that would make the site inaccessible to anyone using that IP address.

i don’t think there’s anything in WP itself to ban by IP, though.

or, if you want to block someone from being able to follow a link from a given site to your blog, you can block by referrer.

Monala

@Mnemosyne: That shouldn’t matter. I have been told that subsidies are allotted based on what you declare on your tax return. So if you are an unmarried couple and only one of you claims the kids on your tax return, that parent is the one that applies for the benefits.

This means that an unmarried couple doesn’t need to include the entire household income, since they are most likely filing separate tax returns, each with their own income on it. (The only case in which they wouldn’t might be where one of the parents has no income and is declared a dependent on the other’s tax return. But then the question is moot – there’s only one income anyway). So the parent applying for benefits for him/herself or the kids only needs to include their own income.

kc

@Patricia Kayden:

You can; the website gives an 800 number. I didn’t want to do that b/c I didn’t want to tie up the phone for a long time AND I’m not ready to enroll yet. When I am ready and if I still can’t get through on the website, I’ll do that.

kc

@The Raven on the Hill:

Beware of windfalls that will take you off the subsidy. When you cross that line, your insurance costs shoot up hugely. (And the IRS will want its money back.)

That’s a bit perturbing for the self-employed.

David M

@kc:

Plan to collect the subsidies when you file your tax return then…

Mnemosyne

@Monala:

If that’s the case, I’m not sure that’s been clear to most people, though maybe it’s made more clear on the website. I know there were people here who were freaked out because their boyfriend/girlfriend’s income was part of the “household” income on the estimation sites, and that income was putting people over the top for being eligible for a subsidy.

Upper West

@The Raven on the Hill: It’s a group plan, so I don’t think the exchanges apply.

Mnemosyne

@Upper West:

IIRC, you can opt out of your employer’s insurance and go to the exchanges if it doesn’t meet PPACA standards for things like percentage of income. I know I got a letter from the Giant Evil Corporation I work for informing me of my right to do that. It was pretty much the only way to prevent companies from continuing to screw their employees with inadequate plans.

Monala

@Monala: OK, I thought of one situation where unmarried couples with kids could be hampered. Person A and Person B are an unmarried couple. Let’s say they have two kids. Person A has the higher income, but Person B declares the kids as dependents on B’s tax return for whatever reason (maybe they are Person B’s kids by a previous relationship).

Person A needs health insurance and goes to the exchanges. Person A has to enter A’s income as the income for a single person household, since A doesn’t declare the kids on A’s tax return – even though Person A and Person B share household expenses and Person A’s income is really helping to support a household of 4.

Monala

@Mnemosyne: IIRC, the estimation sites just asked general questions about household income, not specifying anything. The actual exchange web sites get more in-depth about who is actually declared on one’s tax return.

I was told that the people who need to be aware of this are those who share custody of kids with an ex-spouse or partner. Whoever counts the kids as their dependents on the tax return is the one who can count them as part of their household size for ACA subsidies — even if the kids spend more time living with the other parent.

Stella B

@Upper West: small business group plans are definitely available on the exchanges. Larger employers (the 50 person cut off, I believe) are out of luck for a few years still. They have to find insurance the old fashioned way.

Raven on the Hill

@Stella B: “we’re very, very far from ever qualifying for a subsidy.” Then you’re good on that, at least. But I hope you will look at your potential expenses. If either of you have chronic conditions that need medical management, and these often emerge when people are in their 50s, it’s likely the expenses not covered by a bronze plan will outweigh any savings on premiums.

I don’t know your situation. I only hope you will be careful.

Raven on the Hill

@Upper West: the word from the horse’s mouth is: “Whether you qualify for lower costs based on your income will depend on the coverage the employer offers. You won’t be able to get lower costs if your job-based coverage is considered affordable and meets minimum value.” Check out your exchange site, if it’s running, or look at the discussion on healthcare.gov; they give specifics.

Mnemosyne

@Raven on the Hill:

Basically, if you choose to go onto the exchanges, you may not get a subsidy if your employer’s plan otherwise meets the law’s requirements. That doesn’t mean you won’t get a lower overall price by going through the exchanges — it just means it may not be subsidized.

So if your employer’s insurance seems overpriced, it’s worth checking to see if you can do better even without a subsidy.

Steeplejack

@kc, @kc:

You can get an idea of what plans are available without creating an account.

Raven on the Hill

@Mnemosyne: yes, we agree on this.

carbon dated

Josh Barro, RINO journalmalist, takes issue with the pie chart. I think he makes a decent point.

PopeRatzo

@Anna in PDX:

It has been just spectacular, watching putative liberals supporting the disastrous “insurance” payment structure for health care.

Our Great Liberal Victory is a Heritage Foundation idea, designed to fuck the poor and middle-class. Overheard in blog comments: “Sucks to be you.”

God-damn…

cleek

@PopeRatzo:

idiocy