I was having a good productive discussion with a commenter via e-mail yesterday on window shopping. We were trying to figure out what plan made sense, and the big challenge was reading the label at Healthcare.gov. During the discussion, I had some fun with SnagIt on an example plan, and realized that this could be useful for a lot of people when they look at their health insurance choices:

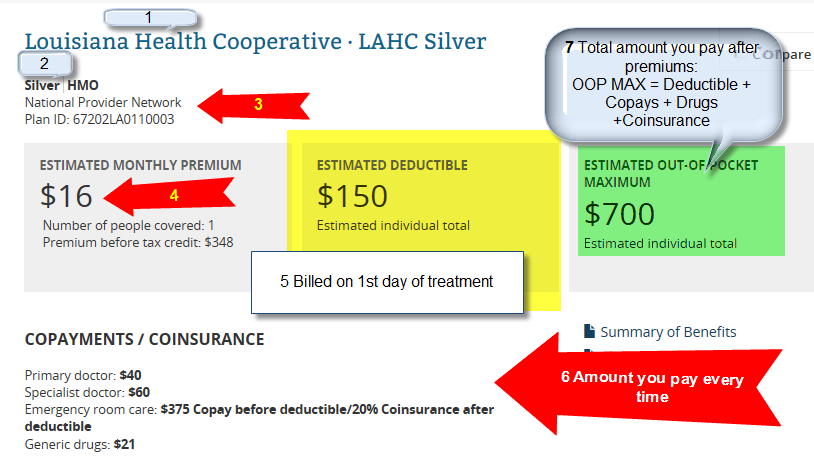

So let’s work our way through the label:

1) Insurer name and Insurer plan name.

2) Metallic band level and basic plan design. The band levels are rough estimates as to how valuable the coverage is. Bronze covers 60% of expected average costs, Silver usually covers 70% of expected average costs, Gold covers 80% of expected average costs and Platinum covers 90% of expected average costs. I don’t like that there is no indicator of Silver Cost Sharing Subsidies nor the level of cost sharing assistance as a Silver with maximum assistance is better than Platinum.

3) Network — insurers can call their networks anything, so this is moderately informative. My company has Mayhew Narrow, Mayhew Middle and Mayhew Broad, so you can compare like to like.

4) Premiums are what you pay every month

5) Deductible is what you pay before any insurance kicks in. There are non-deductible services (Annual wellness exam, Ob/Gyn, contraception, vaccines etc) but if you are having surgery for itchy elbowitis (and yes, I was watching a show about a slightly bossy 6 year pig last night) , you would be liable to pay $150 before insurance does a thing.

6) Copayments are what you pay every time you use a service. In this case, a visit to a primary care doctor for illness costs $40, while a visit to an orthopedist or other specialist costs $60. This particular plan is pushing real hard to keep people out of the Emergency Room with a very high co-pay. Coinsurance is your share of the cost after the deductible is paid but before the out of pocket maximum is reached.

7) Out of Pocket Maximum is the most you’ll pay over and above your premiums in a year. It is the sum of your deductible, your co-pays, and your coninsurance.

So let us walk through an example.

Let’s say you are reasonably healthy but you have a severe case of itchy elbowitis that requires an elbowectomy in January. Elbowectomies are major surgeries. The surgeon, anesthesiologist and hospital will present $30,000 in bills to your insurance company. Since you stayed in network, the insurance company has contracted rates that brings everything down to $7,500.

You are responsible for a $60 co-pay for the surgical prep visit the week before surgery. The prep visit has a contracted price of $125. You are also paying $65 towards your deductible. The prep visit will cost you $125.

You go to the hospital on Tuesday morning, and by Tuesday afternoon, there has been a sucecssful elbowectomy, and you are in bed recovering. You’re on the hook for another $85 of deductible, so there is still $7,415 outstanding. You have a 20% co-insurance that will apply to the next $2,450 in charges. This will mean you pay $490 and the insurance company pays $1,960. Now you have hit your maximum out of pocket limit for the year. The insurance company writes a set of checks for $6,925 to the various billing entities.

Your rehab is now cost free to you. And if you come down with pink-eye in July, that visit is cost free to you as well.

Villago Delenda Est

OK, that’s way too straightforward. Needs to be mucked up a bit and confoozled some more.The CEO’s dominatrix is expecting some rather expensive new diamond studded whips for Christmas this year.

raven

I was interested that none of our plans were gold. We’s had some pretty major surgery and not paid very much at all with the BCBS HMO.

Richard Mayhew

@Villago Delenda Est: If PPACA works right, that dominatrix will need to look for new clients soon as insurers are moving towards the regulated public utility model where we are effectively pass-through entities and risk managers instead of looters.

Now if she is still interested in the medical field, go down the street to the specialty practices, and those docs will ask for another

Richard Mayhew

@raven: what state are you in? I am surprised that there were no gold plans in your region as most insurers offer something at every metal level as it is the same risk pool to them.

Suzanne

@Villago Delenda Est: That actually sounds way hotter than the reality.

KG

Isn’t this pretty much the underlying issue with healthcare in the US? “That’ll be 30 grand.” “Nope.” “Ok, we will take 28%.” “Deal.”

PhoenixRising

And that, my brethen and sistren, is why you will play hell trying to schedule an elective (in timing, not whether it’s ever paid for) procedure in Q1.

Come back closer to the end of your benefits year, kids…we’ll be happy to pay the LAST dollars before OOP.

If you want something truly elective, like lasik, call on Jan 2 & every 2 weeks thereafter asking for a discount. If the doc has a free table you may just get eye surgery for 70% of retail because no one is using their benefits in Feb.

Linnaeus

Okay, I need to change my plan.

raven

@Richard Mayhew: Georgia, I sent you the choices from our organization. When you posted it you mentioned that none of them were gold.

Richard Mayhew

@raven: Oh, okay, that jogs my memory again — private plan sponsors can offer whatever they want.. I was stuck in the Exchange head space on my last comment.

raven

@Richard Mayhew: I’m sorry, I went back and you said “This is interesting for four reasons. First, the university is showing both the cost to the employee and the total premium cost. This is unusual but becoming more common. PPACA requires employers to tell employees the cost of health coverage in box 12DD on the annual W-2. They are not required to show it in the open enrollment period. None of these plans are Cadillac plans.

I may have been comparing apples to transmissions. . .

And your answer makes perfect sense, thanks.

Buddy H

Two brief clips from a 1940 Bob Hope film. Democrats (zombies) and republicans (back from the dead). History repeats itself, again and again, but nobody notices, because nobody takes comedy seriously:

democrat zombies:

http://www.youtube.com/watch?v=8fv5I2rmtuU

republican living dead:

http://www.youtube.com/watch?v=G_AgoX_jam8

KithKanan

@raven: Assuming you’re the one Richard used the enrollment info from in his 10/31 post, your “Comprehensive Care” plan option looks Platinum to me, while the “Consumer Choice HSA” option looks Silver.

I don’t know enough about how HMO plans work to map the HMO plans to metal levels, because in my semi-rural area HMO plans are way more expensive than PPO options so few employers opt for them.

Richard Mayhew

@KithKanan: yep, I think there was basically a high gold/low platinum (Comprehensive Care), a mid-gold with Kaiser, a mid silver to low gold Blue Choice HMO, and a low Silver/high Bronze in the HSA…. the Cadillac portion of the post was on total premium cost. none of those plans are on the path to hit the Cadillac threshold.