Aaron Carroll at the Incidental Economist has an interesting post on the health care costs of Medicaid expansion populations.

There were somestudies that made predictions about the health and composition of the newly eligible for Medicaid. Those studies could be interpreted to mean the Medicaid expansion would cost less than predicted, because people entering would be healthier than those already enrolled. I WAS ONE OF THE PEOPLE WHO THOUGHT THAT INTERPRETATION MIGHT BE POSSIBLE. A recent report from CMS suggests that this lower-than-expected expense didn’t happen. I wrote that we need to figure out why and keep watching….

that there are some reasons that the differences are higher than estimated:

There are several explanations for the difference between the estimates in this year’s report and those in previous reports. First, most of the States that implemented the eligibility expansion are covering newly eligible adults in Medicaid managed care programs, and on average the capitation rates for the newly eligible adult enrollees were significantly greater than the projected average costs previously calculated.

Austin flagged this, by the way. In fact, some of the capitation rates may have been raised because states predicted pent-up demand because they assumed people entering might be sicker (in spite of the research I talked about).

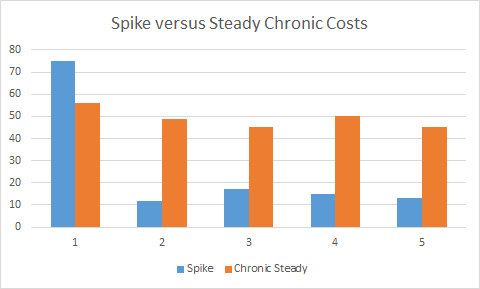

There are a few interesting things here. The first year of any medical insurance expansion to a population that was mostly uncovered is always a shot in the dark. We don’t know how much catch-up care is needed. We know that catch-up care is needed. For instance, we know that Medicare sees the first year cost of members who were either uninsured or massively underinsured during their age 64 year to be much more expensive than the first year costs of people who have Gold/Platinum employer sponsored coverage during their age 64 year. However after a few years, these groups converge. We know that on the Exchange, there is catch-up care compared to people in employer sponsored plans.

There are a few interesting things here. The first year of any medical insurance expansion to a population that was mostly uncovered is always a shot in the dark. We don’t know how much catch-up care is needed. We know that catch-up care is needed. For instance, we know that Medicare sees the first year cost of members who were either uninsured or massively underinsured during their age 64 year to be much more expensive than the first year costs of people who have Gold/Platinum employer sponsored coverage during their age 64 year. However after a few years, these groups converge. We know that on the Exchange, there is catch-up care compared to people in employer sponsored plans.

Catch-up care raises a few important questions. The first is whether or not it is actually catch-up care or a chronic condition. Risk adjustment data is just starting to finalize for the 2014 Medicaid expansion population now as claims from December should be in by now, and the state level data collection, processing and analysis might be able to get a good grab on the data. Good data and analysis on 2014 risk pool composition for Medicaid expansion won’t be available until the end of this year or the Spring of 2016. Secondly, the question is how fast does the spike decline. In states like Michigan that has effecively hoovered up every Medicaid expansion eligible individual into the program, there are very few people left who are Medicaid expansion eligible who have not at least started their catch-up care. In states that expanded Medicaid but have not aggressively enrolled everyone eligible, there is still a pool of people with significant catch-up care costs that will be incurred when that person has low cost-sharing health insurance at some point in the future. In rejection states, there is a massive pool of catch-up care.

Dentistry is a common area of adult catch-up care and a great example of the cost spike and crash. Catch-up care is significant quality of life improvements. It is quite common for an adult who has not been to a dentist in several years to show up to their first appointment with a dentist needing several cavities to be filled, a root canal performed, a molar extracted plus the normal X-rays and cleaning services. That first year might see $1,500 to $2,000 in dental procedure costs. However their mouth no longer feels like it is on fire, general inflamation goes down (which has other good long term health benefits) and the visits in the second year go down as the person might have a small surface cavity that needs to be cleaned out and filled, plus a preventative cleaning. This is an easy case of catch-up care.

Chronic conditions also have a catch-up care component.

Diabetes is a more complex case of catch-up care. JAMA had a study that looked at the prevelance of diabetes in Legacy Medicaid and Medicaid Expansion eligible populations. They found that the Medicaid Expansion population had a lower prevelance of diabetes, but the people in the Medicaid expansion pool who were diabetic were far more likely to either not have been diagnosed as diabetic or to not have their diabetes under control when compared to people covered by Legacy Medicaid. A big pool of people with diabetes entering Medicaid for the first time where it is more likely than not to be uncontrolled will lead to a first year cost spike. That cost spike will result from more people actually being diagnosed and then treated as well as the people with diagnosed and uncontrolled diabetes getting treatment (and having a crisis/complication) while they work to get their sugar levels under control. However, even though diabetes is a chronic condition, a well controlled diabetic is far cheaper (and enjoying a better quality of life usually) in Year 2 than that same person as an undiagnosed/uncontrolled diabetic in Year 1.

The final thing that I want to respond to is the matter of capitation rates for Medicaid Expansion. This matters only in states that use a managed care set-up. I know for a fact that several states that did Medicaid Expansion with managed care in 2014 decided to be super conservative in their projections (after all, it is 100% federal money). They selected actuarial models and outputs that were 2nd and 3rd standard deviation cases to set up their base rates. They assumed a tremendously sick population, and then paid their managed care organizations a lot per person. They did this because several states either had a hard MER floor where the MCOs will refund capitation rates that drops their MER underneath that floor, or there were Medicaid Expansion specific risk corridors. This means a lot of money went out the door in 2014, but a lot of money will be returned to the states as risk adjustment is finalized this summer and fall. It was a public policy bet that the federal government money at 0% long term real interest rates could bear a lot more downside risk than managed care organizations that were facing a new population with minimal data. So state level expenses won’t actually match state level expenditures and administrative costs for 2014 until at least Q1 2016. Expenses and actual costs are different things.

Another Holocene Human

When the diabetes isn’t treated …

And the foot gets gangrenous …

And it’s amputated under uncompensated care …

And the amputee applies for disability and goes on Medicaid …

That sure saved everybody a lot of money, didn’t it.

currants

Which reminds me–Richard, slightly off topic, but I saw this article about Monroe Bird on Field Negro, and–well, WTF can we do/can be done about things like THIS??

Richard Mayhew

@Another Holocene Human: Saves it in Year 1, you’re someone else’s problem for Year 5…. and think of the quarterly bonuses that won’t be paid, and how the hookers won’t be fucking on Thursday night and the blow that won’t be consumed.

Why do you hate poor Columbian peasants?

Oh the humanity….. oh the humanity.

Benw

@Another Holocene Human: it sure did b/c the patient’s church held a bake sale and raised $1M to cover the bills!

Richard Mayhew

@currants: Sue the insurance company for breach of contract.

currants

@Richard Mayhew: [long pause]

Yep. Assuming you can afford the lawyer to do it (right).

Richard Mayhew

Contigency basis or cost of coverage plus reasonable attorney fees… this is a slam dunk case assuming the facts presented in the blog post are accurate. No charges filed, no convictions etc, just the word of a DA… an insurer is on the hook to pay. I showed that post to a pair of attorneys in company legal, and their reaction was the insurance company currently denying claims is on the hook for massive liability as long as we assume the facts in the post are uncontested. Both would be willing to take on the case with zero up front fees.

Benw

@Richard Mayhew: Richard, we come for the health insurance minutiae, but we stay for the discussion with the company lawyers!

The Moar You Know

We lost our grandfathered status with UHC. Today we got the bad news. Looks like Bronze for us unless we’re willing to eat a 40-50% premium hike; even if we were willing, we can’t. We don’t have the money.

UHC is the only company that will work with us as the majority of our employees are outside the state we’re incorporated in – CA. We and our employees are fucked with a capital F. Looks like we’re getting Bronze and an expanded HSA plan ($6k/yr), which is not really any kind of solution. We will lose people over this. Hopefully not many, we don’t have that many to lose (under 50).

I really don’t want to sound like one of those guys, but I will: this is not what I expected Obamacare would allow. I don’t know what’s happening with larger employers but this small company is not happy today.

Mnemosyne (iPhone)

@The Moar You Know:

The state of California has been really on top of monitoring insurance company shenanigans. I would call the state department of insurance right away and tell them that UHC is trying to screw you. Depending on what other state(s) your employees are in, California may be able to work with the local state’s attorneys to try and fix the problem.

As an employee, I think you should be up-front with your employees and tell them exactly what’s going on. If they have decent state exchanges, maybe it’s more economical for all of you for you to put X amount into an HSA and have them buy their own insurance.

Mnemosyne (iPhone)

@The Moar You Know:

Also, too, make sure that you contact HHS and let them know what’s going on. They can’t make new regulations to protect you if they don’t know it’s happening.

mclaren

Once again, Richard Mayhew is lying to you. The wonkish tone of his posts suggests that the ACA is wonderful and everything in moving along nicely. In reality, the broken health care system in Shithole America is collapsing and rapidly pricing everyone but the super-rich out of health care:

Source: “Wrong prescription? The failed promise of the Affordable Care Act,” Trudy Lieberman, Harpers magazine, July 2015, pp. 32-33.

Richard Mayhew

@mclaren: Hey McLaren, it’s been a while since you’ve ranted, I was getting worried for you that you were becoming hinged.

If you actually read what I write, I agree that the high deductible mania is ridiculous, and the better path forward is low first dollar, high actuarial value coverage for everyone. How do we get there, and in your counterfactual world, is telling 15 to 20 million people to go fuck themselves for another generation instead of using PPACA to enhance their lives a viable moral trade-off? In mine, it is not, I’ll take better and attainable over perfect and nowhere close to 50 votes in the Senate every day of the week.