This is a follow-up from yesterday’s post on United Healthcare self-inflicted woes:

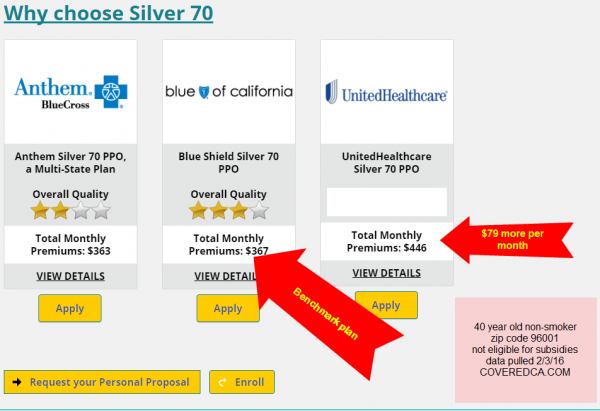

I chose Redding, California as it was the first town in Northern California that was readily apparent on Google Maps. As you can see, for a 40 year old non-smoker, United Healthcare’s lowest priced Silver is $79 more per month than the benchmark plan. For someone making exactly 150% of the Federal Poverty Line this is roughly 5% more of their monthly income.

Andrew Sprung on another matter pulled up UHC’s pricing versus a narrow network Medicaid based insurer in several major markets:

@bjdickmayhew @rebeccastob @charles_gaba @adamcancryn cf UHC pricing vs Ambetter’s https://t.co/wy8s4qnxS1 pic.twitter.com/Qe8LzV7deQ

— xpostfactoid (@xpostfactoid1) February 3, 2016

Again, the difference between the cheapest plan and the lowest priced UHC plan for someone who makes 150% FPL is several percent or more of their monthly income. In Atlanta and Chicago, to buy UHC’s products it would be a bump of 6% of monthly income for that individual.

We know the Exchanges are price sensitive for most people. The only people where the 6% of their monthly income might be worth it would be people who know they are very sick and they have very high needs that they want to have met by doctors they’ve seen for years at facilities they have used for years.

Dork

Can I get this in English?

bystander

I’m compelled to ask an irrelevant question: does @bjdickmayhew get a lot of inappropriate tweets?

Hildebrand

I suppose this is not the time to mention the whole ‘the market will decide’ mantra that is conveniently forgotten when it is one’s own ox getting gored?

Didn’t think so.

Business is so damn mysterious.

Face

@bystander: Oh my. Nice catch. Yes, “BJDick” anything is ripe for bro tweets. Unless Rick is obtuse (unlikely), I’m guessing he knows just how “catchy” this handle is.

Ohio Mom

Don’t worry, UHC is making it up by denying my family’s claims. Which reminds me, it is after nine in the morning, offices are open, time to start in on the phone calls again.

Mai.naem.mobile

@Dork: HIX is the health exchange and ESI is employee sponsored insurance

Mai.naem.mobile

The reason I didn’t choose UHC is because I know several people(family,friends,coworkers) who’ve had problems with UHC giving them a real runaround paying for stuff.

Eric S.

@Mai.naem.mobile: UHC is infamous for denying claims in my circle of family and friends.

Richard Mayhew

@Dork: Translation:

The big national carriers in their first year of operations on the Health Insurance Exchanges (HIX) often treated the individual market as if it was a smaller version of the Employer Sponsored Insurance (ESI) market. That meant they were offering fairly wide networks with a higher proportion of PPOs over EPO or HMO plans. Those plan designs with wide networks means the insurers don’t put too many structural “No’s” into place nor do they have the ability to get cheap rates from a subset of their providers. That means their plans tended to be both expensive and attractive to sick people.

Carriers learned that the individual market is not the ESI market. People were WAY more cost sensitive than a lot of people thought, as the enrollment numbers were going to narrow network HMO/EPO while the very sick went to to the broad PPO’s . In 2015, a lot of carriers (including Mayhew Insurance) changed their network strategy to narrow things down and drive pricing as low as possible even as we as an industry introduced way more point of NO into the process. We made money in 2015 because of that strategy change. We learned what to do by learning what not to do first.

So in 2016, insurance companies that have been on Exchange since 2014 have had 2 full years of learning by doing. UHC just had a single year, so they are still learning by fucking up.

@bystander: Very few as I have one of the geekiest twitter clusters imaginable.

Scout211

I have Tricare and UHC took over from the TriWest Health Alliance a few years ago for the Tricare western region. I have often wondered why UHC would bid for a Tricare contract. The Feds set the costs and the fee schedules. It can’t be a money-maker for them. Can it?

What are the incentives for them to jump into government-provided healthcare?

b1narys3rf

Richard,

Where do you get these “quality ratings”? It is very difficult to find any reviews online of HMOs other than complaint boards amounting to “they all suck.”

Richard Mayhew

@b1narys3rf: NCQA is a good source:

http://www.ncqa.org/ReportCards/HealthPlans/HealthInsurancePlanRankings.aspx

boatboy_srq

@Eric S.: @Mai.naem.mobile:

Wow. So, they’re charging a premium for the opportunity to be d!ckish about covering their customers, amirite? Are they trying to go out of business?

CONGRATULATIONS!

UHC was the only insurer besides Kaiser we could get to take on our company (we offer both) They were not cheap and they seem to have a nasty habit of partially paying claims.

Better than the managed death system offered by Kaiser, but not by much.

@Mai.naem.mobile:

@Eric S.:

I am living this nightmare. Problem is they aren’t actually denying anything, they’re just not paying anywhere near the amount billed, leaving me and other insureds to pick up the slack. I cannot believe this can even be legal, but apparently when you’re sucking down 20% of the entire nation’s GDP, pretty much anything is legal.

laura

Another example of health insurance vs. health care. Single payer is the only solution for basic health care.

Mai.naem.mobile

The UHC CEO took home a $66M paycheck for 2014. And a few years before it was $106M. He is not a co-founder of the UHC just the CEO unlike Bill Gates with MS or the Google guys.

jl

I was puzzled by attention to to UHC, abut looks like its difficulties is being used by hacks ad the sad poster child for the failure of PPACA:

The Real Reasons Insurance Companies Are Complaining About Obamacare

http://talkingpointsmemo.com/dc/obamacare-insurers-complaints-threats

I am with Krugman in thinking that is wise to remind people that all this network and pricing stuff is socially wasteful BS, unless this country is willing to let sick people die and rot in the streets, at work an in their homes; turn them away from ERs, and deny them admission to hospitals when life and limb is obviously at stake. Unless we do that, all this insurance market strategizing, and NO-pointing done in order to cherry pick some people at annual open enrollment (or ‘qualifying events’ for the exchanges) is socially wasteful garbage. I think RM has made that point before, though.

Also might want to note that clinicians have developed strategies to evade NO-points when they see a patient who might die or become maimed if standard of care is denied. This is usually in ER when some clinician decides that somebody really needs to be admitted rather than sent on their way, so often big ticket item.

The linked article claims that the fuss is to avoid more regulation to reduce profiteering that they think is coming their way. If we want to ‘GO SWISS!’, which is probably the best model of mostly private universal health care system, which is relatively high price but offers excellent timely care, then any PPACA regs coming down the pike are very very weak sauce compared to Swiss regulation, which does Not fool around.

I also think important to note that much of cost of this kind of nonsense is not excess profits going to insurers, but excess real costs generated to the system by lower quality care that is produced by stupid insurance and provider games.

Ohio Mom

I think I got our insurance snafu fixed (have to wait for confirmation to come in the mail) but on the way, discovered there is another rejected claim from October. That’s for tomorrow.