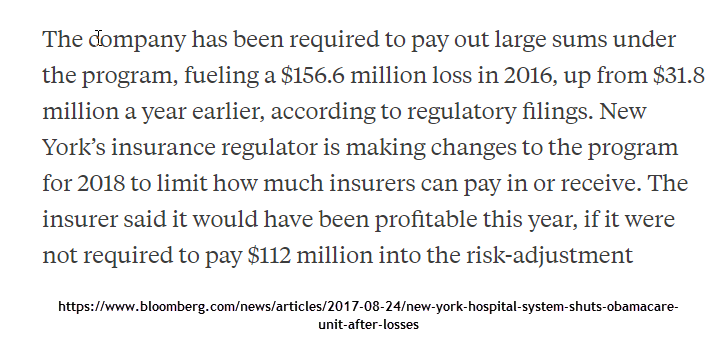

Northwell in New York State is getting out of the insurance business in New York State. Zach Tracer at Bloomberg reports that the Care Connect subsidiary is shutting down. They are partially blaming risk adjustment.

There are three stories that can be told about risk adjustment as an integrated delivery network (IDN) in New York State. One is a structural story about the market. The other two stories are stories about Northwell and the challenges and opportunities of a hospital running their own insurance arm in a risk adjusted market.

The first story is that New York State is weird with lots of odd rules. It still has true community rating where a 21 year old pays the same premium as a 64 year old. It has a Basic Health Plan that covers most of the 133% to 200% of Federal Poverty Line population. It has an extremely funky market in New York City and then once you get out of metro NYC, most of the state is rural. There could be a story that the market does strange things to new entries. We saw Health Republic had trouble in the state. Oscar has trouble in the state. Care Connect had trouble in the state. Insurance is a tough business and the local circumstances in New York State could make it tougher for new entries to the market.

An IDN with low leakage rates should be in a position to aggressively manage and optimize their risk adjustment scores.

Now the other two stories are risk adjustment stories. The first story is that Care Connect enrollees are significantly healthier than the typical New York enrollees. In this story, the coding on the claims is reflective of the patients’ underlying conditions. This is an insurance division problem. They are pricing their products at a point which attracts a lot of healthy people but the price is too low. The price is being set at a point which does not reflect the cost of care plus the cost of risk adjustment.

The other risk adjustment story is that the patients are as sick as the typical enrollee and the premium is an accurate reflection of the cost of care and thus the underlying medical status of the population. But the claims are not being coded aggressively. If this is the case, then it is an integrated delivery network that is not integrated nor delivering on the aligned incentive promise. The docs, in this scenario, are coding as if they are still under non-risk adjusted fee for service contracts. Other insurers would be optimizing their docs to code aggressively and completely to bump up risk adjustment scores.

Care Connect/Northwell has extensive clinical medical records for its patients. They should have good medical history on quite a few of their more expensive patients as their docs have been treating those patients in their facilities for years before the Exchanges opened up. They don’t have a good argument that the cost of data is too high for them to optimize their risk adjustment. If they are not optimizing their risk adjustment coding from at least the docs that they own and control, than that is just a management problem and not a risk adjustment problem.

Another Scott

You outline yet another example that reality is more complex than relatively simple stories that (especially, self-interested) people tell. And an illustration that “arm-chair experts” really aren’t experts, there’s (often many, good) reasons why “obvious” solutions usually aren’t real solutions, etc., etc.

Stuff is complicated, and details matter.

Are there a few words missing in this sentence?

Same as what/who?

Thanks.

Cheers,

Scott.

Baud

Matty Y is calling you out.

https://www.vox.com/policy-and-politics/2017/8/29/16196608/wonks-single-payer

sibusisodan

@Baud: That’s such a weird framing. Perhaps it’s time for those who want the policy to _ask the wonks for help_? That might be more productive than for ‘the wonks to step up’.

Plus, if the wonks have already said ‘we don’t think you can do it this way’, what else should we expect.

Finally, his examples of aspirational policy proposals are fine as far as they go. But none of them start from ‘dismantle the existing massive system’. That’s a massive difference.

David Anderson

@sibusisodan: @Baud:

I think that is an excellent call. And to be honest, there has been a disconnect between the policy wonk wing and the popular wish list wing of the Democratic Party on single payer. The biggest difference I think is a judgment on the importance of loss aversion versus everything is awesome. And that is a clear value judgment as much as a technical judgment.

Barbara

The reimbursement to physicians for the kind of services they provide is often independent of the severity of the diagnosis/code, and many physicians simply hate coding, and try to stick to the dozen or so most common codes. This is a way of saying that the financial interests of physicians are often not aligned with those of IDNs or, for that matter, hospitals, that employ those physicians. I don’t know what the best answer is, but I have observed this occurrence repeatedly.

David Anderson

@Barbara: Completely agree on all counts.

And that makes it a management/internal incentive question. IF docs aren’t rewarded for helping the insurance side do well, than what exactly is the value proposition of an IDN?

Bradley Flansbaum

Dave

As a former doc at Northwell, coding and CMI was never a major issue–at least on in the inpt side. And if clinician approaches to patients are payer agnostic, and they usually are, Medicare CMI in line there with national avg there. Should be the same with commercial lives. I don’t think that was the root cause.

Brad

Barbara

@Bradley Flansbaum: Most provider driven payer/insurer initiatives fail for reasons other than “risk adjustment” to optimize revenue. They fail because the essential mission of a hospital is to fill beds and maximize hospital revenue. It’s very hard for hospitals that own insurers to see insurers as something other than a referral vehicle. Failure to make that leap dooms an awful lot of these ventures.

Bradley Flansbaum

@Barbara: Perhaps you should address your response to Dave