Insurers have signed their final rate contracts for 2018 participation on the Exchanges. Most insurers are assuming that Cost Sharing Reduction (CSR) subsidies may not be paid in 2018. State regulators in most states are allowing insurers to either price CSR into their baseline premiums or they approved two sets of rates, one with CSR and one without and are allowing insurers to reprice mid-year if CSR is pulled in 2018. Insurers are getting ready for a market that they know is not stable and is prone to monkeywrenching. Most of that prep work means raising premiums.

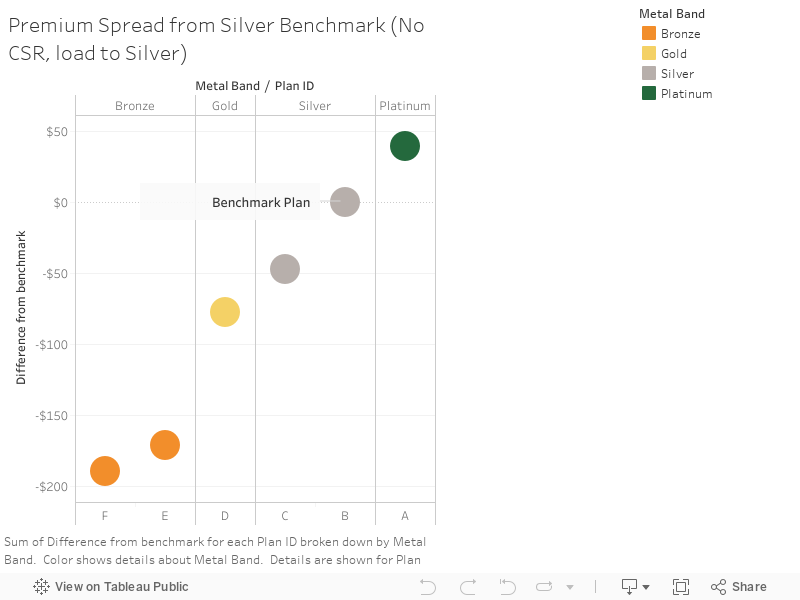

It also produces weird effects. States that tell their insurers to first assume that CSR will not be paid and then to load the entire cost of providing the CSR benefit onto Silver plans will see strange pricing. Silver plans are nominally 70% actuarial value. In typical times, they are more expensive than Bronze, less expensive than Gold and much less expensive then Platinum plans. That is not the case in the No CSR, Silver Load scenario.

The chart below uses data from a single insurer in a region where they are the sole carrier. They received rate approval to assume that CSR would not be paid and to load the incremental CSR costs only onto the Silver plans. We can see that Silver is now more expensive than Gold and Bronze and just slightly less expensive than Platinum.

This is the Gold Gap strategy for 2018. This is what happens when the benchmark has been effectively moved and attached to approximately 90% actuarial value instead of 70% actuarial value. 80% AV plans become comparatively much cheaper for subsidized buyers and Platinum plans are no longer far out of reach for most subsidized buyers.

Bronze plans are now much cheaper than Silver plans. Bronze plans in 2017 for this carrier were priced as if they were about 10 actuarial value points less comprehensive benchmark. In 2018, Bronze plans are priced as if they are 30 actuarial values points less comprehensive than the benchmark plan. A pair of 40 year olds earning $32,000 now could buy a Gold plan for $1 month. Bronze plans will be extremely inexpensive up to the edge of the subsidy income range. Lower net of subsidy costs will bring in more people.

The downside of the Gold Gap is that is it only an on-Exchange mechanism that will improve enrollment. Off-Exchange, non-subsidized buyers will be facing higher costs. Bronze, Gold and Platinum buyers will be facing price increases that are a function of medical trend and the one time hit of the re-institution of the health insurance premium tax. Silver buyers will most likely need to change metal tiers as they will be seeing massive premium increases.

lagarita

I’m in Colorado and just received a letter from Cigna saying that my Silver exchange plan isn’t being offered next year. Is that normal (this is my first year) or because of all the uncertainty? Why don’t they just increase the premium?

NJDave

The chart doesn’t display correctly. Only the top 1/4 to 1/3 shows. (IPad, Safari).

J R in WV

I have a bug needling me on this health care issue. People seem to think there’s a thing called “single-payer” which will improve health care coverage across the population, which that just isn’t so. Who pays for people’s health care and who among the people are eligible for that health care are unrelated issues.

Universal Care is the principle that everyone gets the health care they need. All sorts of different payment schemes could be folded into Universal Care, Veterans’ benefits, Coal miner’s benefits, employees’ benefits, retirees’ benefits. Plain ol’ people who never worked and the working poor have benefits like Medicaid. All those payment schemes are OK by me, as long as everyone has a scheme that they can fit into at all times and under all conditions.

Single-payer is a diversion, a ruse, to distract people from the real cause we should be fighting for: Universal Health Care Coverage for everyone under the banner of the USA.

Single-payer is being used by people who oppose universal care, people who don’t ever expect to implement single payer because they intend to prevent the ACA, Obamacare, from being around long enough to ever have single payer implemented, unless the single payer is us, everyone, individually.

Whenever I see someone calling themselves a progressive fighting for health care and the only thing they talk about is Single-Payer I know I’m seeing someone fighting tooth and nail under the covers to keep universal coverage from ever being even mentioned, much less implemented across the land.

There! I’ve got that off my chest, even it’s on this technical insurance thread where no one will ever see it but me and David-Richard.

Marcopolo

As someone who is insured through the ACA, I expect my costs to be anywhere from 30% to 50% higher in 2018. Also I will be enrolling ASAP instead of waiting for the last 48-72 hours as I have in past years. With the shitbags trying to sabotage it at every opportunity, I will keep my fingers crossed that those are the only issues I will face.

Also want to thank David for these posts. Although they get few comments–from me for example, I read, appreciate, & am informed by them.

Any word on the street about the status of reupping CHIP?

David Anderson

@NJDave: click on it and it will take you out to the hosting site

Ruckus

@J R in WV:

I think you are being a bit hard. Some (a lot?) of people really have no idea what single payer really means, they won’t find out from anyone with an axe to grind and yet what they really want is to get rid of the insurance companies. They think that Medicare is free healthcare. Of course it isn’t, you pay in when you work, I’ve been doing that for decades, as I’d bet you have, to use Medicare to go to a doctor, you have to pay every month, the last number I was given was $109/month. And then you have a 20% copay. It’s far better than nothing but it ain’t free. It is a lot easier though. You are correct that UHC is what controls costs better and gets rid of the profit margins. However UHC is what the VA really is, just a subset of the population. It’s good healthcare but it is not without issues and primarily the biggest issue is their budget. Every wack at the budget cuts service at the VA. That makes the final healthcare worse. Given our fucked up political arena, I think the best we can hope for now is to trundle along maybe making small fixes to what we have. Or have the conservatives kill healthcare altogether for the bottom 90% of us. After all we have no value, right?

Fair Economist

It’s going to look strange to customers to have Silver plans priced about Gold plans. The insurance companies are going to field a lot of calls saying “hey, you made a mistake in your pricing”.

gvg

gold is better than silver right? Or did they do something nontraditional and make silver better? I am having trouble understanding what I am seeing.

Steeplejack

@gvg:

Yes, a gold plan is supposed to be better than silver. Beyond that I can’t help you.

Wesley Sanders

Gold “base” plans are better than silver, but the silver plans are where CSR variants come from. So if you are eligible for CSR, the silver plan is usually better than the gold. The silver plans are priced higher in 2018 because insurers are loading the CSR cost into the premium instead of assuming the feds will cover it.

David Anderson

@gvg: I’ll explain tomorrow :)

Gold is lower out of pocket expenses than Silver

This is where things get WEIRD!

justawriter

Paging Mr. Mayhew: Medica Leaving North Dakota Individual Health Insurance Exchange in 2018

Significant? Horse hockey? Inquiring minds want to know.

David Anderson

@justawriter: Minor — Medica is covering their own ass. North Dakota is not allowing a Silver load so Medica, which is pessimistic that CSR will be paid, is not taking the risk. If CSR is paid, the insurer(s) in North Dakota that assume that it will be paid will make out like bandits If CSR is not paid, the optimists get kicked in the junk.

justawriter

Thank you. I’m still going to put up my umbrella for the sh1tst0rm of “Obamacare is doomed” coverage this is going to generate in my state’s “what’s so bad about Nazis?” local press.

Buskertype

David:

I’ve been trying to understand what the failure to reauthorize CHIP before it expires this weekend means. I gather that it doesn’t mean that my daughter will not be covered next week (right??) but that eventually the funding that the states have already received will run out… is that approximately accurate?

David Anderson

@Buskertype: I do not know, the fallout will vary by state

Buskertype

@David Anderson: ok, thanks