UPDATE 5/2/18 I transcribed the Georgia Individual market RA score wrong and flipped the numbers. No state has an individual market risk score higher than the small group market. Image has been updated.

Being able to work 1,500 hours a year is one hell of a screen for health status.

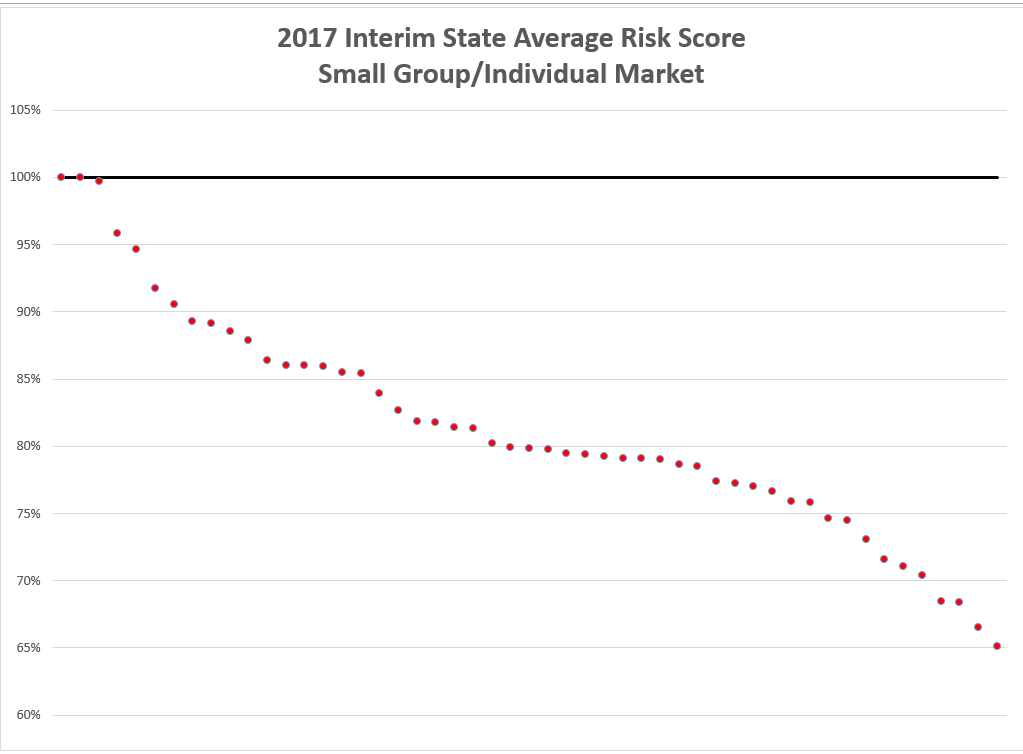

CMS released the interim risk adjustment estimates for 2017. Each state has three lines: ACA metal individual market, catastrophic individual market and the ACA regulated small group fully insured market. Each line is risk adjusted only against itself. CMS produces a state wide average risk score (plan liability average score). This number varies by state. The higher the number, the sicker the population has been coded.

I want to highlight the differential spread between the individual market and the small group market risk scores. They both use the same risk adjustment scheme and the unit of analysis is the state. I have divided the small group average score by the individual market average score. If the number is greater than one, then the small group market is coded as sicker than the individual market. If the number is less than one, the small group market codes as healthier than the individual market.

One state has a small group market that is coded as sicker than the individual market in 2017. Two states have merged their small group and individual markets together into a common risk pool. And then the other forty eight nine states (including DC) see their individual markets are coded as sicker than the small group market.

There is significant variation in the health status of the small group market relative to the insurance market. One state small group market is 35% less sick than the small group market.

Being able to work 1,500 hours a year (30 hours a week/50 weeks a year) is one hell of a screen for good health. The individual market has a significant number of folks who also work at least 1,500 hours a year, but the individual market also contains a lot of people who have significant limitations that are functional barriers to nearly full time work. Those significant limitations are also likely to be expensive health conditions that have high risk adjustment scores.

Linking insurance to work is one hell of a health screening device.

The Moar You Know

If you can do that you’re healthy enough, for a while. But what about the more civilized nations where 4 to 6 weeks of vacation is normal? How does that break down?

(I might add I have never seen a two-week vacation in my life since elementary school and doubt I ever will – which as far as I’m concerned is a huge problem for American society.

Not to mention I could use one.)

Starfish

@The Moar You Know: My spouse made that comment about our recent trip to Canada. He said that Canadians travel a lot more than Americans.

Yarrow

It’s immoral and should be eliminated as a practice. Health insurance should be offered and purchased separately from work. Our entire society would benefit. Better plans would be available to those who didn’t work full time for a big corporation, people could have easier job mobility, working less than full time would still mean you could get good health insurance.

The whole system is rigged to benefit corporations who get, as you say, a reasonable health screening device for workers. They also have all the power–healthcare handcuffs as I call them–because people are afraid to leave their jobs and lose health coverage.

@The Moar You Know: The two weeks don’t have to come all at the same time. A long weekend here an extra day tacked on to another holiday, possibly a one week vacation and pretty soon your two weeks are gone.

Completely agree that two weeks vacation is far too little. People need breaks, especially longer ones. Again, it benefits our entire society.

Seanly

Wait, someone thinks that if you work 1500 hrs/yr you’re essentially healthy? Ummm, no.

KithKanan

@Seanly: No, you don’t have to be essentially healthy. Insurance mostly doesn’t deal with individuals, it deals with populations. The group of people who can/do work 1500 hrs/yr is, on average, going to be healthier than the group of people who don’t, because some of them aren’t working because of medical conditions that prevent it.

sheila in nc

@Yarrow: A major driver for and objective of the ACA was to create a better individual market as a precondition for weaning society off the need for employer-based and employer-subsidized insurance. It’s amazing that so many people didn’t understand that.

Yarrow

@sheila in nc: I understood that. It surprised me that ACA supporters didn’t use “it’ll increase entrepreneurship” as a tactic to sell it. Being stuck in a corporate job because you or a family member need that sweet insurance you can’t get elsewhere is something everyone understands. Lots of people want to take a chance on starting a business but can’t because of health insurance. Increased entrepreneurship that boosts the economy (“It’ll allow someone to start the next Apple or Facebook!”) should have been a top discussion point. It wasn’t and I still don’t really understand why. Corporate hold on our elected officials, I guess.

Ruckus

@Yarrow:

But it was sold as being better for people because they could open a small business. Which of course is competition for someone’s big business.

On the subject of 1500 hrs/yr if I work every hour I’m supposed to that’s 1250/yr. But I am semi retired, does that count?

Mart

@Yarrow: I heard the entrepreneurship argument softly peddled under the roar of DEATH PANELS. Hard to make sane arguments in this country.

Roger Moore

@Yarrow:

Health care should not be offered and purchased at all. It should be provided by the government for all citizens and legal residents and paid for by our taxes.

Elizabelle

@Roger Moore: Agreed.

And, in the meantime, I could see that ACA was designed to foster entrepreneurship; make coverage available for smaller businesses, even if an individual or family had some grave health issues.

David Anderson

@Seanly: As a cohort, people with near full time employment are healthier or at least code to have fewer and less severe chronic conditions than folks who buy their insurance in the individual market. A significant element of the individual market is working at or near full time as well but there is a proportion of that cohort which is unable to work near full-time due to health reasons and these folks are able to access non-underwritten insurance for the first time.

This is at the population level (100,000s to millions of people). At the individual level, there is wild variance.

Daniel Ludwinski

I looked at the data and I don’t see the state with a small group market coded as sicker than the individual market… are you sure this is right?

David Anderson

@Daniel Ludwinski: thank you, post and chart updated.

Stan Dorn

Another factor has been key since 2014: selection. The vast majority of otherwise uninsured people offered employer-sponsored insurance accept it. The same is not true of the individual market, where relatively healthy people are far more likely to take their chances and go without coverage. Why? It’s much more expensive to pay for individual-market than group coverage; and it’s much more work to sign up in the individual market, particularly if you want the subsidies that go along with marketplace coverage. Selection, coupled with measures to pool all risk in the individual market, has translated into higher premiums, on average, than are charged by comparable group coverage.

Increasingly, another factor is the availability of competing plans that operate under very different rules: farm bureau plans, health care sharing ministries, and now short-term and association health plans, under emerging Trump Administration policies. These plans siphon off good risks, leaving the remaining individual market with higher average risks, hence higher costs.

I wonder how researchers could tease apart the relative contributions of these three factors.

David Anderson

@Stan Dorn: Completely agree, the selection effect is massive.

I think the way to look at it would be to use IRS individual data to track when people get laid off/quit/fired from small group ACA coverage and see where they end up in the following month(s) if they do not elect COBRA. Under the selection story, we should expect the folks who went ACA individual market to have higher than average small group risk scores while the below average risk scores either went uninsured, short term plans or health sharing ministries. We would see HSM on the 1095 while the uninsured and STP would be a big question mark.

So who has access to the individualized IRS data that can then be mated to an insurer’s claims?