Georgia’s governor released a plan for a 1332 waiver. This waiver has two severable steps. The first is a reinsurance step. ACA reinsurance has a source of funds that are not derived from premiums cover some portion of claims. The external infusion of money means premiums don’t have to be high enough to cover all claims and all administrative costs. Instead, they just have to be high enough to cover some portion of claims and all of the administrative costs.

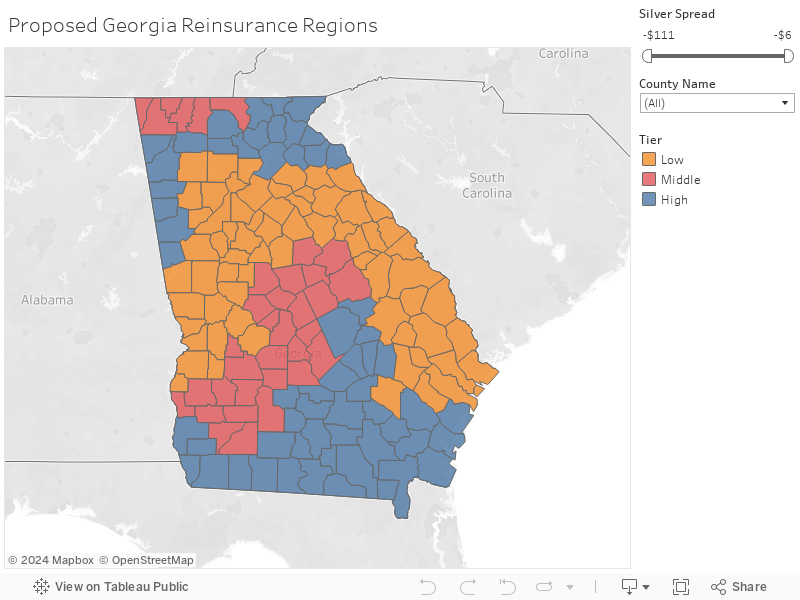

Georgia is proposing a reinsurance scheme that varies by geography. The health economists are going to love this, especially in rating area 13 as it provides a great source of variation and clean discontinuities. The policy objective is to bring down gross premiums in rural, expensive regions more than in urban and suburban regions. This is a valid policy objective. Colorado is running a reinsurance scheme similar to the proposed Georgia scheme for the same exact objective.

The other notable aspect of this proposal is the amount of claims that the reinsurance scheme is proposing to eat. The attachment point which is the claim value where reinsurance starts is only $20,000. That is a knee replacement or a somewhat complicated C-section. Many other states won’t start their reinsurance until the claims run to $40,000 or $50,000. And then the reinsurance program runs to $500,000. This is much higher than usual. None of this is bad. It is a lot of reinsurance.

Finally, the Georgia market has some significant premium spreads between the cheapest plan in a metal level relative to the benchmark premium. Big spreads are great for healthy, subsidized folks as they will see cheap net of subsidy plans. Small spreads push healthy subsidized folks out of the market as they are priced out. Regions with large, current spreads and high (80% coinsurance) will see much smaller spreads in 2021 than they do now. This will bring some uninsured and unsubsidized folks into the marketplace while pushing some currently insured and subsidized out. I argued in August that states have to make choices:

All states will face an environment of guaranteed issued, community‐rated, subsidized private market insurance, available Medicaid expansion for working‐age adults at an enhanced federal cost‐sharing and wide waiver authority that is constrained by law and clear administrative procedures. Within this framework, states will need to find ways to smooth the edges of the law and address issues and populations that are not well served by the law. They have the tools to do so, but the decisions to trade‐off the well‐being of some groups for the gains of others will remain a potent political and policy problem.

Georgia is making a choice.

Brad F

David

Can you review how the term “coinsurance” applies in the context of reinsurance?

Between the attachment points, is the payout 15, 45, and 80% contingent on the three tiers?

Thanks

Brad

David Anderson

@Brad F: Coinsurance is the pay-out percentage by the state.

For instance, lets assume that there is a $30,000 claim.

$10,000 is in the coinsurance range.

Low (15%) has the state paying $1,500 and the insurer paying $8,500 plus the $20,000 = insurer pays $28,500

Medium (45%) has the state paying $4,500 and the insurer paying $5,500 plus the $20,000 = insurer pays $25,500

High (80%) has the state paying $8,000 and the insurer paying $2,000 plus the $20,000 = insurers pays $22,000

p.a.

What, Georgia’s waiver is strictly abt reinsurance? No punitive work-to-survive rules or electrified hoops to jump through?

David Anderson

@p.a.: Georgia has three waivers out

ACA Individual Market 1332 A : Reinsurance (what this post is about)

ACA Individual Market 1332 B: Complete rebuild of the market for 2022

Medicaid 1115: Expansion to 100% FPL, premiums, work requirements and HSA like accounts (think Indiana HIP 2.0 combined with UTAH’s first waiver application)

David Fud

Could you comment on State Senator Jen Jordan’s twitter comments? I would like some verification that she is correct on her take if you could provide some insight. https://twitter.com/senatorjen/status/1191461133728833537

Thank you.

StringOnAStick

I’m wondering if there is data regarding at what cost level a medical event is most likely to cause bankruptcy, and if reinsurance is being designed with that in mind?

??? Goku (aka Amerikan Baka) ??

@David Fud:

I’ll add my desire for David to comment on that thread to yours

This was a reply to the Senator in that Twitter thread:

I’d like to get David’s opinion on this criticism as well. Thanks David for your informative healthcare posts!

Michael Cain

And yet, come the next Colorado legislative session starting in a couple of months, there will be members from rural areas whining that “the Front Range cities have declared war on rural Colorado.” Literally, some of them use the “declared war” phrase.

David Anderson

@David Fud: She is fundamentally right on the mechanics and implications. There is a large literature on administrative frictions that keep people who are eligible for a program out of a program. The Kemp waiver proposal has numerous barriers which an applicant has to successfully climb over or go around to qualify. The finances also work out as described.

Adrianna MacIntyre and I looked at limited Medicaid expansion in Utah: https://www.healthaffairs.org/do/10.1377/hblog20190212.230279/full/

David Anderson

@??? Goku (aka Amerikan Baka) ??: All or nothing is the law, or at least the law as interpreted by the two relevant administrations.

There is a shit ton of wiggle room on how it is implemented (waiver programs galore) but the funding is fairly straightforward.

Kent

This is kind of OT but I’m curious.

Would the M4A programs by Warren and Sanders completely eliminate Medicaid and all the state-administered insurance programs that are medicaid related but operate under different names?

Seems like a pretty compelling argument for M4A if it would eliminate all of this sabotage and “punish the poors” stuff that goes on in red states with the administration of these programs. We hear a ton of fear and loathing about how M4A would eliminate private insurance. But basically nothing (and least I’ve heard nothing) about how it would eliminate all the state-administered Medicaid programs around the country. Which is also probably a net plus in most red states but may be a wash in blue states that have mad real efforts to make it work.

David Anderson

@Kent: Over various time scales, yes; most if not all of Medicaid would go away.

ccswood

There were five public hearings to present both this waiver and the one dealing with Medicaid. It seems to me that the locations chosen were not logical if the intent was truly to solicit the most public involvement. There was one in both Macon and in Savannah. However, three others were in Rome, Gainesville and Kennesaw, all small towns north of Atlanta, two of which are in the blue reinsurance regions on your map. The last was in Bainbridge (also blue on your map), population 13,000, which is located in the most extreme SW county in the state. That location, while an hour away, was the closest to me in Albany, the major city of SW GA with a metro area population of 157,000 and a seemingly better place to hold the meeting. There were no hearings at all in Columbus, Athens, Augusta or Atlanta.

I did not attend the “closest” meeting but I ran across this article which goes over the 1332 waiver request in pretty good detail.

https://www.healthaffairs.org/do/10.1377/hblog20191105.878300/full/

Kemp proposes to eliminate access to the Federal ACA website and will direct everyone to multiple profit minded websites run by brokers and insurance companies. Websites will offer both ACA compliant and non-compliant plans, hopefully clearly marked and quality rated.

“Georgia believes that this decentralization of enrollment (i.e., a shift away from a single platform like HealthCare.gov to multiple enrollment channels) would promote competition, improve customer service, and drive enrollment.” Because this certainly seems easier than the “poorly run” HC.gov site!!

Subsidies will be state specific and may not match the feds after the first year. Georgia’s contribution to these funds will be subject to the whims of the legislature. A good portion of Georgia’s contribution will also have to go towards back end administrative functions now performed by the feds.

“The state could amend this subsidy structure in the future based on actuarial analysis, funding levels, and enrollment.”

“However, Georgia would cap its contribution towards the Section 1332 waiver on an annual basis. Unlike in the current individual market, this cap could result in waiting lists even for individuals who qualify for subsidies. Georgia notes that subsidies will be granted on a first-come, first-served basis until the state’s funding cap is reached. If there are a larger number of subsidy-eligible residents than expected, those individuals could still enroll in coverage but would be placed on a waiting list for subsidies (meaning they would pay full premiums even though their income would qualify them for subsidies under the ACA).”

So, just because you qualify for a subsidy does not mean that you will actually get one? Each Nov 01, all of us are supposed to duke it out for the available funds? How much time will they take to notify you as to whether you qualify? Guess that you might have to be prepared to quickly cough up another $1000 per month (if you are old and poor) or move out of state?

Hunger Games and medical emigration?? Disrupt 450,000 in order to add only 30,000 additional insured? And they call this the Patients First Act?