One of the challenges of choosing health insurance in an open enrollment period when the menu of choices is somewhat lengthy is avoiding dominated plans. A dominated plan is one where on all relevant to the decision maker characteristics it at best ties and typically loses to another option. Choosing a dominated plan means that you are choosing a plan that is objectively inferior to at least one other option. An inferior plan means the insurer will make more money from you compared to an optimal plan choice.

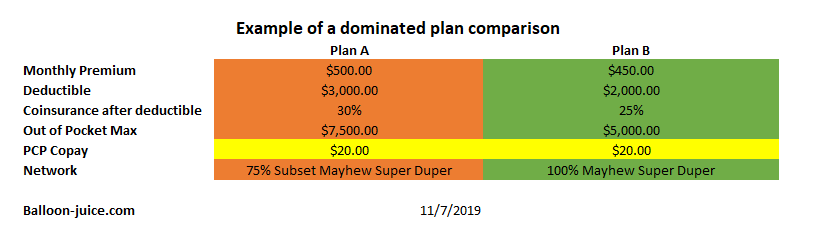

I will show an example below of Plan A being dominated by Plan B on a few characteristics:

Plan B beats Plan A on premium, deductible, coinsurance rate, maximum out of pocket and network. Plan A ties Plan B on PCP co-pay. A full domination plan analysis will probably look at more characteristics than those, but this is the short toy example of what to look for when thinking about a plan being dominated.

In the ACA, the creation of well defined, and mutually (or mostly mutually) exclusive metal bands would make unsubsidized dominated plans a rare event. From 2014-2017, subsidized dominated plans are easier to see as one could expect a company offer two Bronze plans priced significantly below the benchmark Silver plan with significantly different deductibles but otherwise identical cost sharing structures both be priced at zero for a particular subsidized buyer.

From 2018 to present, due to silver loading for CSR funding termination, dominated plan offerings are likely to be more common within a particular company in a particular region as gold plans are frequently priced underneath silver plans. In some regions, gold plans can have zero premiums after subsidies for large populations. As long as the benefit design is not too funky relative to silver and bronze plans, gold plans can readily dominate bronze and silver plans for subsidized buyers in certain regions.

So when you are looking for plans in either Medicare Advantage, Medicare Part D drug coverage or the ACA exchanges, look hard at dominated plans. And if you find one, avoid it.

thylacine

“Dominated” is also the term used in game theory, when one strategy is better than or equal to another no matter what the opponent chooses.

David Anderson

@thylacine: PRECISELY —

There is an emerging econ/policy literature on dominated insurance plan choices that is currently focused on Medicare Part D, Medicare Advantage and employer sponsored insurance within a firm. The ACA markets offer a new data set with a very different population.

BC in Illinois

At first, I read the title as “Beware of Dominated Plants.”

I was expecting a garden feature.

I need another cup of coffee.

stinger

Thank you, David. I’m so glad you post here. Interesting and often directly useful information!

David Anderson

@BC in Illinois:

I’m seeing if I can put together a project team to look at dominated plans in the ACA together. I have a project folder on a Google Drive titled “Dominated Plans.” Since that file went up, the ads that I am getting served have gotten quite… shall I say …. interesting

Wayne

I’m confused as to why I would not pick the Mayhew Super Duper plan, or does it mean I should continue looking?

David Anderson

@Wayne: Mayhew Super Duper is the network. Plan A only has 75% of the providers from Mayhew Super Duper while Plan B has all the providers in Plan A plus some more for the entire Mayhew Super Duper network… Plan B has better potential access so Plan B wins on network.

Kelly

I discovered a Obamacare marriage penalty this week. My brother recently retired and I’m trying to help him navigate Obamacare. His wife is on Medicare but he is too young. His subsidy is about a third of what it would be if the were both of Obamacare age instead of the half I naively expected. That’s several hundred dollars a month. A glitch I suspect would be fixed by now under Democratic Party domination.

wvblondie

I’m confused. In the example you give, why would anyone pick Plan A? Or is it that in the real world (or as “real” as insurance companies ever let it get) it’s harder to identify dominated plans?

David Anderson

@wvblondie: No one should pick plan A. Lots of people do pick Plan A

Butch Fries

The Exchange site is infuriating. We’re being required to show documentation for information that hasn’t changed from prior years. In one case, for example, we were told the USPS lists a different address for us than what we provided. The USPS address shown is exactly identical to the one we listed, and yet we’re being forced to explain this “discrepancy.” Also required to provide copies of SS cards and prove citizenship, even though this isn’t the first time we’ve used the Exchange. I hates it.

daveNYC

@David Anderson: Any numbers on how many do and why they do so? Some probably aren’t paying attention are just aren’t that bright, but I’ll bet there’s shenanigans going on too. Pick Plan B then next year Plan B is transmogrified into Plan A and anyone who just reups is boned.

David Anderson

@daveNYC: I don’t know that answer yet, trying to get a research team together for an answer.

ProfDamatu

@Butch Fries: Ugh. And I got a letter from the Exchange claiming that I hadn’t filed a tax return with the APTC reconciliation form for 2018, and that I’d better clear it up with the IRS right away or risk losing 2020 subsidies.

Except that I’m pretty sure that the IRS can’t possibly have actually told them I didn’t file my taxes with APTC reconciliation, seeing as how, though I did get an extension, I received my tax refund check weeks ago, and a double-check of my e-filing shows the reconciliation form right there, plain as day. Obviously the IRS *does* think I’ve filed my taxes! SMH