The Center for Medicare and Medicaid Services released their draft actuarial value calculator a few weeks ago. This calculator is how insurers determine which metal tier (bronze, silver, gold, platinum) a plan can be placed in. The calculator refers to a series of reference tables that are derived from national experience and pricing levels to estimate how much a particular benefit configuration. Benefit designs are constrained by the allowable maximum out of pocket limit.

In 2021, the estimated allowable out of pocket limit is $8,700. This limit is calcualted by taking the previous year limit and adding the percentage of premium growth of a set of index premiums. If premiums go up by 5% then the allowable out of pocket limit goes up by 5%.

A plan with an $8,700 deductible and an $8,700 out of pocket limit will have an actuarial value of 61.06% which means, on average, the insurer will pay 61.06% of the entire pool’s allowed, essential health benefit claims while patients in the form of cost sharing will pay 39% of the claims.

In 2014, the minimum plan had an actuarial value of just below 58%.

As trends continue, insurers won’t be able to build standard (58-62% AV) Bronze plans by 2024. They won’t be able to build Expanded Bronze plans by the time my daughter graduates from college.

Why is this?

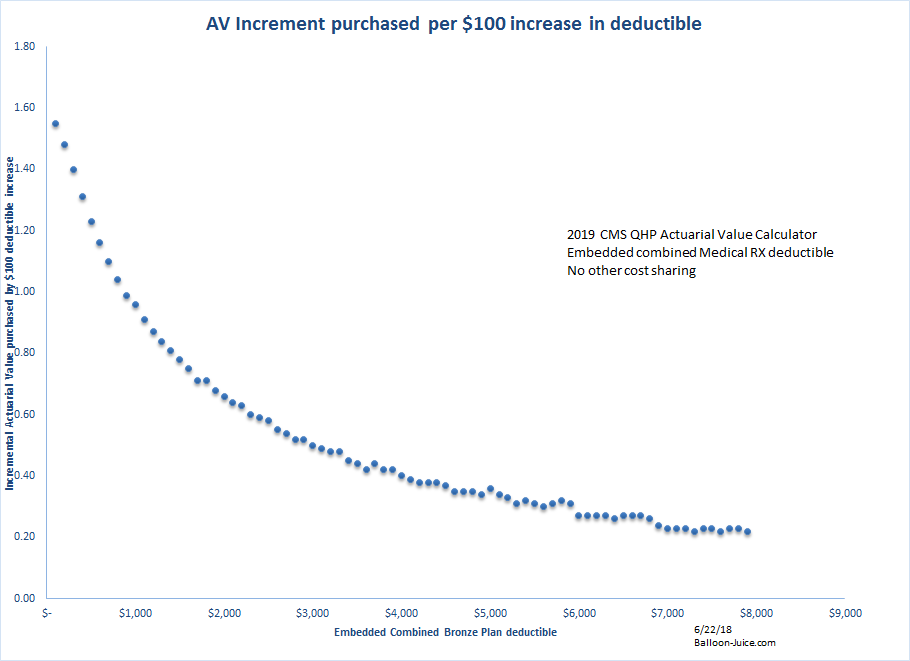

The marginal value of another $100 of added deductible declines fairly rapidly. To hold AV constant, maximum out of pocket limits have to increase significantly faster than premium increases. We looked at this on Balloon-Juice in 2018:

health care costs are so skewed to the right. Half of the population barely touches the system so the first $100 of deductible captures most of their health care spending and the first $500 of deductible is almost entirely their annual spend. The declining marginal purchase of AV per $100 spent on deductible is real and big.

By the time the deductible is going from $3,000 to $3,100, very few people are actually running up charges to that level. It buys half a point of actuarial value for this jump. By the time the last $100 is added to deductible for the skinniest plan possible with a $7,900 out of pocket maximum, the AV bought is .22 points…

Why does this matter?

Subsidized buyers care about the spread between their preferred plan(s) and the benchmark. A Silver plan under current rules can have a 66% AV. As the minimum Bronze creeps upwards in actuarial value, the spread becomes tighter and tighter. The vast majority of individual health expenditure profiles will make people fundamentally indifferent on cost sharing between a 59% Bronze and a 62% Bronze from the same insurer with the same network. The difference then would be the net premium which is a function of premium spreads and premium spreads are a function (holding everything else constant) of the actuarial value spreads.

The incremental buyer on the ACA exchanges is someone who is flipping a coin to get insured or not insured and the decision is health insurance or paying off a credit card a little faster. The incremental buyer is relatively healthy and they are not buying on the basis of plan characteristics beyond net to them premium. As a minimum Bronze increases in actuarial value, the probability of an incremental buyer seeing a zero-premium plan decreases. This will knock down enrollment and increase the average risk and therefore average non-subsidized premium.

The end of the Bronze age is not a 2021 problem, but Congress and regulatory entities need to start thinking about how they want to deal with this when it becomes a 2023 or 2024 problem. One of the most straightforward solutions is to rejigger the out of pocket maximum limits to correspond to a targeted minimum actuarial value so that low end Bronze could again be a 58% AV plan with perhaps an $11,000 out of pocket limit.

WaterGirl

I was hoping that ‘The End of the Bronze Age” would be a hopeful article announcing the end of the Trump Era.

Too much to hope for, I guess.

rk

@WaterGirl:

That would be the end of the orange age.

WaterGirl

@rk: Unless you take into consideration that he may be using a “bronzer” as his base makeup. :-)

Sorry, David, for filling your thread with this instead of something in response to, you know, the actual subject of your post.

My only excuse is that I have been in an unrelenting terrible mood since the NH vote.

Butch

But really isn’t the problem that nibbling around the edges of the ACA won’t fix the fundamental issues? People are already buying insurance based on bullet points listed on a balky website, and the out of pocket limit is a fiction. Spouse’s Bronze plan would really do no more than slightly delay bankruptcy if something major happened, because Blue Cross sets a whole bunch of different deductibles, including $13,500 for anything the insurer considers out of network or “unusual” (and you’ll quickly discover that there is nothing so routine that it can’t be classified as “unusual”).

guachi

And if Congress legislates an increase in Out-of-Pocket maximums it’ll be a hard sell. Easiest way to do that is not sell it at all and just do it while rolling in something else useful to whatever bill passes.

Aardvark Cheeselog

Sigh. The Boots Theory illustrated.

David Anderson

The point I will be making is that a zero premium plan with an $11,000 OOPMax, negotiated prices and some pre-deductible services is superior to the following options:

a) a non-zero premium plan with a $8300 OOPMax negotiated prices and some pre-deductible services

AND

B) a zero premium plan with an infinite out of pocket max (at least until bankruptcy courts intervene, non-negotiated prices and no pre-deductible services

Those are the choices that a marginally attached individual is making when they enter or not enter the ACA insurance market.

Robert

The big picture – medical prices continue to rise much faster than overall inflation, while wages continue to fall behind. All other things being equal, David makes reasonable points which are likely to be anchored in the reality of what can be accomplished politically. But the bigger take away is the medical industry (and university systems) are pushing an unsustainable path – this has been known for a long time but the end game of pushing more people out of the middle class is finally coming into eyeball view (as opposed to being a simple calculation). If there were any easy answers those would have been tried, so buckle up.

daveNYC

@David Anderson: I get that you’re talking about a very specific scenario, but when the solution is to up the out of pocket maximum by around 30%…. wooof.

TC

The ACA cannot fix our healthcare system. Not even with armies of Davids paid to analyze data to create papers, charts and graphs all in attempt to bend the cost curve and educate the public. This problem can only be solved politically via government managed healthcare.

Universities, Think Tanks and government agencies spend hundreds of millions trying to figure out how a profit driven opaque market can show real progress on this issue before the pitchforks come out. Meanwhile, Insurance companies suck hundreds of millions more out of the system leveraging the sheer size, complexity and controlled chaos of our current profit driven healthcare system. Millions more are made in the healthcare debt collection industry (my son worked in that) to squeeze the unfortunate few of their last dollars.

Multiple Millions more are spent by employers to manage these health benefits – that’s my industry. I provide HR Software and related consulting to businesses and non-profits to manage their employees benefits, COBRA, 1095 reporting (ACA requirement). I’ve made a comfortable living (I’m the 10%) for 20 yrs now. For example, SHRM (Society of Human Resource Management) estimate the cost for an employer to enroll an employee each year -collecting, sending data, communicating to the employee each year how the benefits changed as mandated by the ACA- is $70 per EE/yr. There are about 130M FT employees in the US. I’ll leave the math to the paid experts

ProfDamatu

@David Anderson: I see your point. regarding choices in this narrowly-defined enrollment decision, but fundamentally – we need to do something about cost-sharing for ACA enrollees who don’t qualify for CSR subsidies, and that “something” shouldn’t be “raise it even higher.” Don’t get me wrong, the ACA saved my life, but within a few years, none of the plans available to me will be affordable to use even just under current trends (unless Optima gets religion and starts dramatically Silver Loading, and even then….). This year, there was only one plan with a network that included all of my doctors with a deductible below $3000. (I actually ran a spreadsheet with all of the possible choices, including coinsurance, deductible, and OOP max, and looked at how much I’d spend for allowable charges ranging from the amount I racked up in 2019 (about $6k, which is about the minimum I’m looking at in a year with two followup MRIs) up to $30k – I was curious where the “Bronze is a better deal” point was – so I’m more familiar than I ever wanted to be with the tradeoffs.)

It’s just scary to think that within a few years I could be paying my 9.8% of income for a plan that pays nothing until I kick in a deductible of $4000 (which is itself over 10% of my income most years). I realize that most people on the ACA never touch the medical system, and that the answer may be “get a job that provides insurance, or don’t get sick again” but cost sharing really is getting to the point of cruelty for anyone unfortunate enough to have medical issues but who is too “rich” to qualify for CSR help.

ProfDamatu

@ProfDamatu: And – thank heavens my cancer experiences were back when it was still possible to find an affordable-premium plan with an OOP max of $3000 or so! (Only 4 and 6 years ago, for those counting at home!). I hate to think where I’d be now if, instead of shelling out a total of about $6k out of pocket for both cancers, I had instead had to cough up a total of $16000 out of pocket (as would now be the case).

BigMango

Mitchell and Webb Bronze age introduction..lol

https://www.youtube.com/watch?v=nyu4u3VZYaQ

joel hanes

I’m sorry, David, but for me the sum of all your wonderfully thoughtful pieces has been to inspire in me a burning moral rage at the entire institution of for-profit health insurance.

Perverse incentives have produced perverted institutions.

Odie Hugh Manatee

I remember when insurance actually used to pay some of the bills. Over the last three years my wife and I have spent over $12,000 for medical expenses without the insurance paying out a single penny. Our insurance is through her employer and it’s managed by BC/BS. The worst part is that they don’t count everything that we have to pay towards the deductible, which really sucks.

It’s basically a catastrophic coverage plan at this point and we get to pay for everything else until the catastrophe.

Odie Hugh Manatee

@Odie Hugh Manatee:

That $12K was over the last three years, btw…