Today the Affordable Care Act is 10 years old. The individual market has price linked subsidies that are tied to the silver benchmark. Individuals who buy a plan that costs less than the benchmark pocket the savings. Plans are partially community rated in that the same plan is priced the same for everyone of a given age and smoking status. Prices can not vary for health conditions. However, prices can vary up to 3:1 for age. A 21 year old will pay one third of the premium of a 64 year old on the same exact plan.

For individuals who don’t qualify for subsidies, this makes plans much more attractive to young people than old people.

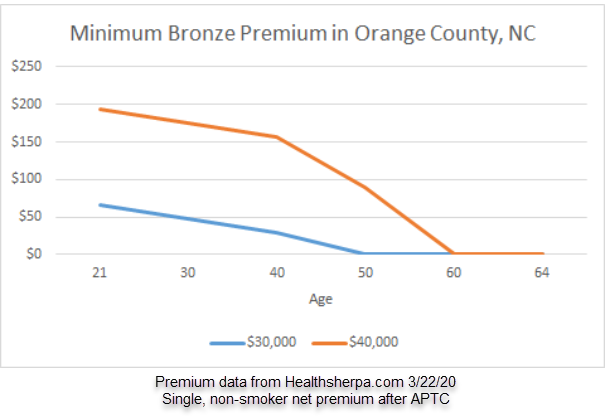

However, the subsidy mechanics invert the attractiveness for individuals who have subsidies. The age ratchet makes premiums for subsidized old folks much cheaper than premiums for subsidized young folks. The chart below is the cheapest premium in 2020 for a single, non-smoking individual in Orange County, North Carolina. The blue line is someone earning $30,000 and the orange line is for someone earning $40,000. The horizontal axis is age of the buyer.

The first thing to note is that the net of subsidy premium for the cheapest plan is lower for the individual with lower income irregardless of age.

However the second thing to note is that an individual earning $30,000 a year is paying $66 per month at age 21 (2.6% of income) for a high deductible Bronze plan while a 50 year old earning the same amount of money is paying nothing. Bumping incomes up to $40,000 per year, a 21 year old is paying $194/month (5.8% of income) while a 50 year old pays $90/month (2.7% of income) and anyone over 58 has a zero premium plan available.

The age ratchet lowers net of subsidy premiums for plans priced below the benchmark faster for older individuals. Older individuals are more likely to already value having health insurance while younger individuals who are relatively healthy, are rather indifferent to health insurance as a general statement. Higher costs are a barrier to enrollment that is more significant for younger individuals.

Reworking the subsidy formula so that younger and relatively healthier individuals see cheaper premiums than they currently see for below benchmark plans would reduce adverse selection among the younger population. It would increase uptake and also reduce risk and variance within the risk pool which would lower premium levels for the entire risk pool.

lurker3000

As an older subsidized person, I’m grateful for this IRL. But yeah, leveling out the premium pain would make insurance more palatable to the ever invincible youth market. Maybe. On the other hand, based on beach behavior recently, maybe the health risk is part of a thrill incentive to gamble vs think logically.