A dozen states currently have a Section 1332 reinsurance waiver for the ACA individual market. There are two flavors of waivers with significant variation in local implementation. The first type of reinsurance waiver is the “designated disease” waiver where the state reinsurance pool covers the medical expenses of individuals who qualified for the pool on the basis of a limited number of diagnosises that are known to be high cost and non-random. Alaska and Maine have waivers set up like this. The other method is an “attachment point” method. In this reinsurance choice, states will pay a percentage of the claims once claims reach a minimal number (commonly somewhere between $30,000 to $50,000) and a cap.

In normal times, these two methods are “potato” and “potatah” ways of injecting non-premium dollars into the payment pool. These two choices eat slightly different types of risk but they are reasonable choices for states to make. Non-premium dollars are a combination of state funding and pass through dollars from the federal government. The pass through amount is the result of lower subsidies and it is a fixed amount. States are the ultimate risk holders if their obligations are more than projected, there is no federal backstop.

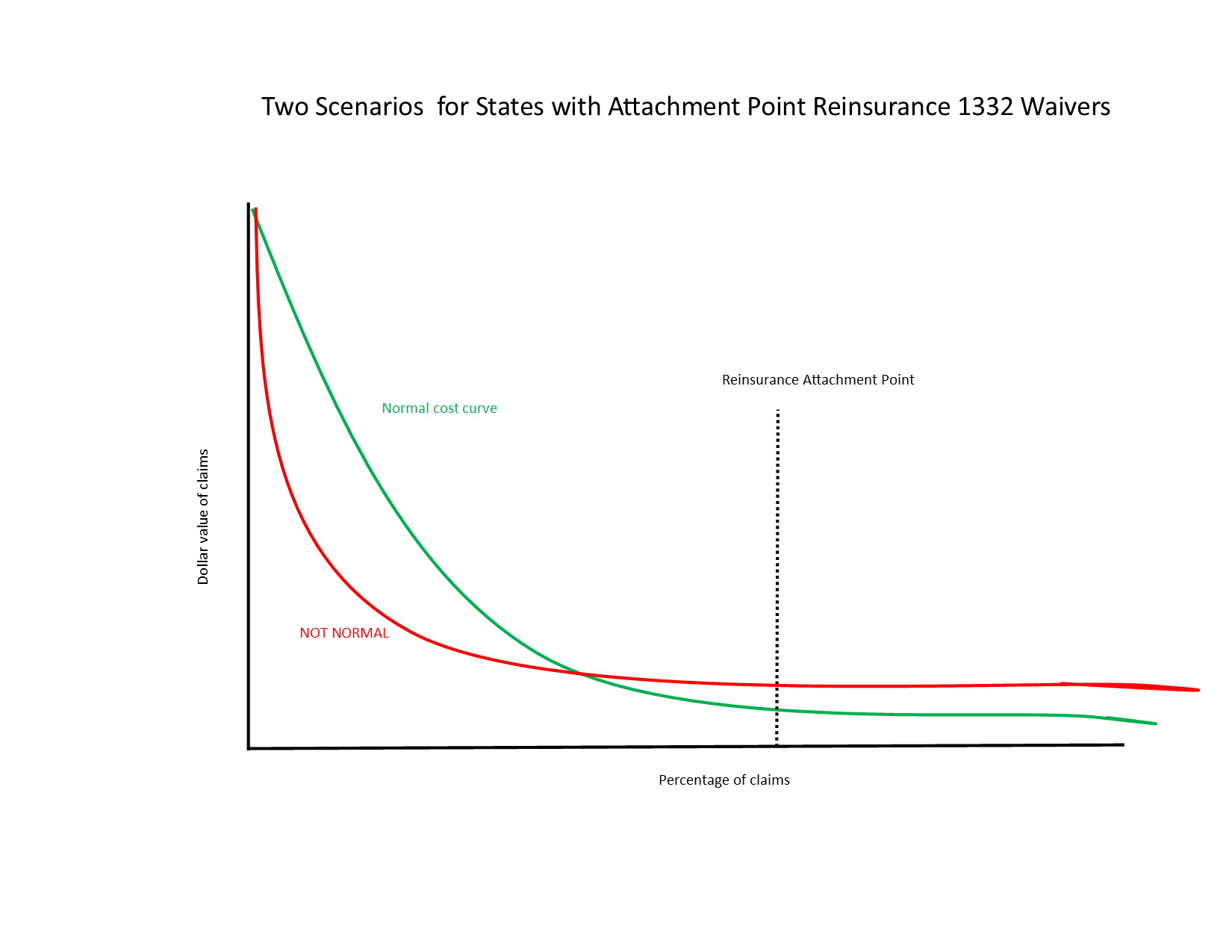

These are not normal times. States with attachment point reinsurance programs could be facing an unusual and unprojected claims curve.

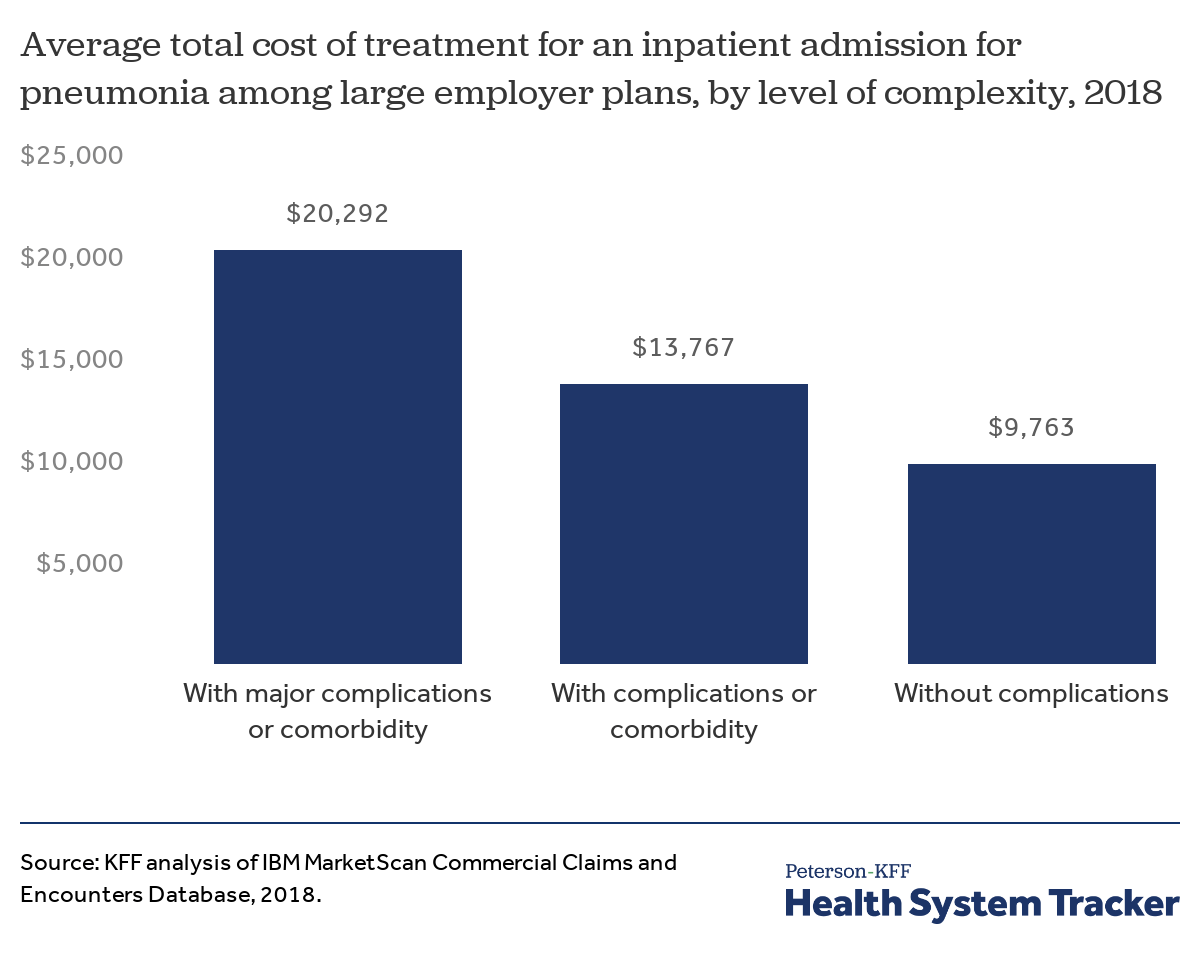

Kaiser Family Foundation is projecting that the average hospitalization for someone with COVID19 with complications could readily be over $20,000

An average claim that comes in at $20,000 won’t trigger a reinsurance payment. Some claims will be less expensive than average. Some will be more expensive than average. If the distribution of expensive claims are heavily skewed to the right of average, a lot of unexpected claims would begin to bump into reinsurance territory.

Statesbuilt their program budgets on the assumption of a normal experience year with lots of low and medium dollar claims and few big claims. Insurers priced their premiums on similar assumptions regarding reinsurance payments. A bad COVID19 month could put a lot of people into the ICU with high cost claims that don’t displace too many other expected high cost claims as those claims are likely for cancer, or other must treat conditions. This will be especially true for conditions that are mostly treated with specialty drugs so these patients don’t need nor compete for inpatient admission beds.

In the red line scenario, the reinsurance fund has much higher levels of obligations even if total medical spending is constant because the shape of spending has changed. A lot of low dollar utilization will either disappear or be displaced to next year while higher dollar claims that qualify for at least some reinsurance could be more common. In that scenario, the state, as the ultimate fiscal backstop, would need to find millions more dollar above budget in a time when all state discretionary funds are extraordinarily constrained.

rikyrah

Block grants are a scam and a fraud??

Ang

So if I am understanding this, the states that used the attachment point method are likely in deep and desperately hoping that either the current COVID bill or one in the future will rain money on them. Considering the deep animosity many on the R side have towards Medicaid, the ACA, and the people who rely on such things, that seems quite worrying.

David Anderson

@Ang: It depends. Some of the states have escape clauses written into their waivers where the states can change the attachment point or pay-out rate to fit the budget. States that don’t have escape clauses may be in big trouble depending on the number and distribution of spending of cases that go into the ICU.