Yesterday, I mentioned that insurers can’t rely on the assumption that 2021 will look very similar to 2019 in terms of population health and usage patterns. There are too many fundamental unknowns that are being caused by the COVID-19 pandemic. Insurers are comfortable handling statistically quantifiable risk. This is risk that has an expected distribution pattern and predictable outcomes even if there are extreme tail risks. An insurer is more than willing to back a $1 billion dollar prize for a small premium if the prize is awarded if a 40 something male with bad knees can run a sub 2 hour and 10 minute Boston Marathon after 2 years worth of training. That is a quantifiable risk that is extremely unlikely to require a pay-out. Insurers hate uncertainty where they can not even think about quantifying reality.

Insurers within the ACA market space have two major types of responses in the face of significant uncertainty.

The first choice is to not take on uncertainty. This means insurers leave markets. We saw this in the run-up to 2018 as insurers did not know what the rules of the road were going to be. Some insurers looked at Repeal and Replace as well as the potential termination of CSR payments and decided that they could not afford to risk the company on the basis of policy uncertainty. Going into 2018, about 42% of the counties in the country were monopolies. These monopolies were more likely to be in rural regions. Monopolies are not necessarily bad as Coleman Drake, Jean Abraham and I showed in a recent Health Affairs article. Monopolies with smart silver-gapping strategies can lead to low net of subsidy premiums for subsidized individuals.

The other choice for insurers when they see uncertainty is to raise rates. Covered California has a scenario that sees a 40% rate increase for fully insured lines of business next year. If a company jacks up rates too high, it is a low enrollment, low risk year especially if risk adjustment is directionally decent. If a company does not increase rates high enough, they will get all the price sensitive enrollment at premium levels that are too low. This logic dominated early rate filings in 2017 when insurers were trying to figure out what was going to happen with Repeal and Replace as well as CSR payments for 2018.

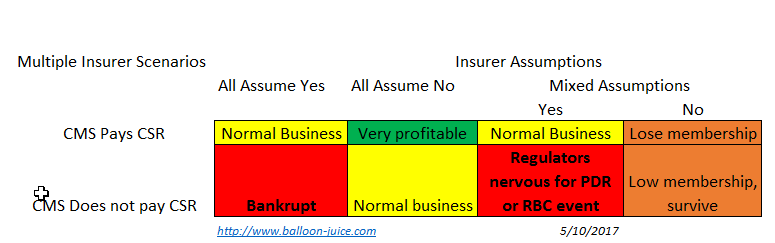

But things get a bit odder when all carriers agree but get the government action wrong. If the carriers think the government will pay but the government does not, the outcomes are unequal. The carrier with the absolute worst value proposition is not hurt that much. No one wants to buy that product anyway. It is a minor hit for an ugly plan.

Now if a insurer offers a very attractively priced plan with a good network and good customer service, they attract all of the membership. That usually is a good thing! Not in this case. Offering the most attractive plan means that plan takes all of the losses. And if that plan goes under, the special enrollment period refugees will choose the next most attractive plan, sending it under. This is an odd winner’s curse scenario.

If there are multiple insurer and they disagree the dynamics are interesting. Insurers that assume they won’t be paid CSR always survive. They won’t get much membership as they are massively overpriced for the market. They will keep some portion of their sickest membership so they will be net risk adjustment recipients and their administrative costs relative to premiums will be very high. But they survive.

In this split decision making scenario, the carriers that are optimistic that CSR will be paid are in an all or nothing scenario. If they are right and the government pays CSR, they get almost all of the membership in the market. Assuming they priced appropriately, they should make good money for the year. If they guess wrong and CSR is not paid, they get all of the membership and the state regulators shut them down due to either a premium deficiency reserve (PDR) event as they have to come up with an extra 20 points of actuarial value that is not being compensated by the government, or there is a risk based capital problem as they have too many members to be safely covered by their current reserves

The COVID-19 pricing problem is structurally similar to the CSR termination pricing problem from the Spring of 2017. The safe, don’t lose the company bet in a multi-insurer market is to price really high.

Assuming that my logic is right that CSR uncertainty is an isomorph of the COVID19 pricing problem, we should expect a significant increase in both premiums and single insurer counties in 2021.

Gin & Tonic

I’m going to use this thread for a sort of personal question. As some may know, my son has been living overseas since last fall, and probably will not return to the US until near Labor Day. He is on a fellowship now, and does not have employment for his return. Now I’m reading that the Trump admin is essentially closing access to the Obamacare exchanges, but my state has a SEP open until April 15. Given the uncertainty, should he enroll in an ACA plan using my home address (which he is using as a mail drop now anyway) or wait until he returns to the US and enroll then using his return as a “life event” – if that is even possible then? Subsidy or not isn’t really an issue, we can help him pay, I just don’t want him returning to the US un-covered.

Butch

We’re in a rural monopoly area (one “choice” of insurance companies) and I’m wondering – can a monopoly company pull out of an area if there’s too much uncertainty? That would leave us with no options.

Another Scott

I know it’s unknowable at this point, but how would a federal Stage 4 rescue package that includes payment for COVID-19 treatment (as many good folks in the House have argued it should) figure into the Obamacare insurance pricing calculations? Sure, it depends on the details, but could you blackboard/flowchart the thinking? (Say a bill is active on June 1, if the timing matters.) Would it affect unsubsidized ACA enrollees? Stuff like that.

It might be a good cudgel in arguments for our Representatives and Senators to pass such a thing.

Thanks.

Cheers,

Scott.

David Anderson

Inter-state move is a qualifying life event. He can get covered in September through normal procedures

David Anderson

@Butch: They theoretically could pull out of an area, but another insurer would walk in and offer benchmark plans for $5,000 per 21 year old and cheapest Silver plan for $4,500 per 21 year old and get a firehose of federal money as everyone would choose the free to them silver plan.

Folks making more than 400% FPL are truly hosed though but the business case for a jack up premiums so high that nose bleeds look like the Mets locker room from the mid-80s while aiming to only enroll subidized buyers is iron clad.

I will post on this tomorrow

Gin & Tonic

@David Anderson: Thanks. I’m assuming that was to me. I’m also assuming if inter-state move is a QLE, an inter-country move will also be one?

piratedan

as an insurance rated aside, we’re now seeing insurance carriers now determining to not pay for clinical tests performed at hospital laboratories, now insisting that they be performed at outside laboratory entities…

think of it this way, your local hospital system (say a regional entity that is either affiliated with a religious founding sect or a group of suburban hospitals serving a mostly middle class constituency or whatever chain of entities you wish to imagine) is now no longer going to be reimbursed for the laboratory work that they provide based on a decision by insurance carriers.

They are dictating where your lab work will be done, likely adding days to a turnaround in that data getting to your PCP.

David, do you have any idea on what is driving this?

Butch

@David Anderson: Thank you, David! I will check in. Our premiums are already pretty high even with subsidy.

piratedan

@piratedan:

the scenario I am describing is if you’re seen at an outpatient clinic to get work done, be it at the behest of a Dr. Office, an employer or for some other reason; insurance companies are now stating that they will not authorize the payment of those lab services if they are not performed at a provider of their choosing.

Which strikes me as just a bit beyond their scope

Raoul

I saw the headline about possible 40% premium spikes the other day. Eye popping. It’d mean something like an extra $2,500 a year in premium for me. It really does seem like our kludged-together insurance system is going to be sorely tested by all this.

I don’t feel super inspired that Biden wants to more or less keep what we have (and yes! I will vote for him. I just think we will all need to use as much leverage as possible after he is in office to disabuse him of this system. Employment-based coverage when 10.4M people lose jobs in two weeks is bananapants.)

Another Scott

Relatedly, Dean Baker at CEPR – Getting to M4A Eventually:

Cheers,

Scott.