Massachusetts is running a general COVID-19 special enrollment period. Late last week, they released an interim enrollment report.

Forty days into the COVID SEP (which began on March 11, 2020, and runs through May 25, 2020), approximately 8,300 residents have used it to enroll in a Health Connector plan. To date, COVID-19 SEP enrollees comprise 6,800 families representing 8,300 people.

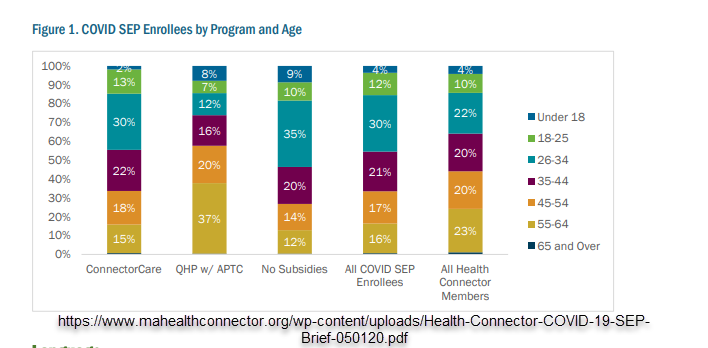

More interestingly, to me, is the mixture of folks who are signing up for coverage.

The two right most columns are the columns I am interested in. The All COVID SEP Enrollees seem to be significantly younger than the current Mass Health Connector enrollees. Younger enrollees (all else being equal) are likelier to be healthier than older enrollees for both general health/age reasons and the ACA subsidy math makes low cost plans less valuable to younger enrollees than older enrollees.

Will the younger enrollees who are coming into the risk pool due to an attention/information/revaluation shock of a global pandemic stick around. They had a revealed preference of either in-attention OR valuation that insurance was not a good enough value relative to premiums to not enroll last November and December, but does a pandemic increase the salience and value of any insurance versus no insurance? I would suspect that is mostly a yes.

If these folks do stick around, they should lower the average risk and thus the average gross (pre-subsidized) premium by a smidge. This is one of the many questions that actuaries are trying to figure out right now as rates are being prepared for 2021.

FR

I’m one of these folks. After I left my charter school administrator job, I started freelancing consulting. I had a great and expansive health insurance while working in schools, so before I left, I did every potential test and went to specialists check-ups on previous issues as well as some nagging stuff.

My thought process is that any insurance on the marketplace that I would be able to afford was only going to be useful for long-term stuff, which I figured I’d get very quickly if things looked dicey. COVID was a kind of “protect myself” moment, so I got cheap insurance with some subsidies. I’m unlikely to keep it though – but that’s because I’m going to grad school and I’ll jump onto that policy

Brachiator

I also wonder if younger enrollees are single or married, and with families.

Before the pandemic, I would say that for younger people, not getting insurance was a rational choice. The odds of them getting sick are low. But I also wonder how many younger people would opt out of private employer plans, and the average cost of those plans compared to ACA marketplace premiums.

David Anderson

@Brachiator: In most cases, I would strongly lean in your direction, but there are quite a few zero to very low premium plans available so the value proposition is fuzzier.

Yutsano

@David Anderson: We’re also talking about Massachusetts, which does still have its state mandate in place. So some of the purchasing could reflect that as well. Unless that’s in the packaging and I’m missing it. Which is entirely possible as I’m still quite in bed.

Brachiator

@David Anderson:

You’re absolutely right. This is totally anecdotal, but most of the single people in places I’ve worked think about health insurance as either/or propositions. Unless they are compelled to consider coverage because of marriage or children, they never look into coverage or compare costs, even if there are zero or low cost plans available. Thinking about health insurance, unless necessary, is just a nuisance.

By contrast, they will seriously look into and ask about auto insurance.

Same process, but motivation and necessity leads to different results.

Yutsano

@Brachiator: Not to mention car insurance is also mandated pretty much everywhere in the US now. We had that with health insurance until the Republicans screwed that over. Granted the mandate enforcement was strange* but it was at least an attempt.

*So the IRS could charge the mandate but not enforce it…yeah that didn’t exactly work as intended. You should see the machinations we had to go through just to suspend that from being enforced!

different-church-lady

David, I hope you don’t mind my once again hijacking one of your threads with a tangential. This is a follow-up to one of my earlier hijacks, and this seems like a good thread to do it in, since it’s both Massachusetts and ACA related.

In a couple of previous posts I was fretting about my pending hospital bill for a five-day stay treating what was probably bacterial pneumonia (Although some of the doctors were so certain from the get-go it was COVID-19 that even after both tests came back negative they acted like they wanted me to pretend it was anyway!)

I am right on the edge of subsidies. I have what is the most lightly subsidized plan in Massachusetts — a few thousand more dollars of income and I kick up into Silver.

The thing I was fretting over a couple of weeks ago was getting an Explanation of Benefits that made it appear as though no part of the bill would be covered by insurance.

After about 10 days of background anxiety, the bill itself arrived.

Sticker price: around $8500

My share: $250

And from this point on if anyone says a bad syllable about the ACA they are going to get an earfull and a half from me.

(Congrats to Redshift who pretty much nailed it with, “… I finally got a helpful person at the hospital who said “unless we send you a bill, don’t worry about it, we’ll deal with it.”)