Insurers in most states have tremendous amount of flexibility. Their plans need to be approved by state regulators but the regulators are often looking for network adequacy (are there enough doctors/hospitals in the local network), actuarial soundness (are the premiums sufficient to cover claims and not force the company to fail), and then there will be checks for actuarial value which is a standardized calculator that CMS publishes, and a few other secondary concerns. Some states like New Jersey have fairly restrictive cost sharing rules that insurers can maneuver within to get to a desired actuarial value. However, most insurers in most states can design their plans’ cost sharing with minimal restrictions.

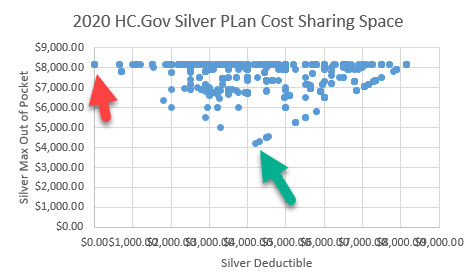

This is important as there is tremendous functional space for insurers to maneuver around in. I’ve pulled up every non-CSR silver plan sold on Healthcare.gov and plotted maximum out of pocket and deductible cost sharing for each plan for 2020.

There is tremendous variation. I want to pull out two cases that illustrate some extremes of the potential for screening and selection (Chenyoun Liu has a great paper on this topic).

The red arrow points to a $0 deductible, $8,150 maximum out of pocket plan. Most of the cost sharing is going to be very large co-pays for inpatient hospitalizations and big co-insurance. These plans are attractive to people who think that they are unlikely to be in the hospital but could see themselves at the urgent care or PCP a few times.

The green arrow points to a single silver plan sold in South Dakota where the deductible and the maximum out of pocket is $4,200. All of the cost sharing is in the deductible. This plan’s cost sharing design is attractive to someone who knows that they have a massive set of claims coming as their total exposure is far less than it could be for other ~70% actuarial value plans.

There is tremendous amount of cost sharing variation within state and even within county for a single metal tier. This makes comparing plans and expected expenditures difficult without expert support. It also makes academic analysis challenging. This is why I’m looking at California as their rule sets waives away most of the variation and allows for far cleaner comparisons even at the cost of potential generalizability.

Buying insurance is tough in the best choice environment. The ACA individual markets are not that even if they are better choice environments than the unregulated insurance market as analyzed by the GAO.

dnfree

This doesn’t have anything to do with the subject of this column, but I have an ongoing discussion with a right-wing relative. This is what he sent me a couple of days ago. I haven’t so far been able to find any articles to explain where this goes wrong (although I’m pretty sure it does). Do you have any suggestions as to where to look? Don’t take too much time away from your day job!

What Imperial College London did was to use a model that overestimated the infection fatality rate by a factor of ten.

We now know, as the IFR rates of various countries falls and falls, that the Imperial College estimated IFR was completely wrong. The UK, for example, has seen 42,000 deaths so far, which is 0.074% of population. The US has seen about 200,000 deaths 0.053%. Sweden, which did not lockdown down, has seen about 6,000 deaths, which is an infection fatality rate of 0.06%. All three countries are opening up and opening up. Whilst the ‘cases’ are rising and rising, the deaths continue to fall. They are, to all intents and purposes, flatlining.

In Iceland it is around 0.16% and falling. In other words…

Stop panicking – it’s over

Whilst everyone is panicking about the ever-increasing number of cases, we should be celebrating them. They are demonstrating, very clearly, that COVID is far, far, less deadly then was feared. The Infection Fatality Rate is most likely going to end up around 0.1%, not 1%. https://drmalcolmkendrick.org/2020/09/04/covid-why-terminology-really-matters/

Robert Sneddon

@dnfree: I know you’re not really wanting facts and reality in a reply to your “I’m just asking questions” screed but…

The UK has had about 60,000 excess deaths over the past nine months, compared to the average for the same period over the past five years when COVID-19 was not present, so it’s practical to assign all those excess deaths to COVID-19 and its effects. The UK has had about 378,000 confirmed cases of COVID-19 with maybe another 400,000 asymptomatic cases that didn’t get confirmed. Call it a million cases total against 60,000 deaths, that a case fatality rate of 6%. That’s terrifying in its own way.

Basically the waste of text you posted is an example of how to lie with statistics — you take the entire population of a country where the disease, thanks to unparalleled efforts in suppression has only infected a few percent and use that to calculate a total fatality rate. Riiiight.

If nothing else the infection and the dying is continuing, in America and elsewhere around the world and it will continue all the way through this year and the next regardless of any vaccines that are mass-produced. The numbers you quoted in your duplicitous drive-by are only a snapshot of the early days of an ongoing disaster.

Sab

@Robert Sneddon: Also, even if you don’t actually die, you may well have very long term, very serious chronic health issues. Heart damage. Neurologocal problems. Lung damage.

dnfree

@Robert Sneddon: I think you have misinterpreted my “screed” as being from me rather than from a relative. Yes, I am looking for facts, as is my usual habit.

Edited to add that this relative has latched on to all of the recent claims that Covid is less severe, including the one from the “witch doctor” woman and the one that the CDC says only 6% of Covid deaths are actually from Covid, based on death certificates, which I went around and around with him about how death certificates work. So if there’s an article or other reference that explains what you said, it would be helpful. And I agree about the long-term damage, Sab. I tried looking up this Malcolm Kendrick but couldn’t find much.

Brad F

David

How do the premiums vary for those two plans? As first reactions and choice architecture always in play, is their a dominated choice if one looks ONLY at what the monthly premium charges would be on the initial search page? Hypothetical–as I am assuming those two plans are from different states.

Brad

David Anderson

@Brad F: Premiums come into play, and you’re right the $0 deductible huge MOOP plans are from several different states and even more insurers.

I think the broader point is that it is hard to say that there are many if any clearly dominated baseline plans as there is too much overlap in cost sharing designs.

Brad F

@David Anderson:

MOOP?

How does Medicare play into above.

You were referring only to ACA exchanges, yes?

Sab

@dnfree: I understood that your comment was from a relative and not from you. I think it’s good for us to know that stuff is out there, because I personally cannot bring myself to my relatives like that anymore.

David Anderson

@Brad F: Maximum out of pocket — and yes, these are only ACA plans.

ProfDamatu

Insert here my usual comment that even that “low” MOOP of $4200 isn’t terribly feasible for a large chunk of the non-CSR people buying on the exchange. :-/