Last night, the Center for Medicare and Medicaid Services came out with their annual pre-Open Enrollment ACA data packet. One of their big brag points is a legitimate increase in competition back on the ACA exchanges:

Table 1 shows PY17–PY21 QHP issuer participation and plan availability. In PY21 there are 181 QHP issuers participating in HealthCare.gov state Exchanges, an increase of 6 issuers from PY20 and an increase of 22 issuers when considering only states using HealthCare.gov in both PY20 and PY21. On average, PY21 enrollees have access to between 4 and 5 QHP issuers, which is greater than in PY17–PY20, and over 60 QHPs, which is greater than all previous years. Additionally, 4% of PY21 enrollees have only one available QHP issuer, which is the lowest percentage since PY16.

This makes sense. The ACA marketplaces are notably profitable with insurers consistently making well over the cost of capital in profits over the past few years. The ACA marketplaces are policy stable. The ACA marketplaces are politically stable (assuming the Supreme Court does not go YOLO on them). Profitable markets that are fairly predictable and stable with some states reinsuring against moderately high cost claims and federal catastrophic reinsurance is damn attractive. Insurers should expand. Insurers should enter new markets. This makes sense. This is a good brag point.

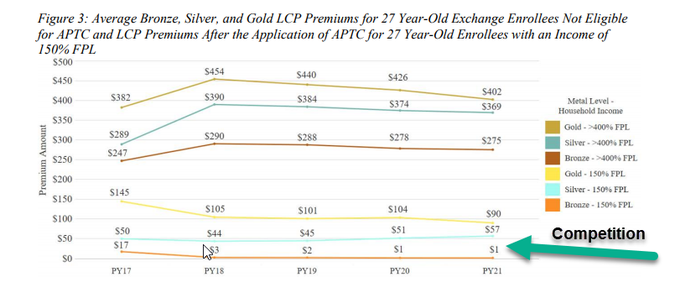

However… the ACA subsidy system does weird things with competitive markets. I want to highlight Figure 2:

The cheapest Silver plans for a subsidized buyer has gotten more expensive even as more competition is in the market.

THIS IS WEIRD!

It is also a direct result of the price linked subsidy system where the subsidy is attached to a dynamically generated value in each county. That value is the price of the second least expensive silver plan. Subsidized buyers are indifferent to price levels. They are very sensitive to price spreads. A monopolistic insurer can elect to create very large benchmark spreads. This is a way to get to accidental and incidental single payer in some states. These are short term price discounts as very profitable monopolistic markets should see new entries sooner rather than later. In competitive counties/regions, insurers will price at least one of their silver plans as close to the bottom of the premium range as possible to increase the probability that they will get a good chunk of the CSR eligible and heavily subsidized population. In both scenarios, the benchmark silver premium is the same, but the cheapest silver plan is way more expensive to subsidized buyers in competitive markets. This is weird set of incentives and market design as competition does not help consumers on premiums; it may help on other attributes (network, plan type, customer service, unobservables etc) but not on price.

So more expensive cheap silver plans are a direct consequence of new entries into the market.

Interestingly, the cheapest gold to cheapest silver gap is shrinking. We saw in California significant shift out of silver and to gold in 2018. Gold’s absolute average cheapest premium is lower in 2021 than it was in 2018-2020 and the spread is lower, so I think we’ll see more movement to gold this year as well.

Another Scott

Thanks for the explainer. :-)

Graphs like Figure 2 drive me nuts. What is the time period of the premium? Monthly? Annual? (I assume monthly.)

Insurance in general seems to hate, hate, hate actually talking about time periods. GEICO and Progressive and Elephant and … all talk about saving on premiums in their ads, but are they talking about over a 6 month policy or over a year??

(sigh)

Thanks.

Cheers,

Scott.

Mudbrush

This sentence made my brain hurt. I’m not smart enough to understand this stuff and that scares me, as I will probably have to go on the exchange in the next year. Thanks for pointing out HealthSherpa, though!

Ken

Do you think this is a problem, and if so what would be a legislative solution? Your answer may assume a functioning legislature.

StringOnAStick

Migrating more people into gold plans at prices close to silver is a good thing, yes it no? It seems like it should be “yes” since people are getting their care with lower copays and less risk of sudden huge medical expenses.