Yesterday, it leaked that the Biden Administration is inclined to re-open Healthcare.gov. In some ways, Healthcare.gov has been partially open since last April with a broad Special Enrollment Period (SEP), but there is a good argument that a full Open Enrollment Period(OEP) which does not require administrative burden to prove worthiness combined with elite messaging and validation as well as significant advertising will insure more people.

However, one of the challenges of an SEP and a partial year OEP is that the value proposition of the insurance gets worse as we get deeper into the year. ACA insurance contracts are designed on a twelve month cycle. The actuarial value of a plan is for the entire year and the entire pool. Shortening the length of the contract means that the actuarial value (the share that the insurer pays out of general premiums) goes down.

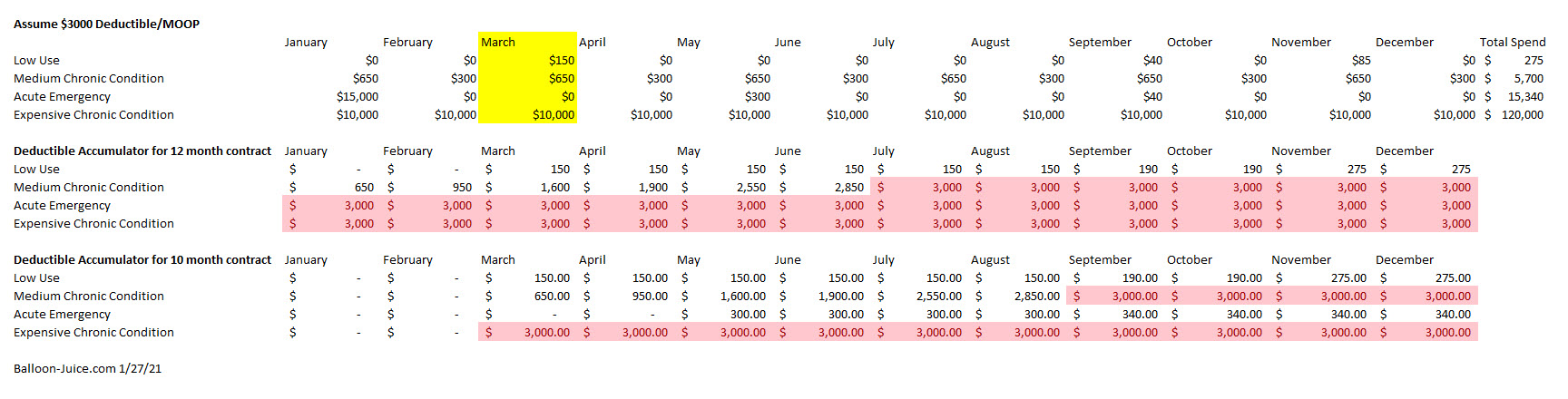

I want to take four utilization patterns and illustrate what is happening when a contract starts in January compared to when it starts in March. For this purpose, I am assuming a single policy with a combined $3000 deductible/Maximum out of Pocket with no other cost-sharing for simplicity sakes.

- Low Use — barely touches the system, a PCP visit, an urgent care visit and a prescription

- Medium Chronic Condition — routine expenses of prescription drugs and specialist visits but no acute emergencies

- Acute Emergency — BABY!!! or APPENDICITIS and otherwise looks a lot like a Low Use individual

- Expensive Chronic Condition — My niece Claire with her leukemia treatment is going to be consistently running up high monthly costs so her family is shopping on the combination of network and out of pocket maximums as they hit the MOOP in the first month no matter what.

The low use individual is indifferent to when their contract starts. They are unlikely to hit MOOP at any point in any scenario. The Medium Chronic Condition person hits their deductible in July under as 12 month contract and in September under a 10 month contract. More importantly, the 12 month contract has the insurer paying for 47% of their claims out of premium revenue while the 10 month contract has the insurer paying only 31% of their annual claims from premium revenue. The effective AV dropped significantly. The individual with an acute emergency with a 12 month contract hits their deductible in the first month of a 12 month contract but never hits it under a 10 month contract. The person with the expensive chronic condition hits the deductible as soon as the policy goes live in either scenario.

These are stylized examples (for example, an acute emergency that happens in July would be fully MOOP-ed in either scenario).

However, the intuition that for a given benefit configuration (deductible, co-insurance, co-pay, maximum out of pocket), the shorter the contract length, the lower the effective actuarial value being offered stands. As plans start later in the year, the effective actuarial value goes down. A Gold plan transitions into a Silver plan in the middle of the year, and then a nominal Gold plan becomes, in reality, Bronze as hot chocolate weather arrives. Bronze becomes Tin and Copper as well. The speed of metal decay will vary depending on cost sharing designs (deductible heavy designs decay faster than co-pay heavy designs) but it is a simple unidirectional reality.

This matters. The monthly premium for an ACA plan is the same if the plan starts in January or if it starts in March or if it starts in November. The value proposition for an ACA plan gets worse as the start month gets deeper into the year. The actuarial value declines while the monthly premium stays constant. This is a problem for future nerds to figure out a solution and then advocates to get that solution implemented via either legislation or regulation, but this is something that we need to be aware of as a limitation on the size of impact an unexpected mid-year OEP could do.

Ken

Is there some reason that ACA contracts run on a calendar year basis? Why can’t someone buy insurance in April that runs to next April, with deductibles, max payments, etc. resetting in April instead of January?

I assume some software would have to change, but I don’t think of that as a good reason.

wvng

Speaking of Claire, how is she doing?

Chris T.

@Ken: The goal is to prevent someone from not buying insurance until the day after they discover they have cancer (or whatever). The method—limiting “open enrollment” to N weeks per year and adding the “significant family status change” (moving, new kid, whatever)—of achieving this goal is … well, I’ll just call it “suspect”. But that’s the “why”.

Ken

@Chris T.: OK, that makes sense, though I think we have similar reservations about the motivation. But I still don’t see why, if a person “legitimately” buys ACA insurance in April because they lost their job, it can’t run until next April.

Brad F

David

The value proposition and AV for payers may work against them if elective cases at the margins (screenings, knees, hips, spines, insulins) that might never have been done get booked with a rejiggered OEP. That is not a minor variable to overlook and even in a stylized world, requires notice. Correct?

Brad

David Anderson

@wvng: so far so good on Round 5 — her numbers look good and she is tolerating the current treatment round.

I will have an update and a call for more blood donations at the end of the week.

Kelly

I’ll be transitioning to Medicare this summer so actuarial value decay will hit me twice. Hopefully I’ll remain a low use guy and it won’t really matter. I’m usually a low use guy. The one time I spent enough that I should have hit my deductible/out of pocket limits the illness bridged December and January spreading the cost over two benefit years, below the limits for each year.