Senator Warner (D-VA) released, at the end of January, the Health Care Improvement Act of 2021. HCIA-21 has several moving parts that seem to mostly conform to median Democratic positions and policy preferences. One of the big ones is removing the income cap for subsidy eligibility and also enriching the premium tax credits.

Capping health care costs on the ACA exchanges: The Health Care Improvement Act of 2021 will ensure no individual or family pays more than 8.5 percent of their total household income for their health insurance. Currently, no family making more than 400 percent of the federal poverty line ($51,040 for an individual in 2020) is eligible for premium assistance on the ACA exchanges. This provision – which is supported in President Biden’s American Rescue Plan – expands premium assistance to individuals making more than 400 percent of the federal poverty line and places a cap on insurance costs for all individuals and families on the ACA exchanges.

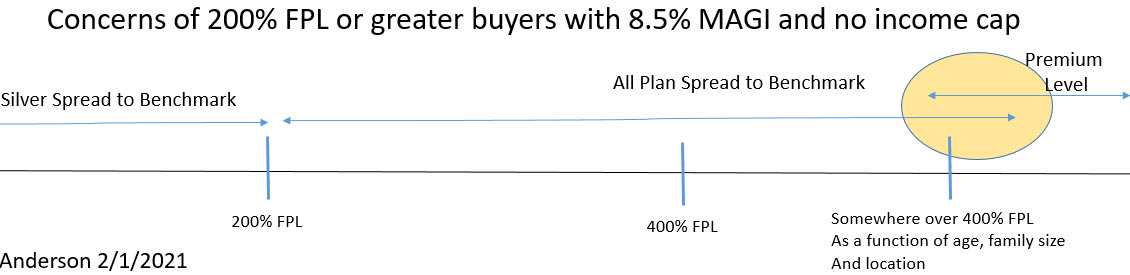

So what does this mean? I’m going to look at this from the LEVEL & SPREAD perspective I outlined earlier this week.

Right now under current law, households that earn over 400% FPL (~$51,000+ for a single individual) can not receive Premium Tax Credits (PTC). This makes the 400%+ FPL cohort premium level sensitive. They care very much about actual, gross premium as that is also their net premium. There are also some folks who earn under 400% FPL who are also level sensitive as the benchmark is so low that they are paying full premium, but this is a small cohort. Policies that reduce the gross premium level such as state Section 1332 reinsurance waivers, wrap-around subsidies with state funds, Farm Bureau “don’t call it insurance” plans, underwritten short-term limited duration plans and most of the public option variants are attractive to this group because it directly lowers what they pay every month.

Changing the applicable percentage of income to 8.5% instead of ~9.86% means that the few people who are currently subsidized but live in areas where the benchmark is too low to matter are far more likely to become spread sensitive. This is a small increase in their personal welfare and it is small population.

The big change is that a big chunk of the people who earn over 400% FPL become spread sensitive instead of level sensitive.

Most of the universe of households who currently earn over 400% FPL will become spread sensitive buyers. Households that earn mid to high six figures will still be level sensitive in this universe as 8.5% of 500K is $44,000 in premiums for the benchmark silver plan. That is plausible for a household of a pair of 64 year olds with three 17 year olds on their plan in the most expensive regions in the country but it is rare. Some people will always be level sensitive but expanding the income cap by either a discrete amount (say to 600% FPL) or eliminating it entirely dramatically reduces the size of this population.

Previous efforts to alleviate the economic pain of price level sensitive populations becomes an even greater give-away to the top 3% to 5% of the income distribution. Reinsurance waivers effectively move some subsidy revenue out of the current 100-400% population and distributes a mixture of federal subsidies and state funds to people earning over 400% FPL would, without any changes to state policies, merely be a transfer back to the federal treasury. States that want to think about enhanced affordability and have current reinsurance waivers would need to significantly rethink their current policy portfolios as reinsurance would not contribute to affordability for the population that currently benefits from reinsurance waivers.

Price linked subsidies do weird things. The biggest weird thing they do is make most people indifferent to price levels but sensitive to price spreads. That can be okay. But it is a deliberate trade-off that shapes all policy intentions and policy outcomes for as long as we keep the fundamental structure in place.

Matt

It will never cease to amaze me that the folks who defend our for-profit healthcare system insist on describing it as “a free market”. It’s like old-style Soviet central planning but with an extra layer of vampiric middlemen skimming 20% off the top of everything and lying to customers.

JKC

Dave, as someone who’s been a practicing clinician for 22 years, I appreciate your posts. It’s interesting to see how the sausage is made.

They are also proof that you couldn’t come up with a more dysfunctional payment system than we’ve cobbed up in the US if you tried.

David Anderson

@JKC: Bullshit, I can come up with an even dumber and more expensive system with only half a dozen beers and a pound of coffee.

TomatoQueen

@David Anderson: You scary, mon.

JKC

@JKC:

@David Anderson: I would have thought you’d at least have held out for a hooker and some blow… ; )

Brad F

David

Can you explain further on following:

without any changes to state policies, merely be a transfer back to the federal treasury.

Brad

David Anderson

@Brad F: Good question.

Right now, a 1332 reinsurance waiver injects some state funds into the claims payment pool so that 100% of claims don’t have to be paid for by only premiums. Adding state funds lowers the amount of premiums that needed. Lower premiums do two things; first it lowers premiums for people who are LEVEL sensitive (>400% FPL) and secondly it decreases the amount of federal subsidies.

If everyone is SPREAD sensitive, lower premiums don’t help them. IT only reduces the amount of federal subsidies. And from a state budget POV who cares…..

laura

Our monthly healthcare premium is several hundred dollars more than our mortgage. We have not qualified for subsidies. We’re grateful that the ACA still exists – Thanks Obama or retirement would not have been an option, but I’m hoping that a lowering of Medicare age may happen. It would automatically reduce our costs by around 40% – a Big Biden Deal.

David Anderson

@laura: I think taking away the subsidy cap at 400% FPL is more likely than a Medicare age drop… either would be helpful I think

Brad F

@David Anderson:

Could you envision a regime whereby reinsurance dollars are selectively cleaved (65/35): premium reducing for plans outside of exchange (>6xFPL) and a “happy” offset for those inside of exchange? Regulatory or statutory jujutsu–but can find the middle ground.

David Anderson

@Brad F: Give me a 12 pack— yeah — but why?

Brad F

@David Anderson: Pareto efficiency? A plan benefiting subsidized vs. non-subsidized only not optimal. Im suggesting a path to make both sides better off

Ronno2018

My strategy for retirement at age 60 will be to manage my income from retirement investments to be below the ACA subsidy limits. I hope it works!

David Anderson

@Ronno2018: Given reconciliation is moving forward and there is broad agreement in the Democratic Party on removing the income cap for subsidy eligibility, this is a very plausible pathway forward.