This week, Oscar Health is going to IPO. It will attempt to raise about a billion dollars from the public markets after raising over $1.5 billion from non-public sources.

This is a big bet. I don’t get what Oscar is doing. That is not a new sentiment (July 2019, March 2017, June 2016 among other comments).

Oscar has had massive losses (from their S-1 p.23)

We have not been profitable since our inception in 2012 and had an accumulated deficit of $1,012.9 million and $1,427.1 million as of December 31, 2019 and 2020, respectively. We incurred net losses of $261.2 million and $406.8 million in the years ended December 31, 2019 and 2020, respectively. We expect to make significant investments to further market, develop, and expand our business, including by continuing to develop our full stack technology platform and member engagement engine, acquiring more members, maintaining existing members and investing in partnerships, collaborations and acquisitions. In addition, we expect to continue to increase our headcount in the coming years. As a public company, we will also incur significant legal, accounting, compliance, and other expenses that we did not incur as a private company. The commissions we offer to brokers could also increase significantly as we compete to attract new members. We will continue to make such investments to grow our business. Despite these investments, we may not succeed in increasing our revenue on the timeline that we expect or in an amount sufficient to lower our net loss and ultimately become profitable. Moreover, if our revenue declines, we may not be able to reduce costs in a timely manner because many of our costs are fixed, at least in the short-term. If we are unable to manage our costs effectively, this may limit our ability to optimize our business model, acquire new members, and grow our revenues. Accordingly, despite our best efforts to do so, we may not achieve or maintain profitability, and we may continue to incur significant losses in the future.

I will try to give Oscar’s argument about why they are a multi-billion dollar company and then I want to work through what I see as my sources of doubt.

Oscar has identified a real problem: Health insurance is not a consumer friendly business.

Oscar’s solution is to throw a ton of technology and front-end user interface development at consumer facing applications to make the consumer experience way nicer and smoother. Oscar then thinks that it can apply machine learning to its ever growing stack of data consisting of both claims data and user reported data to more effectively direct their covered lives to highly effective providers or to direct earlier upstream interventions to save long term money.

The back-end secret sauce relies on a high level of engagement (p.118 of the S-1 ~44% of members are “engaged” monthly.) Over time, the data gets better and the recommendations improve as members are engaged and active and they stick to OSCAR longer which allows for capture of the downstream gains from the back-end secret sauce even as the consumer experience is pleasant and not-painful which is a second source of value.

They are overwhelmingly doing this on the ACA individual health insurance markets.

I think this is a fair description of their pitch.

I have significant doubts about the probability that OSCAR can be a good enough insurance company as it is currently configured to make long term sustained profits. I have several concerns:

- ACA Individual Market is a tough market for the back-end value proposition

- Increased competition

- Ability to execute in 2 parts

- Policy, price shocks and attention

TLDR: OSCAR is making a lot of big bets that highly engaged membership because of an easy to use and user friendly experience can lead to better data that leads to better interventions and a source of private and social value over time. They have spent at least $1.5 billion dollars to learn how to be an insurance company and buying membership. They want to spend a lot more to keep on buying membership and building out their back-end. I have a hard time seeing how this strategy works well on highly competitive ACA individual marketplaces where the marginal buyer is buying almost entirely on cost. If they succeed, that is great, but I still don’t understand what their operations looks like when they are profitable.

More below the fold.

1 — ACA Individual Market is a tough market for the back-end value proposition

The ACA individual market from 2014-2021 is a bifurcated market. Individuals who earn between 100 to 400% Federal Poverty Level receive price linked subsidies that fill the gap between a household’s expected contribution and the local benchmark plan’s gross premium. Many insured individuals will over the course of their contracts never have a claim. Most costs are at the extreme end of the distribution. The marginal new buyer in the market is extremely price sensitive. Many buyers are on the market for a year or two at the most. Some buyers are long term individual market buyers, but the market as a whole is a churning maelstrom of price chasers.

From this perspective, membership chases premium more than it chases other features. Vastly superior networks are not highly valued (~$25 per month willingess to pay) and adversely selected. Customer experience is likely a positively valued attribute but given that most people are barely touching the medical system over the course of the year, it is not going to make up a large pricing gap. Most of the value proposition from the buyer’s point of view is pricing, and more specifically whether or not the plan is either the cheapest silver plan if the buyer earns under 200% FPL or the cheapest plan in each metal tier for everyone else.

OSCAR’s pricing is widely variant. In 2021, they are selling in 128 counties served by Healthcare.gov. In 24 counties they offer the least expensive Silver plan. In another 10 counties, they offer the benchmark silver plan. Slightly less than 20% of their potential market by population on Healthcare.gov will a consumer who is subsidy eligible see OSCAR as either the best or 2nd best option for the most commonly bought plan type (silver). Assuming the House reconciliation bill passes, this will be even more important as both the least expensive and the benchmark silver plans will be effectively zero premium plans. Looking at Bronze plans (the lowest premium, highest cost-sharing plans) OSCAR only has the least expensive plan offering in 16 counties. They have low risk membership attractive pricing in Arizona including Maricopa County and then bits and pieces here and there. In Texas, they are operating at a significant pricing disadvantage to Medicaid managed care like entities such as Molina and Centene.

2 — Increased competition

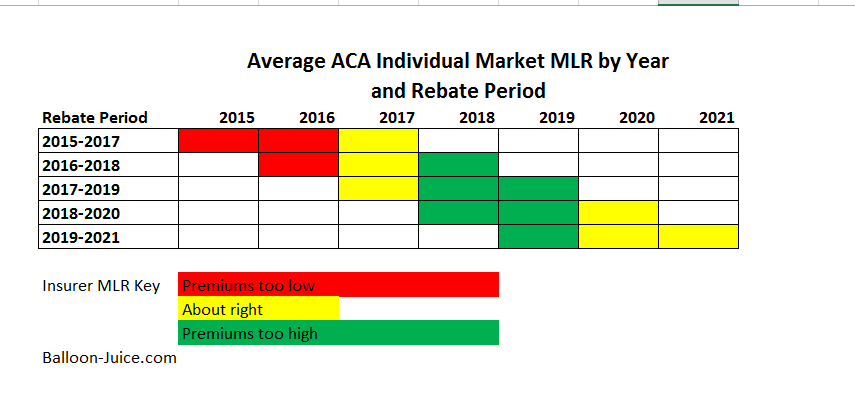

From 2018 to 2020, the structural conditions of the ACA market were set up to allow insurers to make a whole lot of money. Policy and political uncertainty in 2017 created a massive number of monopolies in 2018. Silverloading led to premiums to be massively overpriced in 2018 and overpriced in 2019. Industry wide Medical Loss Ratios (MLR) were really low. By 2020, Silverloading probably had mostly worked its way through the system after two years of nearly flat industry wide premiums. And then COVID hit which meant a massive decrease in claims. These years are structurally set up for insurers in the ACA individual market to be making serious money through low MLR. OSCAR did not do this. They got their 2020 MLR down to 84.7% from their 2019 MLR of 87.6%. Their MLR is well above industry leaders.

From 2018 to 2020, the structural conditions of the ACA market were set up to allow insurers to make a whole lot of money. Policy and political uncertainty in 2017 created a massive number of monopolies in 2018. Silverloading led to premiums to be massively overpriced in 2018 and overpriced in 2019. Industry wide Medical Loss Ratios (MLR) were really low. By 2020, Silverloading probably had mostly worked its way through the system after two years of nearly flat industry wide premiums. And then COVID hit which meant a massive decrease in claims. These years are structurally set up for insurers in the ACA individual market to be making serious money through low MLR. OSCAR did not do this. They got their 2020 MLR down to 84.7% from their 2019 MLR of 87.6%. Their MLR is well above industry leaders.

There are two ways to get MLR down; increase premiums or lower claims costs.

And the possibility that they can increase premiums quickly without losing a lot of membership will be constrained by increased competition. Insurers, by 2021, had mostly returned to the marketplaces after running like hell in 2018. More insurers are projected to come back in 2022. Holding premiums constant (average $505 PMPM) and bringing MLR down to 80% only reduces the $1000 Per Member Per Year loss by about $300 PMPY. OSCAR needs to at least increase premium while still compressing claims and then get a handle on their admin costs. Given new entrants to the marketplace, the premium portion is going to be a significant challenge. And this challenge of increasing competition, assuming the Supreme Court does not remove more than 1 or 2 pages of the law in Texas v California, will be persistent.

OSCAR’s pricing is not amazing in most regions to compete solely on price. And these are prices that are generating significant operational losses, so OSCAR is trying to buy membership and scale right now so that they have more leverage against hospitals to get lower per unit costs (some areas they get good for commercial plan pricing, and other areas, they are paying for the privilege of having almost no utilizing membership in a region where the local hospitals can laugh at the concept of pricing concessions). If OSCAR has to price at a level where they break even, they have an even harder time getting to scale.

3 — Ability to execute in 2 parts

Strategy and Covered Population

I have repeatedly said that I have a hard time seeing what OSCAR does besides get good press, deploy a nice app and lose a lot of money that my former co-workers do not do. This specifically applies to their ability to run the basics of pricing risk and running the back-end of an insurance company in a regulated market.

OSCAR currently insures a population that on net is much healthier than the general ACA individual market. OSCAR is currently insuring a population is coded to be very healthy relative to the rest of the ACA universe. We know this because OSCAR is a significant net payer into risk adjustment. In 2020, each member, on average had about a $1700 transfer into risk adjustment (some markets OSCAR was a risk adjustment receiver) which is notably larger than the 2019 net outflow of just under $1,200 per member per year. About a quarter of premium goes out the door for risk adjustment.

THERE IS NOTHING WRONG WITH A STRATEGY THAT INVOLVES PAYING INTO RISK ADJUSTMENT!

Centene and other Medicaid-esque insurers routinely pay a significant portion of premium in net risk adjustment payables. Other insurers are profitable with significant risk adjustment receivables. Both of those courses are fine as long as pricing and strategy are aligned with the population being insured.

I don’t think there is alignment.

OSCAR’S membership is currently heavy on 18 to 34 year olds and light on 55 to 64 year olds (P. 117). Premiums are heavily concentrated in 55-64 year olds.

Profitable insurers with large risk adjustment payables are mainly competing on price because their membership is barely using services.

More importantly, OSCAR’S adjustment profile is saying that their covered population should be healthy and use few services but their MLR is telling me that they either have horrendous per unit costs or a lot of utilization. I am curious if their highly engaged members and OSCAR’s no cost-sharing virtual platforms generate a lot of low dollar, low acuity claims that are not generating risk-adjustable diagnoses for things that if there was either cost sharing or an expectation of in-person visits with the corresponding transaction and hassle costs would never have generated a visit. I know that if my son is feeling mostly fine but a little warm and had green boogers coming out of his nose and he wants to go to bed by 7:00, the diagnosis is likely a viral infection with a treatment course of sleep, hydration and a day of cartoons. If there are either cash or transaction costs to go to a doctor, we’re not going to the doctor unless it does not clear up in a week. If there is a no cost to the visit and we can do it in between conference calls, sure, I’ll get him checked out.

OSCAR has demonstrated that they can sell an experience at a loss. The population that is mostly buying this experience is young and comparatively healthy. They have not demonstrated that they can price their products competitively at a break-even point. There is little space left at current pricing to drive down MLR. Their 2020 membership gains were from a population that was even healthier relative to the rest of the market than their 2019 population which was still an extremely healthy population relative to the rest of the market.

OSCAR contends that its analytical engine’s special sauce driven by integrating both claims (which every insurer can do, and many can do so from far deeper and broader data sets) and member reported data which is somewhat unique to OSCAR will lead to better choices for lower cost bundles of care and better health. This sounds plausible if there are large populations with robust medical needs that may be amenable to management and intervention. But given OSCAR is insuring a population that is heavy on young people and light on old people and has a risk score that is well below market averages, where is the squeeze? OSCAR’s special sauce to better manage diabetes could be fantastic but OSCAR is unlikely to be covering a lot of people with Type 2 diabetes. Where is the squeeze with the current covered population?

Scale

OSCAR is bragging that they are rapidly growing. They are buying membership with large losses. Some of their markets have decent scale within the context of the ACA (California, Texas, Florida). Some of their markets are tiny with fewer covered lives than my high school had students. They have half a million total covered lives in 18 states. Their ability to leverage their membership to get good pricing locally is limited. Their administrative costs have been high and are not shrinking on either an absolute or percentage of premium basis. When I worked at UPMC Health Plan, the Medicaid line of business for a single state (Pennsylvania) had 400,000 covered lives and was profitable. We had scale in parts of the state and were an after-thought in other portions of the state. We had scale challenges in a single state with the same ballpark of covered lives as OSCAR has in a good chunk of the national footprint.

4 — POLICY

As I mentioned earlier, OSCAR has been operating in an environment from 2018-2020 that is conducive to pricing high and low MLRs. That is changing.

More importantly, operating with the assumption that the Biden Administration is able to pass the COVID-related American Rescue Plan with significantly enhanced subsidies for more people, large chunks of the current covered population will be receiving significant positive price shocks. Inertia has been the friend of any insurer that can gain membership by pricing low in their first year and then raise premiums modestly over time. Price shocks, even positive price shocks, will make people who are currently not paying attention and automatically renewing their policies in plans that are no longer the best priced options, pay attention. OSCAR’s pricing in 2021 for Healthcare.gov is the best for the under 150% FPL group that will see $0 premium Silver CSR plans. This will be helpful to OSCAR in 2022. However, its pricing in other markets will not be as good as other on-exchange carriers which people will pay attention to and plausibly switch to in 2022.

Cheryl Rofer

Sounds like the Silicon Valley startup approach: Lose lots of money, but make up for it on volume.

Ken

@Cheryl Rofer: Plus, they’re applying machine learning to enhance the user experience and carve out market share. Very SV, in case “We’ve lost 1.5 billion dollars, but with another billion we can do so much more” wasn’t enough of a clue.

taumaturgo

In simple words. Is a scam. Is monetizing pain and suffering for profits. Like their counterparts, the only service they wish to provide is to themselves by spending heavily on midnight TV ads and glossy mailers.

Edmund Dantes

Under section 1.

this sentence just ends in the middle.

“ Most of the value proposition from the buyer’s point of view is pricing, and more specifically whether or not the plan”

really interesting read.

Frank Wilhoit

Oscar’s strategy (as distinct from their tactics, which, as you point out, sucketh wind) can only be to become large or influential enough to lead the entire industry to put irresistible pressure on legislators and regulators to simplify the individual market beyond recognition. As long as they are trying to paper over the existing landscape with “friendly” UX, they are going to burn cash with nothing to show for it (except, possibly, some evocative gestures in the direction of a possible future “friendly” UX). If they actually managed to get the landscape simplified, then their play would be to license their UX IP to their competitors, who at that point would be playing catch-up.

That strategy is not going to work, for several reasons. Too much money is being made off the complexity and opacity of the landscape as found — maybe more by skimmers than by principals, but not enough to make the principals want to blow it all up. And the only really effective way to simplify the consumer experience would be to go to single-payer.

David Fud

Sounds like a good short sale opportunity for the investors among us.

SiubhanDuinne

Kushner taint.

Another Scott

@Frank Wilhoit: I end up at the same conclusion, but I would phrase it differently. They say:

Emphasis added.

They want to buy themselves into being a big enough player to collect monopoly rents. They know that the post-Reagan business path to giant profits is to become a monopoly. They know that people/companies don’t want to deal with more than one insurance company. So, their goal is go get huge. If they can’t get big enough to win, they hope to become big enough – with enough subscribers – to be bought out with golden parachutes for management and investors.

Having a flashy website and staying in the news helps keep them front-of-mind for people who make decisions without really understanding what’s going on.

I think they’re right that there will be fewer insurance company players in the future, especially as we move toward single-payer. Private companies probably aren’t going to go away. Those that remain will be sitting pretty is their hope.

tl;dr – Follow the money, and remember that the people at the bottom aren’t the real product.

My $0.02.

Cheers,

Scott.

Barbara

It’s a real conundrum, if your value proposition is a kind of artificial intelligence that can make care for sick people more efficient when your pricing methodology and general marketing appeal attracts mostly young, healthy people, which more or less makes it very hard to accumulate data for your AI. Other companies have missed the mark with their exchange business, but few have stuck it out like Oscar. Its model might actually be more strategic for a Medicare population, which prioritizes service and network experience and uses a lot of care.

Lobo

My .02 cents.

Here is why I see trouble:

I see this everyday. Build technology and it will solve. In this approach, I always ask what problem are you trying to solve? What is the current solution? How is yours better? Usually, it is a solution in search of a problem. If technology was the answer Haven would have worked. But it didn’t.

2. OSCAR is making a lot of big bets that highly engaged membership

People do not want to be highly engaged in insurance. They have better things to do. Sure there is a small cohort that is thrilled monkeying around with it. But most want to forget about and do better things with their lives. It is not that people want a nicer experience per se, but that want an experience as seamless and hidden as possible. Having to interact with another portal is a burden.

3. But given OSCAR is insuring a population that is heavy on young people and light on old people and has a risk score that is well below market averages, where is the squeeze?

This dataset might not be robust to accomplish anything. In addition, I bet it skews heavily white causing a huge bias in the data.

My quick thoughts.

Frank Wilhoit

@Another Scott: I think perhaps you meant to say that the people at the bottom are not the real customers.

cain

My dad had come up with a concept that uses AI to come up with an app that would figure out the correct dosage of a medication based on the data of tens or even 100s of thousands of people who might be using the medication. I’m not sure how that would play out but I thought it was kind of interesting, but he couldn’t find anyone who would be willing to chase it down.

Another Scott

@Frank Wilhoit: Yes. It’s the old internet mantra – “If you’re not paying, you’re the product.” If OSCAR can’t make money from their overt business plan, then their overt business plan isn’t their real plan.

OSCAR’s sources of money going forward are likely (eventually) other players in the industry – either by eating their subscribers and charging more, or by being bought out. They seem too small to be much of a threat to the giant established players at the moment. But if they can hold on long enough, and get enough buzz, then they can hope to become the next

Pets.comTesla and have the magic of the stock market allow them to punch above their weight. Will it work? No idea.Cheers,

Scott.

laura

OSCAR makes me grouchy.

I hate internet-cute names with the heat of 10 thousand white hot suns. I distrust the black box solutions model that depends on capturing market share to survive. Extreme youthful caucasity. I expect this is a make money scheme posing as a health insurer. Kushner – do not trust.

PJ

@Barbara: But Oscar doesn’t prioritize service or their network. When they were my insurer, they routinely denied claims even though they were clearly covered by my policy; only when I appealed them to the state board did they finally pay up. In one instance, I checked to see if a specialist was in-network by going to their website, which showed her listed as in-network, and I called Oscar to confirm that the referral from my PCP to her was OK, and they gave me the green light. They then denied the claim stating that the specialist was out-of-network. When I pointed out that she was listed on their own website, they claimed that this had just been a “prospective” listing as in-network, and that at the time of my visit, she was out-of-network. Their business model is predicated on insureds just giving up at all the red tape they throw in front of you.

SiubhanDuinne

@laura:

Heh.

Barbara

@PJ: It’s interesting to see how actual practice deviates from public image. The provider listing was deceptive. It’s probably too late, but I would have complained about that.

Do you mind me asking what line of business it was — exchange, Medicare or commercial?

Capri

Everyone of the problems being pointed out here would be made worse by going public. If your only chance of success is to out-endure your competitors and your rosiest projections are to lose billions more before seeing any money, why change yourself into a company that has to primarily worry about turning a profit in the next quarter? It makes no sense.

PhoenixRising

@Frank Wilhoit: And the only really effective way to simplify the consumer experience would be to go to single-payer.

Yep, and I think their play (to the extent it isn’t ‘we can lose $X per member & make it up on volume’) is to have the back end built for a public option, which is the side door into single payer. The deep pockets on Oscar are connected enough that if we get that public option, they might be able to “help” write the RFP for the UX/backend coding purchase.

As Lily Tomlin said: No matter how cynical I get, I can never keep up.

David Anderson

@PhoenixRising: Their pockets aren’t that deep. If OPTUM (owned by UHC) wanted to squash OSCAR, they could do it with barely a bump on the bottom line.

Frank Wilhoit

@PhoenixRising: I’m way ahead of you. What you say here not only may be true, it might not be a bad thing, as — in the still very unlikely event of things playing out that way — it could lead to a smoother rollout. But Oscar’s parents’ pockets are not deep enough to wait that long — nor would anyone’s be. That is the puzzle.

randy khan

An IPO is not a bet by the company. It’s a bet by all of the new investors. And, often, an IPO is a cash-out event for the early investors, so they can get a return. In this case, the founders look like they’re not selling, but others are, to the tune of about 5% of the total, so call it $50 million.

Mary G

Nobody likes their health insurance – if they’re healthy, they’re pissed that they pay for what they see as nothing, and if they’re sick they’re mad about things they didn’t know weren’t covered, or they have a big copay, etc. etc. Saying they’re going to change that by being BFFs on the internet is like @SiubhanDuinne: says. The Kushner boys are idiots.

Barbara

@randy khan: I don’t know anything about Oscar, but I agree that in the usual case an IPO is an early investor and/or private equity exit strategy.

Another Scott

Motley Fool – Will OSCAR be the next Lemonade?

WTF is Lemonade?

Motley Fool – Is Lemonade really the disruptor investors think it is?:

[ clang, clang ] Danger Will Robinson!! [ /clang, clang ]

Why am I remembering commercials of dancing old mortgage bankers throwing cash around like it’s 2006??

Are there health insurance credit-default swaps yet??

FWIW.

Cheers,

Scott.

Barry

@PJ: “But Oscar doesn’t prioritize service or their network. When they were my insurer, they routinely denied claims even though they were clearly covered by my policy”

This is my opinion about their whole proposal.

The bad ux is deliberate. The whole point of insurance is to not pay. How can the user interface improve that?

Arclite

I work for a healthcare company that dominates its state with around $4B in annual revenue. We’re $160M or so underwater over the past year thanks to COVID. This is a hard time to be in healthcare insurance.

Wayne

“OSCAR contends that its analytical engine’s special sauce driven by integrating both claims (which every insurer can do, and many can do so from far deeper and broader data sets)”

I worked at Oscar in Provider analytics at the beginning and led a team focused on the same for a huge national payer 5 years later. The national payer still hasn’t caught up to Oscar’s data science capabilities in 2014; there’s a strong case to be made they can leverage this in a way others cannot, because they’ve prioritized it since day 1.

David Anderson

@Wayne: Assuming OSCAR’s analytics are superior — I have two comments. First, OSCAR is almost entirely a single line of business with narrow footprints without a ton of longevity in the markets. Other insurers have multiple lines of business (ACA, Small Group, Large Group, Medicaid, Medicare Advantage etc) with decades of data so the odds that any member showing up for the first time in the ACA pool of business is truly new to the data set is high for OSCAR and not as high for large, multi-line carriers. OSCAR might be able to get more out of any given piece of data, but large carriers can throw a lot more data at a problem.

Secondly, where is the squeeze for an exceptional data model on a low acuity population? Oscar’s population is young and coding as healthy. There should not be a lot of predictable, chronic conditions to squeeze costs. Given the risk scores, OSCAR’s expense profile is heavy on incidents that involve the phrase “hold my beer and watch this” and light on insulin compared to other, profitable insurers. “Hold my beer” is actuarially predictable but what is the individual level intervention that reduces “Hold my beer” incidences and costs per incidence?

Wayne

@David Anderson: On item 1, huge national payer employer is unable to connect nearly all current members to past membership. Been working almost 2 years. Additionally, I’ve found tons of money-saving insights about provider behavior but there is no mechanism to act on any of it. Big national payer has no relationship with physicians and they’re often working through health systems and provider groups as an extra layer, each with their own incentives. Oscar purchased large historical claims/care datasets when entering new markets and has built their digital infrastructure and customer experience for this purpose from the very beginning. They’ve also trimmed/selected narrow networks in a lot of places not just for prices but for provider communication/engagement.

On item 2 I agree with you, no good answers here. On the diabetes issue, members have to be coded, with recency/frequency, to get credit for risk-adjustment purposes. Greater use of remote visits relative to competitors probably exacerbates this. My guess is Mario & Josh are working to better align incentives in the background and to ensure proper coding. I haven’t spoken to them in years, but if I had to guess I’d say their long term angle here is to be better than competitors at managing certain conditions –> make more money, allowing them to lower premiums –> attract more members –> repeat. Taking advantage of the vicious cycle that doomed Health Republic in NY.