Now that the Senate has passed the American Rescue Plan, we can be very confident that sometime in the next week or so the ARP will be showing up at the White House’s door step ready to be signed.

One of the big pieces of the ARP is a 2 year update of the ACA subsidy table. There are two major things going on in the update.

- Everyone will now be eligible for subsidies if the benchmark silver plan costs more than 8.5% of their income

- Subsidies for everyone who currently gets a subsidy will increase

Point 1 is mostly aimed at upper middle class families. Senator Cassidy (R-LA) consistently told a story about a Louisiana radio host and his wife who were both in their mid-50s and had 2 kids in their late teens/early twenties including one with a significant pre-exisiting condition. This family earned over the subsidy cap and was paying $40,000+ a year in premiums. This family will see massive relief in April or May once this gets operationalized.

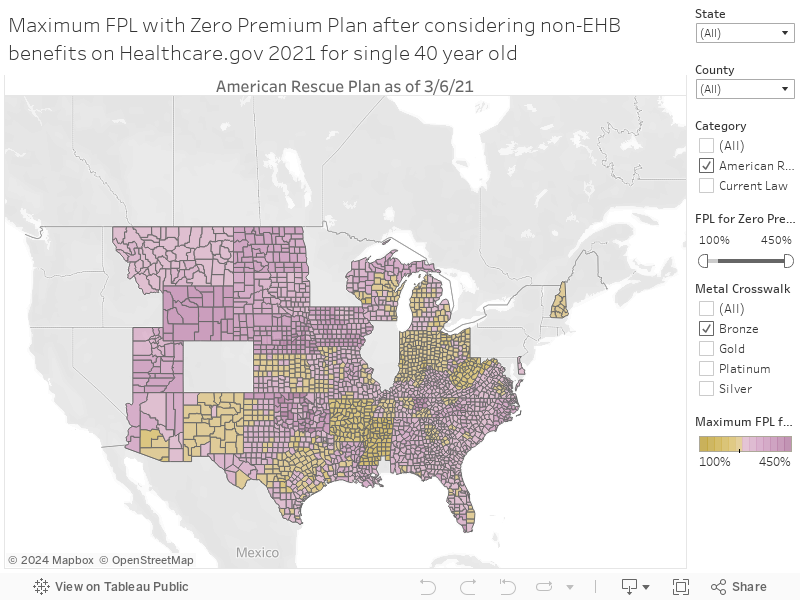

Point 2 is aimed at making the currently subsidized significantly better off. Zero premium plans will be way more common. Everyone earning under 150% FPL will now see two Silver plans with 94% Actuarial Value (low deductible) plans whose core benefits will cost them nothing. Most people earning well over 250% FPL will see at least one Bronze plan with a zero dollar premium plans. Zero dollar Gold plans on Healthcare.gov will be available to single 40 year olds earning over 200% FPL in all of North Dakota, Wyoming and big chunks of the Great Plains and a little bit of North Carolina. At that income level, gold beats silver with CSR on both price and cost-sharing.

There are a lot of other moving parts in the ARP but this is what I’m focused on right now.

Tableau with changes below the fold

wvng

As Joe once said, “this is a big f…ng deal!”

p.a.

Why the blanks? Benchmark silvers already under 8.5% income?

rikyrah

Imagine that

An Administration interested in supporting Obamacare, not tearing it down

David Anderson

@p.a.: Really good question. There are two components of premiums for ACA plans. Essential Health Benefits are required benefits. Non-Essential Health Benefits are “add-ons”. Non-EHBs can not be paid for with federal subsidies. The most common non-EHB is non-Hyde voluntary abortion coverage, but they also include acupuncture, gym memberships etc.

So the blanks are places where the least expensive AND 2nd least expensive Silver plan both have some non-EHB benefits in them.

sab

This is a huge deal. Before I went on Medicare, my monthly premium for a silver plan was as much as the annual premium on Medicare.

@rikyrah: Yes. Ohio’s Rob Portman has been bleating for years that the ACA has problems that made it unaffordable for the middle class, but he couldn’t be bothered to do anything to help fix it.

Xantar

Wait. So is #1 permanent or is it only for 2 years? I’ve seen ambiguous reports.

Spartan green

Do people get to choose a better plan this year?

Hoodie

What do you think this fundamentally changes health insurance for smaller employers? I would think that some smaller business would drop health coverage, especially if they have older employees. We hit a cliff in premiums with a couple of our employees hitting 60.

David Anderson

@Hoodie: look at something called an ICHRA

KatieK

I currently have coverage through the ACA. Will that plan be adjusted accordingly to where I don’t need to reapply for coverage or do I need to “go shopping”?

SamInWa

Some of my friends are in the category of having no income (semi-retired), but not poor enough in assets to qualify for Medicare expansion. (living in Washington State).

Do the changes happening under the ARP impact people in that situation?

Also, will people be able to change from a crappy bronze plan to a silver plan mid-year?

Almost Retired

Marginally on topic, but does anyone have any further information about the Administration’s plans to push for lowering the age for Medicare to 60? I know, one thing at a time, but it was brought up repeatedly during the campaign. Asking for a friend who is 59 and almost retired…..

Mary G

I hope the administration does a better job of getting the word out about this than Obama’s did. Appearances by actual people talking about how this will change their lives would help the voters understand why elections have consequences much faster.

Goku (aka Amerikan Baka)

What about a family that pays $1200-1300/mo for an ACA Bronze plan? Will they be eligible for federal subsidies?

David Anderson

@Goku (aka Amerikan Baka): Yes!

Julie

@SamInWa: I’m pretty sure there is no asset test for Medicaid in WA state. If you go to wahealthplanfinder.org and enter an income level that is below the cutoff for ACA, you will be put on Apple Health (Medicaid).

Freemark

I need to get an ACA plan starting April 1st. Do you think plans will be updated in time for me to do that?

KithKanan

Point 1 will affect far more than just the upper middle class in high cost of living areas like CA. If I weren’t getting employer coverage, I would fall in the group as a single about to turn 40 making just a bit over 400% FPL and still living in a studio apartment.

David Anderson

@Freemark: If it is not updated in time, don’t worry, you’ll get a retroactive payment to make you whole at the new subsidy table. Go get you some…. insurance.

Freemark

@David Anderson: Any chance you know where I can find out what the change in subsidy will be. A change in subsidy may allow me to get a better plan. But I need to know what the difference will be.

Sharon

@Almost Retired: I actually read that they wanted to change it to 55. But you’re right, I’ve heard nothing since the election.

Melissa

@Freemark: enter your info into KFF’s new subsidy calculator, then go on Healthcare.gov to check out your options. By doing some math with your new estimated subsidy, you should be able to ballpark your monthly cost. https://www.kff.org/interactive/subsidy-calculator/