The ACA as experienced by individuals and families is a program that varies tremendously at either the county or zip code line. Pricing is a function of which insurers are in a given region, what their strategy is and how those facets interact with other insurers. And these characteristics and interactions change dramatically over time and space. The lived experience of the ACA is very unstable and mostly unpredictable.

We looked at this in November 2016 with a focus on Tennessee:

More importantly, people in Perry County who are getting subsidized will see the ACA working really well. They have good, cheap health insurance. However their cousins across the state [in Roane County] are getting a raw deal compared to the great deal that they get in Perry County. This is especially true as we move up the income scale which means moving up the likely voter scale and influence scale.

And that was true for 2017. It was true for 2018-2020. It is untrue in 2021. Silver premium spreads between Roane County and Perry County Tennessee have converged as competition returned to the markets and strategies evolved.

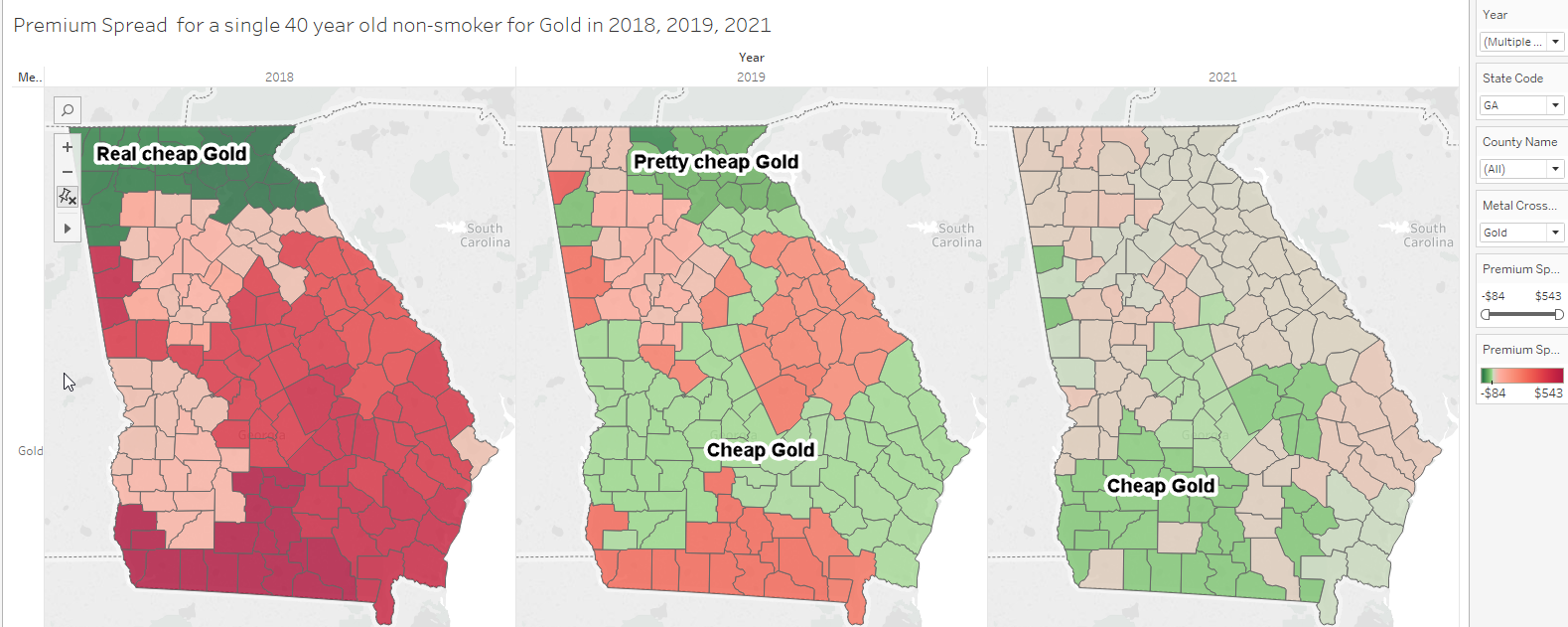

I want to look at Georgia and the experience of Gold spread from the benchmark plan to illustrate this point even more clearly. Georgia’s insurance regulators told their insurers to do whatever they needed to do in 2018 to deal with the non-payment of CSR benefits. Some insurers broad loaded, others silverloaded, and one, silverloaded and took silver-gapping to an extreme degree. This produced amazing variation across space in Georgia. However the below benchmark gold plans (green in the map below) are not consistent over time. Cheap gold was readily available in North Georgia in 2018. It has disappeared in 2021. In south Georgia near the Florida line, gold was achingly expensive (red in the map) in 2018 relative to benchmark while it is below benchmark in 2021.

The lived experience of someone who is actively shopping on Healthcare.gov is wildly variant. It is variant across geography. It is extremely variant across time. The time variation is two fold; one is a unidirectional that if we hold everything else constant, premium spreads should increase for plans priced below benchmark due the age ratchet mechanically increase premiums at a standard percentage each year a person ages. The other variation is everything else. Life changes, insurer strategy changes, insurer competition changes, regulations change. Inattentive buyers will see significant premium swings even as they make no choice.

I am curious as to how people experience and perceive these variations.

dnfree

Is it accurate to say that this shows the effect of states’ rights also? The ACA is dependent on how tightly a state regulates insurance, and whether the regulation process is more favorable for insurance companies or for consumers? Does this ever change over time (a particular state becomes more or less consumer-focused), or is it pretty consistent over time within a state?

Butch

I’m in an area where there is no competition and the experience is miserable. I would go with any alternative in the world to an ACA plan here in the Upper Peninsula of Michigan.

David Anderson

@dnfree: The within state variation is mostly function of insurer level variation (both within and between insurer) as some insurers are strategically nimble and adjust strategies quickly while others have strategy arthritis. There is some in-state policy variation (Kentucky is most notable) with the decisions to expand Medicaid, 1332 reinsurance waiver concept and the decision to go to a state based marketplace or not three of the main easily observed dimensions.

Betsy

I’m having a great time with free insurance as long as I keep my income below ~18,000/ year. I can do this several ways.

• I can live poor as a churchmouae and just live off my 18,000 deliberately limited income. (Fortunately this is not too difficult as I am a Gen X’r and I have had to do this for a lot of my life including some of my prime earning years while I waited for baby boomers to retire out of jobs which they never did because the recession hit and they had to stay working, etc. but anyway I digress)

But I would rather just make more money without falling off the subsidy cliff and having to pay $1100-$1200 a month for decent health insurance

• I can live off some of my savings, which is not a great idea long-term,but I’m hoping by the time I run out of savings, we’ll have Medicare for all, or the age qualification will be lowered to where I will age into it before too many more years.

• I can earn more than18,000, but continue to live really really cheaply and stuff the extra (anything above 18K) into a retirement savings account that doesn’t count against my income for tax and ACA purposes.

Again, not a great option unless you’re pretty close to retirement age and able to make it on 18,000 a year cash net.

But fortunately you can stuff quite a bit away into a retirement account before you hit the limits of that tax exemption … As long as you’re able to live without it for quite a while, like years. Eventually it *will* be yours when you’re really too old to enjoy it anymore, but will need the security

• I can keep driving a 20-year-old car and living cheaply

So bottom line … Policywise this situation just sucks for our economic societal wellbeing.

I know there are a lot of people like me, who are capable of earning quite a bit more than 18,000, but they are deliberately keeping their income low in order not to fall off that subsidy cliff. I know, because there are articles about this written for people in my situation or other situations similar to it. I have bookmarked them and refer to them when I do my annual financial outlook (such as it is)

And I think it’s a really dangerous way to run an economy – in which your middle-aged people, with the most life experience and a lot of earning power, and probably at the peak of their economic years, but as happens at that age, with significant health risks or maybe pre-existing conditions that they simply cannot risk going without gold level insurance, but if they earn what they’re capable of earning then the insurance premium ends up costing them just huge huge amounts of money over $1000 per person per month (in my case it would be over $1100 and I simply don’t have the disposable income to just throw that away like that).

Especially when you’re self-employed and you’re covering so many other costs, and with just one income l you don’t have anyone to back you up and you have to supply your entire existence playing breadwinner and homemaker and provisioner and planner for your entire household. It really is a matter of the old saying “Two can live as cheaply as one.”

Bottom line, what I am saying David, is if we continue to have a subsidy cliff like this, we’re going to run the entrepreneurial economy into the ground. Some of your most productive earners are deliberately keeping their income low and living, like me, without spending anything above the bare minimum in order to be able to do it.

Once again it’s a continual challenge and roadblock in the American economy that individuals are forced to try to do risk management by making tremendous changes in their choices,artificially induced by the systemic arrangements, when the risk management could be much more efficiently done at a societal scale.

As soon as we can just get Medicare for all, goddammit, people like me can start contributing to the economy again by earning money, and spending money, instead of cutting so close to the bone out of fearing for financial disaster based on one untimely hospital stay.

End of rant.