At the Health Affairs Blog, Patrick O’Mahen and I lay out the challenging choice environment for people trying to buy insurance on Healthcare.gov. We know from the Medicare Advantage research space that choice quality crashes when people are faced with more than fifteen choices. The price of bad choice is most heavily borne by individuals with cognitive decline and limited resources. Overly burdensome choice complexity is a regressive tax.

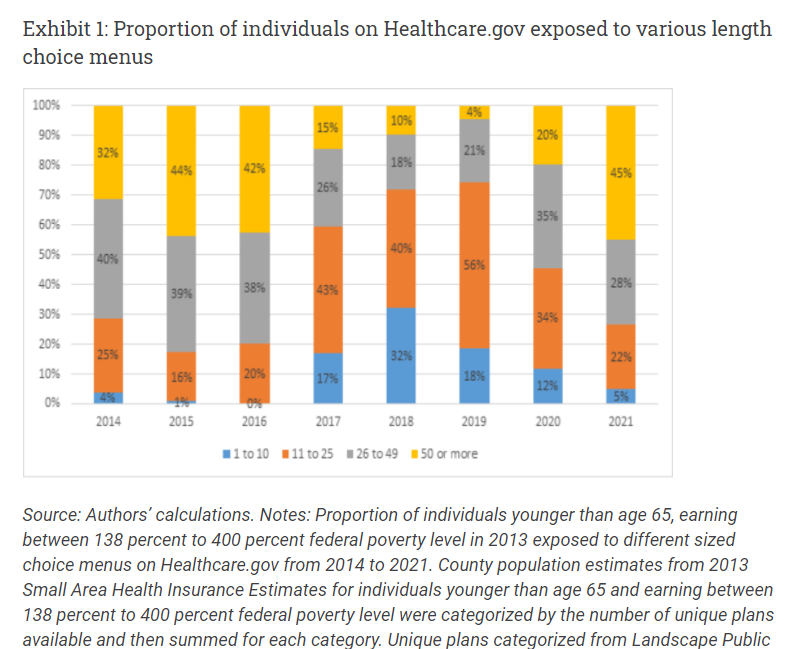

We first looked at the number of unique plans that were subsidy eligible on Healthcare.gov from 2014-2021 on a population weighed basis so that a county with 2,000 residents and 2 plans counts weigh less than a county with a million residents and 65 plans. We sliced the universe into four buckets and considered 50 or more plans to be an OUCH indicator for plan choice. That is a lot of choice. And it is an amount of choice that varies considerably over time. 2021 had 45% of people on Healthcare.gov looking at 50 or more plans. This was similar to 2015 and 2016, but very different from 2018-2020.

We first looked at the number of unique plans that were subsidy eligible on Healthcare.gov from 2014-2021 on a population weighed basis so that a county with 2,000 residents and 2 plans counts weigh less than a county with a million residents and 65 plans. We sliced the universe into four buckets and considered 50 or more plans to be an OUCH indicator for plan choice. That is a lot of choice. And it is an amount of choice that varies considerably over time. 2021 had 45% of people on Healthcare.gov looking at 50 or more plans. This was similar to 2015 and 2016, but very different from 2018-2020.

I think there is a lot of very interesting work that can take this image as a jumping off point, but that is not where I’m going this morning.

Instead, Patrick and I propose that states and exchanges bear the burden of expertise by offering options where the individual puts in some basic criteria such as :

- Maximum premium to pay

- Have to have doctors/hospitals

- Current Drugs

- Measures of liquidity/assets (ability to afford a deductible etc)

And then from these sets of relatively clear preferences, expert decision support systems would be used to pick a pretty good if not perfect plan.

Another option is for states to integrate their exchange functionality with other state based social welfare databases so if other data systems indicate that an individual is eligible for a zero premium plan, the individual is placed into a zero premium plan with the option to opt out.

In both these cases, the entity that is able to handle complexity and expertise bears the cost of complexity instead of the individual. These steps would likely increase enrollment and improve the risk pool as the hassle and attention costs of enrollment can be waived away for individuals who are likely to be relatively low users of healthcare services. I think that expert decision support and the assumption of administrative burden by the state is where most of the action will be over the next couple of years as these frictions dominate modest changes in net premiums that rejiggering subsidy regimes can do. I also think that the choice environment is likely to get more crowded in 2022-2023 and beyond as the large national insurers are re-entering the markets en masse and the current insurers are either holding constant or expanding their service areas.

Sidenote 1: Exhibit 1 in a wide variety of forms has been the image/graphic/exhibit that has been lodged between my eyes the most for the past six months.

Thistle313

When I retired last year, my employer provided access to that kind of system to help me navigate Medicare signup. Put in my meds, my docs, and it showed my best choices for both traditional Medicare and Medicare advantage plans. It was great.

Lobo

One of your key statements here is, “Overly burdensome choice complexity is a regressive tax.” Overly burdensome “administrative friction” could be considered a regressive tax also. You are providing the language to start framing this in a better way. Thanks. I think there is another paper there.

On another note, as Americans we fall into the trap of “the perfect”. A lot of resources are spent on this quest instead of accepting “pretty good”. The problem of integrating this into social services is that their systems are not the most up-to-date and suffer from a lack of technical staffing. So who is the entity that can bear the cost of complexity becomes the question. Interesting analysis.

Just Chuck

@Lobo: When it comes to health insurance, I think most people are looking for “least bad” rather than “perfect”. There’s a built-in assumption that anything that might possibly not be covered will result in being bilked for their life savings over it. Hell, that assumption is often there for things that are covered. The level of distrust people have in both the product and the vendor can’t be overstated.

David Anderson

@Just Chuck: I agree — the choice threshold should, in my opinion, seek to avoid “piss-poor” even at the expense of giving up some probability of selecting “perfect”.

There is a growing body of research (Abaluck et al) that finds quality of insurers matters a lot on mortality/morbidity and people don’t buy on these attributes so that excluding the truly “piss-poor” plans would have a modest effect on choice menu size but significant mortality improvements.

David Anderson

@Lobo: GET BEHIND ME SATAN

No more new paper ideas until after Christmas and the 1st semester of coursework.

With that said, I think you’re right, there is something very interesting to start poking at here. Ben Handel has some good work on this under development (https://static1.squarespace.com/static/5ee3119aa4c9ed2dd490b6ff/t/5ef258c31703e25727e59132/1592940748952/HKMS_draft.pdf) and then there is a whole Public Administration literature that is digging into the incidence and costs of administrative burden on a more granular level.

dnfree

@Lobo: yes, now we’re in systems design territory and finding out what information each system maintains, is it accessible and if so how, is it current and accurate information, how can they be improved if needed, how can they be merged, how can they feed each other. It can take a long time to put this together, and of course there will be a lot of different systems—federal, state, local, of differing quality and accessibility. Toward the end of my long career, it’s amazing how much time went into exactly this kind of problem—getting data coordinated.

Fake Irishman

Great to see this come out. Now there’s at least one scholarly collaboration that arose out of a connection in Balloon Juice. (God help us all)

Fake Irishman

One thing that Dave doesn’t mention here is that target date retirement plans already do a lot of this for retirement investing, which is what inspired this piece: you pick when you intend to retire, and then you pretty much check your balance twice a year. professionals take care of the rest for a very very low fee. So the idea here is: what are some things states can do to recreate that sort of ease?

Quaker in a basement

As a prob/stat student, I have to say this is the best use of a stacked bar chart I’ve ever seen.

Lobo

Everyone: I always love this dialogue.