One of my mentors asked me to see if I could make sense of everything that I have done, am doing and thinking about doing including plausible dissertation ideas.

The objective is to see if I can tell a coherent story of my research interests that is somewhat more sophisticated than but just as true as: “I like my co-authors, I enjoy writing with them and we have cool questions that we run into on a frequent basis.” I think that explanation can hold a lot of water but tying together what the cool questions are in my mind is a good thing. I’m including the version of my story board that only contains publicly available works so that are things which have been published, accepted or there are working papers released. The version that my mentor is getting includes a lot of works in progress, future ideas, grant applications and plausible dissertation subjects.

This took a few hours to figure out. But I think that I have a story to tell with the core of my research agenda being something like this.

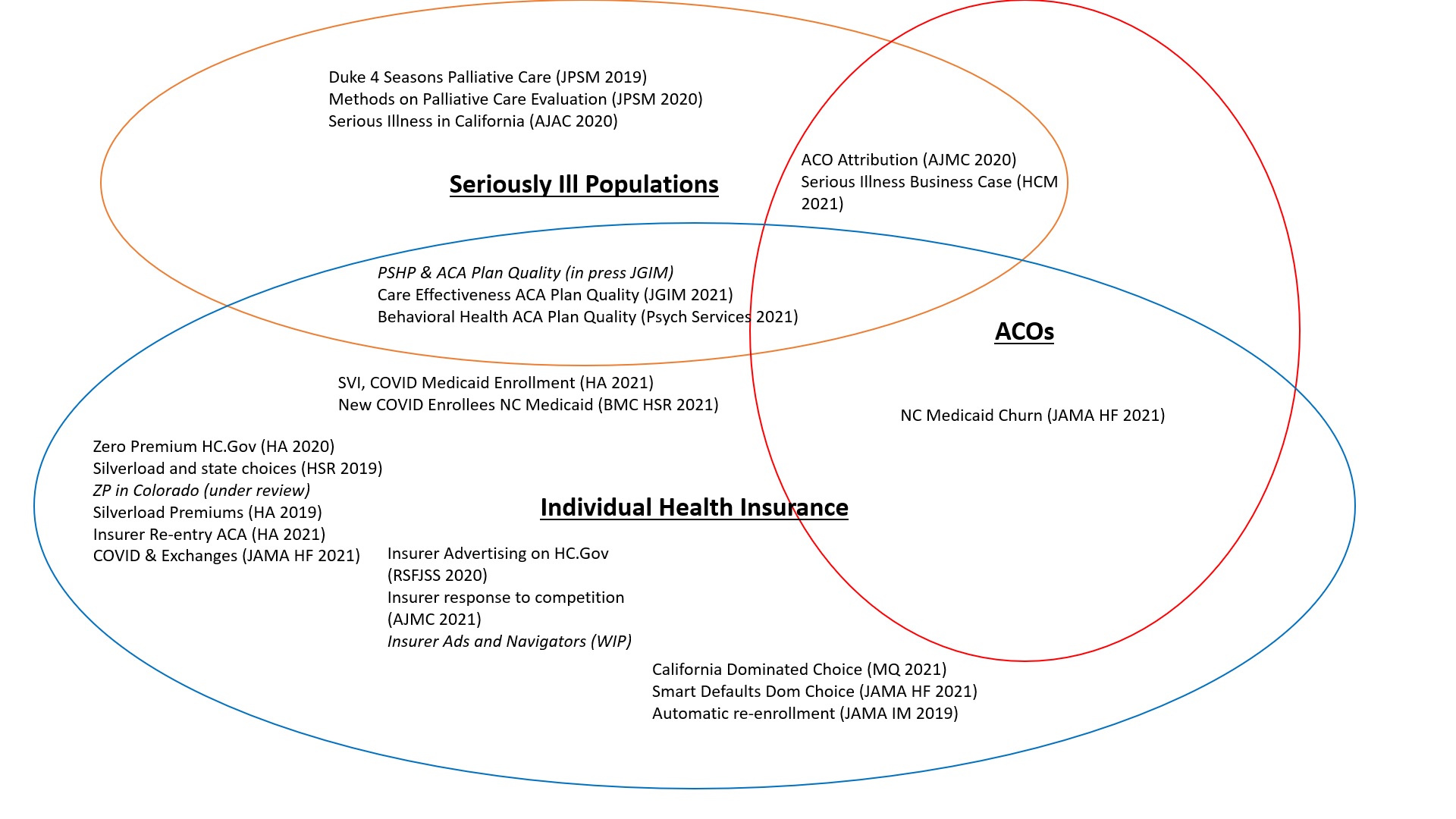

I am fascinated by the individual health insurance markets and how individuals interact with complex choice environments as well as how risk bearing entities, including insurance markets and accountable care organizations respond to incentives and structures to attract or repel individuals with significant care needs, specifically those with serious illness.

I think this mostly hangs together.

Serious illness is what I was brought down to Duke to work on originally. We evaluated a demonstration program for pre-hospice palliative care and produced two papers on the finding that the design decisions precluded us from saying much. We also looked at insurance coverage of seriously ill individuals in California and found, as expected, significant selection to the least restrictive plans. Serious illness is a critical component of attribution for population health models such as Accountable Care Organizations (ACOs) as seriously ill individuals may face higher mortality risk so the decision on attribution models will substantially shift incentives. These incentives may encourage ACOs to either ignore the seriously ill or take steps to attempt to attract and care for the seriously ill if they are likely to be profitable net of risk adjustment. Within population health programs, figuring out churn is crucial (and a few more papers to be submitted before March Madness).

The US is moving towards individualized choice insurance markets from Medicare Advantage, Medicaid managed care, ACA and the likely increase in ICHRA penetration in the group markets. Understanding how non-elderly individuals interact with choice is critical. I have several strands of research in this domain including a premium and enrollment domain. The ACA has had significant price and policy shocks that have led to many different people seeing many different prices for various products. Transaction costs are significant. Information is critical for people to make choices. Individuals with high care needs may care about quality ratings in their decision process, so we have looked at factors associated with different quality scores. Medicaid managed care entities tend to have below average measured quality. Public information builds awareness. We have looked at how people respond to changes in elite messaging from supportive to oppositional, changes in television advertising and enrollment levels, as well as insurer responses to changes in competition and navigator funding with their advertising. Finally, once people are present to make decisions, substantial behavioral and cognitive hurdles remain. Automatic re-enrollment lowers complexity costs but can lead to objectively inferior choice while improved policies can continue to facilitate automatic re-enrollment while improving choice quality.

My future research will examine shenanigans, selection and screening for and against marginalized populations as well as seriously ill individuals and groups that may or may not risk adjust well.

Baud

I like animal videos.

satby

I look forward to posts on this. I have a friend who is rapidly approaching the end of his life, and his poor wife is struggling with understanding what is covered and what is not on his Medicare Advantage program. It just shouldn’t be that hard, and the main incentive for insurances should not be to save money by denying legitimate claims. But they do all the time.

Math Guy

Do you ever view this issue through the lens of game theory? Perhaps it is possible to implement a correlated equilibrium that “optimizes” the exchange market.

OzarkHillbilly

@Baud: I like working with wood. I also like the dark. But I don’t like working with wood in the dark.

Hmmmmm…

David Anderson

@Math Guy:

Next year’s electives

Another Scott

Thanks for this. What I’m seeing is something similar to what good dentists used to say – “I’m working to put myself out of business.” Meaning when dentistry is successful, tooth decay and all the rest will be over. The sensible endpoint is a huge overhaul of the US system with fewer for-profit gatekeeping entities.

Your work demonstrates the fundamental conflict among the current US for-profit health insurance system, universal healthcare, affordability, access, fairness, efficiency, and sustainability. I’m glad you are so good at it, and are sharing it with us.

Typo?

Paying, perhaps?

Thanks again.

Cheers,

Scott.

Betsy

I just want to be covered for medical care when I need it. I’m overwhelmed by decision and choice. Why does everything in American have to be hard?

WaterGirl

You are indeed a lucky man, being able to say “one of my mentors”! Many of us have only one, and have none. Not totally luck, I am sure, but definitely fortunate.

Now I’ll read past the first 5 words.

Wag

Holy mackerel, you’ve got your (academic) life laid out for the next few years. Fascinating set of questions you’ve proposed.

narya

@David Anderson: I loathed game theory, and my reasons for doing so may relate to what you put in the Venn diagram. That is, part of the challenge, as I understand it, is sorting out how to create a sustainable health care system, which means (a) understanding the players (Medicare and other health insurance providers are the big dogs, IMVHO; so much is based on CMS’s calculus, and that drives providers’ decisions) as well as (b) creating reasonable paths for folks to be able to follow to maintain their health and not go broke. I thought game theory removed certain kinds of complexity, but those very kinds of complexity are inherent in the systems you’re analyzing.

I’ll note that I’m starting to figure out what I need to do for Medicare, as that eligibility isn’t too far away, and it is STUPID HARD. I have a freaking Ph.D. and I frequently get completely lost, even on sites (like the government’s) that are pretty good. Sure, here are the details, but WTF will it COST me, and what will I GET?

And then there’s the question of folks who are very sick and under-insured, or folks who are just poor, but whose poverty leads to worse outcomes and care that ends up being more expensive–generally to a government entity–when they finally GET care.

Sorry; that was mostly ranting! I can’t wait to see what you do–I hope you do a simplified version for us jackals! I found, when writing my dissertation, that having my (autodidact, high-school-educated, very smart) dad as my ur-reader really helped me clarify what I wanted to say and remove unnecessary jargon.

Nelle

This is timely as I was listening to the Hidden Brain podcast on choice architecture this morning. One of the examples was on how choice is set up on the ACA site. Instead of the path of least resistance for the consumer, it is the path of least resistance for the insurance company. The researchers estimated an approximate 9 billion (over a year?) on unnecessary insurance.

Do you have a recommendation for a primer on when and how the US turned to for-profit health care – I don’t need anything lengthy or complex – but this is insane, especially after living under National Healthcare in New Zealand. As a friend there said, “What kind of barbarism is it that sees it okay to profit off of the sickness of others?”

David Anderson

@Nelle: I think the better frame to your question is —

“How and when did the US not turn to non-profit/utility/government models of healthcare finance for significant chunks of the population unlike many other OECD nations….”

Going that route, then The Political Life of Medicare by Oberlander (https://www.thriftbooks.com/w/the-political-life-of-medicare-american-politics-and-political-economy_jonathan-oberlander/557853/item/47513910/?gclid=Cj0KCQiAosmPBhCPARIsAHOen-O7CgpuELY7oEwXSkdes9bZtC0TpjC45HcqUjstC_Z9prTF-PpKpC8aAtGGEALw_wcB#idiq=47513910&edition=5304194) is not a bad spot to start

David Anderson

@narya: I agree that game theory is often a simplification of reality but at times, I think it is a usefully wrong set of simplifications, especially on the insurer offering side.

narya

@David Anderson: Oh, I can see how that framing could be important! “Usefully wrong” could lead in very interesting directions.

stinger

So your dissertation topic will be shenanigans? I like it! “He holds the PhD in Shenanigans.”

MazeDancer

Any topic or area of focus you choose will, no doubt, greatly benefit from your study.

In your copious spare time, consider ruminating “Passivity & Privilege” and “Chronic vs. Not” in how people choose healthcare.

The first is about how when presented with too much complexity, people who have the means, choose over-coverage. Which is why Medicare Advantage plans are popular. Even when people don’t need them.

But if they have them, they are sure enough going to use the coverage, almost recreationally.

The second is about how people who are not among the millions who have “mystery illnesses” that cannot be diagnosed, much less treated, by conventional means of drugs and surgery, have no idea what real life is like.

While I am saddened they have joined the ranks of Chronic Lyme, Fibromyalgia, Chronic Epstein-Barr, ME/CFS, and other unnamed sufferings, perhaps people with long COVID will help stimulate research and erase the “there is no such thing, It’s all in your head” status associated with those conditions.

Nelle

@David Anderson: But wasn’t there a time, 1972, where the US explicitly ruled that healthcare could be for profit? Folk tales? Bad memory? (I was hoping to blame Nixon, et. al.) How does that relate to Medicare? I best get the book, right?

David Anderson

@stinger: Yep, shenanigans will be the fundamental view of my dissertation (at least this iteration of a proposal that I don’t need to submit until Fall 2023). I’m thinking about risk adjustment, network tilting and information dissemination and how they all interact with risk, chronic illness, embedded disparities (racialized and medicalized) and market dysfunctions.

I don’t think I have a Hookers and Blow dissertation but that was on the agenda for about a year.

David Anderson

@Nelle: Nope, healthcare in the US has always been profit seeking with a parraellel public/non-profit/religious provision component. Nixon IIRC signed legislation making HMOs way more common but insurers pre-Nixon could and often were for-profits and physician groups were overwhelmingly small businesses that sought to make money to buy the mistress a Mercedes.

Ohio Mom

I suspect this isn’t what you mean by “individualized choice insurance markets” but the individualized choice for Ohio Son’s coverage I prefer is traditional Medicaid. But it looks like he will be pushed into a managed care plan sooner or later.

I can only assume there is a kickback somewhere in this scheme, this bring Ohio.

Lobo

I often talk about how stories are essential to success. Lots of discussions on how fascinating research gets buried in the dullness of academic speak. If you don’t mind a suggestion, I would start your story with:

I am fascinated by the individual health insurance markets and how individuals interact with complex choice environments as well as how risk bearing entities, including insurance markets and accountable care organizations respond to incentives and structures to attract or repel individuals with significant care needs, specifically those with serious illness.

and then end it with your punchline:

My future research will examine shenanigans, selection and screening for and against marginalized populations as well as seriously ill individuals and groups that may or may not risk adjust well.

Your use of the word “Shenanigans” makes it relatable to the public with a chuckel. Most of us have experienced the “shananigans” you talk about. Thanks for doing this!

Ohio Mom

@MazeDancer: When I was researching Traditional Medicare vs. Advantage plans, one thing I found out is that if you ever want to switch from your Advantage plan to Traditional Medicare and you have acquired a serious illness (perhaps that illness is the reason you want to switch because your specialist is out of network), you may not be able to get or afford a Plan B.

Plan B underwriters will either charge you a lot more for your expensive newly-acquired illness, or decline to cover you altogether (if you had turned 65 with that illness already established, the underwriters have to accept you nevertheless).

I don’t know why anyone of any means would prefer an Advantage plan — they are in a position to afford the extras — gym memberships, vision coverage, etc. — on their own. But advertising and the promise of a bargain are powerful.

For years (especially pre-ACA), I looked forward to reaching Medicare age, thinking it a golden age of freedom from pre-existing condition clauses. Not so, it turns out.

David Anderson

@Lobo: I like that edit. I will take it.

narya

@David Anderson: I want to read this dissertation. Even though these things are NOT my areas of great expertise, I will also volunteer to be an editor when the time comes. (I was a freelance copyeditor & proofreader for several years.)

J R in WV

David’s original post says:

And that’s why we love his work.

Scholastic analysis of shenanigans, what’s not to love?

Nelle

@narya: So very generous!

Nelle

David, are you familiar with psychologist Eric Johnson’s work on choice architecture? I’m not, myself, but Shankar Vedantam talks about it in this episode, https://hiddenbrain.org/podcast/choose-carefully/.

Poe Larity

David, have you covered whether insurance providers can have different rates depending on Covid vaxing?

Lobo

@J R in WV: That’s right. David will be soon be known as Mr. “Shananigans.” Of course, he will have to explain that to his partner. ;)

David Anderson

@Nelle: Yep, I’ve cited him on several papers

David Anderson

@Poe Larity: Lightly…. https://balloon-juice.com/2021/08/26/delta-delta-and-wellness-programs/

and

https://balloon-juice.com/2021/07/29/medical-underwriting-and-non-vaccinated-covid-cases/

Poe Larity

@David Anderson: Thx!

BurntOutDoc

I have an ACA plan on the West Virginia exchange, and it’s shenanigans all over. The 2022 annual premium for a (repurposed narrow-provider list Medicaid-like) silver plan with a $6,000 deductible is $20,000. I didn’t get the plan with dental and vision like I had last year, because they don’t have ANY actual providers – if I called the dental/vision office, they said they couldn’t get paid even if they were on the list of providers, and thus couldn’t see me. I’m 62, and need cataract surgery and an overdue colonoscopy, but these things will have to wait until I’m 65 / on Medicare. My longstanding ophthalmology group in town isn’t in plan, and there is no colonoscopy provider anywhere near where all four parts (gastroenterologist, anesthesiologist, surgery center, and pathologist) are in plan. Plus, it’s a follow up colonoscopy 5 years after the last one, so it’s diagnostic, not preventive. “Out-of-pocket limits” are a farce since they keep track of it in such an error-packed way that you never reach it. I picked the lowest premium plan because I know I will never use the insurance unless “hit by a bus”. Actuarial value on health insurance and lottery tickets doesn’t give me any real world information. They may have had record enrollment in the ACA this season, but there will be a high dropout rate as well soon to follow, due to patients recognizing they don’t get anything for their premium unless they are high utilizers.