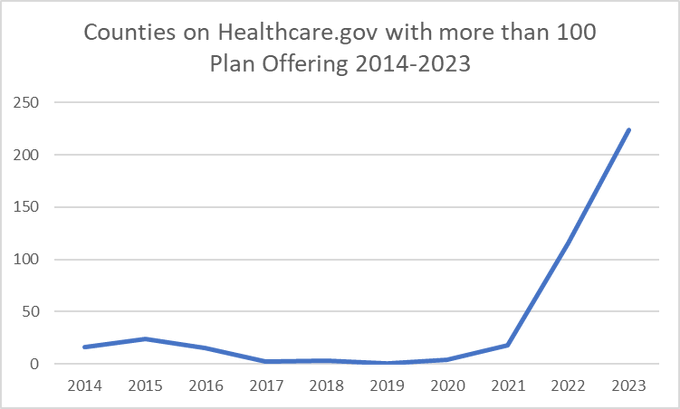

I gave a short talk earlier in the week to a bunch of ACA nerds. As I was prepping my slides about choice complexity, I created a graph showed something that I sort of had realized but not actually seen or fully internalized:

We know that picking insurance is really tough. The Medicare Advantage literature suggests that choice quality goes down hill rapidly after people see 15 or more choices. Some of my ongoing research looks into administrative burdens and choice frictions that lead to sub-optimal choices and dominated choices. We’ve talked about the increasing proliferation of large choice menus before. The work that I did with Patrick O’Mahen looked at the population with at least 50+ choices and in 2021, that was about 45% of people were exposed to 50+ choices and when I did a short off the cuff update, 2022 saw 67% of people seeing 50+ choices.

I had not realized that the count of extreme menu lengths were becoming so much more common over the past couple of years. I had known that big cities like Miami and Houston had ridiculous menu lengths but in 2023, about 10% of all Healthcare.gov counties have very large menus.

When I poked at the causes of this menu length expansion, it is a bit of everything. More insurers are entering markets on average. Each incumbent insurer is adding a couple of extra plans per year per county. And some of the insurers that are expanding their footprints have a historical strategy of “stacking the shelves” with a lot of nearly similar plan variants.

Yutsano

The FEBHP has a bunch of plans available every open season. If I open up the comparison tool I get lost and that’s only about 10 or so. I can’t imagine how one could navigate dozens of options so similar to each other!

Ohio Mom

Never had to wade through the ACA Marketplace but I will say there is an overwhelming amount of choice in selecting one’s path through Medicare, even after you exclude all the Advantage plans. So many Medigap plans!

You can get stuck in the woods comparing the numbers but then you also step back and wonder which insurance company might be easier to work with or more trustworthy (a decision you make on whim).

Choosing a Plan D option is marginally easier because a computer site does a lot of the work. But still, there are snags. My old plan’s price is going up mainly because they don’t like my dry eye drops.

There are some other brands of drops I could plug in to compare but first that means getting in touch with my opthamologist and finding out her opinion on the alternatives.

I know lots of people use brokers to help them sort through all their Medicare choices but then you are back to being overwhelmed, this time about what broker to use, are they smart and honest enough, and so forth.

Of course, bamboozling and exhausting consumers with too much choice is an old retail trick, for starters, on display in every supermarket.

Roger Moore

The more I see stuff like this, the more convinced I am that California has it right with its active buyer approach. I live in LA County, which ought to have a plethora of plans as the most populous county in the country. Instead, I have 39, with about 10 in each metal tier. It seems like a manageable number, especially because it looks like no provider has more than 2 plans in any metal tier, and those have substantial differences, e.g. HMO vs PPO.

Feathers

There hasn’t been any push to limit the number of plans a provider can offer? Seems like an invitation to scam.