One of my colleagues, and co-authors, Farrah Madanay is presenting some of our preliminary research this morning at the National Health Policy Conference on benefit terminology in the ACA. We looked at all the different ways insurers described their first tier, in-network benefits on the ACA individual market from 2014-2020. It is a mess:

Consumers are expected to not only compare plans across insurers, but also interpret benefit concepts with terminology varying from plan to plan. For example, “no cost-sharing” is expressed 24 different ways, including $0 copay, 0% coinsurance, “no charge” copay, and “not applicable” coinsurance. A relatively unexplored topic is the complexity consumers face in benefit concept lexicon across marketplace plans. To characterize this complexity, we analyzed cost-sharing descriptions for all standard component plans using public use files from HealthCare.gov.

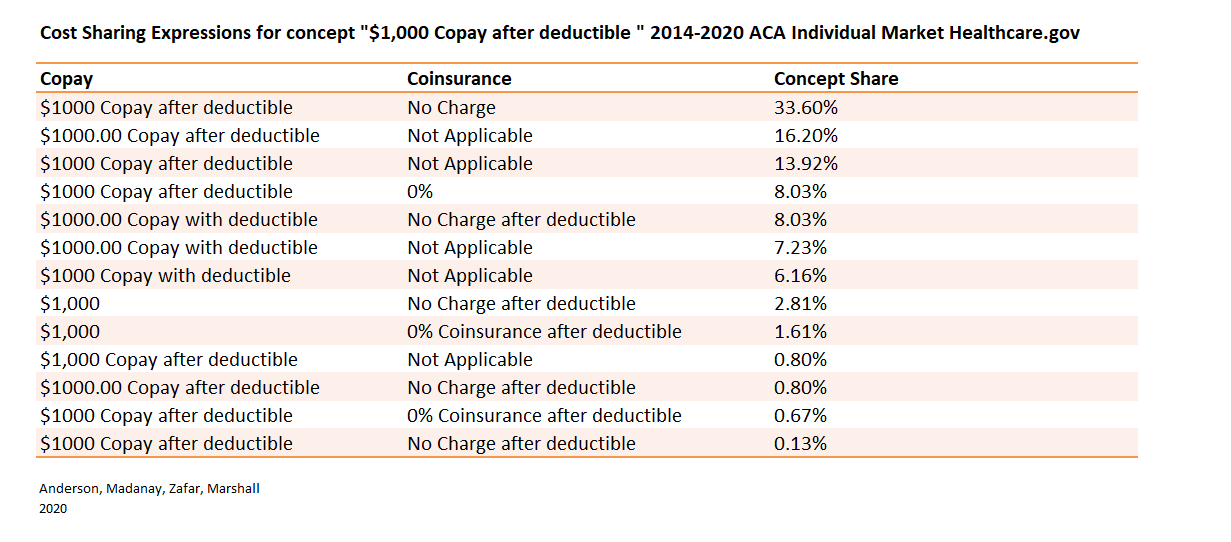

For instance, the cost-sharing concept of “$1,000 copay after the deductible” is expressed in 13 different ways and the distribution of expression is fairly diverse.

We found that most benefit categories (ie “PCP well visit” or “X-rays” or “Emergency Room” etc) have cost sharing concepts that have lots of variants. We are currently looking at the county-year level exposure to see what is happening there (interesting things but I can’t write about it yet).

Choosing insurance is hard. In an ideal world where we expect people to choose their insurance, we expect them to compare networks, benefit structures, hassle/transition/switching costs, and then also integrate those projections against a probabilistic projection of future healthcare needs that is not uniformly weighed. That is a tough challenge in an ideal choice environment.

We are showing that the ideal choice environment does not exist as people are also expected to translate how Blue Cross describes their benefits against how Aetna or UPMC or Centene describes their benefits. These are tough things to do when most people aren’t spending all day thinking about health insurance; they leave that to geeks like me.

Choice is tough in the best of cases, and we’re not in that universe.

RSA

This looks like a good problem domain for application of concepts and techniques developed for the Semantic Web.

MattF

I guess the alternative is to specify some set of plans and have insurance companies price them.

OldVet

What is the point of this article? The Republican Party assures me that everyone loves their insurance company. /s

OldVet

@MattF: I guess an alternative is to go to a single payer system that minimalizes the role of the for-profit medical insurance industry.

WV Blondie

To the insurance industry, this is a feature, not a bug! They want folks to make bad (i.e., more expensive, less covered) choices. Is anyone surprised at this?

Spanky

FINALLY! Somebody addresses (one of the many) elephants in the health insurance room that trips people up. By design.

Thanks, David, to you and your colleagues.

frosty

@MattF: This is precisely what Medigap does. All the plans are the same, pricing is different.

David Anderson

Don’t attribute to malice what can be explained by individual tech writer trope preferences….

We are testing whether or not there is in-company/in-corporate parent variation in expressions as we think there is a damn good chance that most of this variation is the Cigna tech writer style guide says X and the BCBS-Michigan tech writer style guide says Y for the same concept.

frosty

@OldVet: I like single-payer as an alternative, not necessarily without the private insurance industry though. That’s what my son’s Medicaid plan is. Paid for by the state, choice of insurers and doctors.

frosty

We started out expecting to get a Medicare Advantage plan. MA is private PPO or HMO insurance and is as described above, a CF to try to figure out. And it doesn’t work at all if you live on a border and your insurance is in one state and your docs are in another.

It took me three months to navigate this mess from the first seminar until I got my cards. I have friends who ran an insurance agency and it took them two tries over a year to figure out what plan worked best for them.

We went with Medigap G because of the cross-state issue and because we expect to be traveling a lot. It cost us $1,800 a year more than the MA plan we’d picked out.

M4A -ptui! We can do better.

Jager

I have a friend who has been going through serious medical issues for over two years. He has Medicare and his supplement is from Blue Cross of Nevada. He’s a retired hospital administrator and he can’t figure out the billing.

Villago Delenda Est

National regulatory agency for health insurance imposes definitions that all providers must use. They will whine, but fuck the greedy Ferengi idiots.

Bard the Grim

How hard would it be, if insurers were forced to provide appropriate standardized data for each of their plans, to write a program where buyers could play around with variables (number and age of family members, probability of getting pregnant, needing surgery, etc.) and get a simplified comprehensible assessment of each plan? And what are the prospects for states and the federal system putting such requirements into place?

Kelly

@frosty:

I did not know that. Next year I age into Medicare. A vast new research project and I just got comfortable with Obamacare.

Just Chuck

@Bard the Grim: I’m a developer on precisely such an app (no url, not sure if they want it shared publicly yet). You enter your basic household info, zipcode, and which services you’re likely to need in a year (like chiropractic, mental health, oncology, etc) and it comes back with a list of plans sorted by out of pocket expense.

The plan data actually is standardized and public — it’s called HIOS (Health Insurance Oversight System).

Bard the Grim

@Just Chuck: That’s awesome! Both for standardized data and your code. Are there other apps, or is yours the first? Will it be public/free? How useful do you think it is? If you can tell us, who paid to develop it and why?

Adam Lang

…$1000 copay after deductible?

What in the world has a $1000 copay after the deductible?

ProfDamatu

@Adam Lang: I’m guessing that would be some niche case; basically, spending in between your deductible and out of pocket maximum – only thing I can plausibly think of where it would make sense for it to be a copay like that rather than just coinsurance might be an ER charge. So, for instance, maybe if you haven’t hit your deductible yet, you might end up paying the entire (say) $5000 ER charge, while if you’ve satisfied your deductible but not hit your OOP max, your copay for using the ER might be $1000. Seems odd to me too.

David Anderson

@Adam Lang: Inpatient hospitalization or MRIs or specialty drugs would be my guess (I have not memorized the data)

Barbara

Just parking this here. You probably already have seen this, since it is put together by UNC, but this is a terrific visual of what has been happening to hospitals over the last 15 years. With more than 150 closures, all but 30 are in Southeastern states. Source

Brad F

@Adam Lang: What shocked me is i had to scroll to #17 to find the question I wanted to ask. I look at this stuff as much as the next guy–and I thought i was nuts. “What in the world” is right.

Just Chuck

@Bard the Grim: The company’s called Clear Health Analytics. I don’t know all that much about them (I work for a small company writing their API code). The site is free, so I would guess they do consulting, maybe charging for API use.

I have to imagine there’s other companies doing the same thing, since the data is public. CHA’s secret sauce would be their service cost model, a bunch of opaque mathy stuff that factors into the overall predicted costs. It looks pretty useful, though not to me, since it’s for the national exchanges, and I live in a state (CO) that has its own system.