There are strong rumors that President Trump will issue an executive order that will allow individuals to buy association health plans. These plans are not regulated by the ACA, instead they are regulated by ERISA. If the executive order or the subsequent rule making that comes from the order are upheld in court, these plans would be allowed to medically underwrite and risk rate their premiums.

So what does that mean for people who are looking to buy insurance on the individual market?

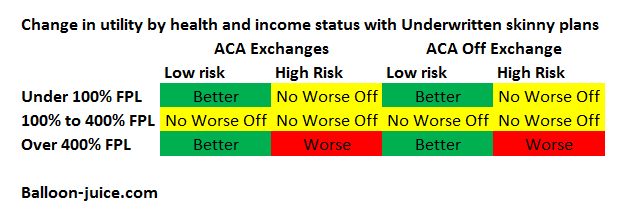

We need to split the universe of buyers into two risk groupings:high risk and low risk. Low risk individuals will get good underwritten rates and high risk individuals will get bad underwritten rates. Risk can be a function of medical history, hobbies, zip code, age or any other factor that an insurer has ever used to divide their risk pool. I think that we also need to divide the universe into three income groups. People who make too little for Exchange subsidies, people who make just enough for Exchange subsidies and people who make too much for Exchange subsidies.

I want to look through the distributional implications prospectively first:

People who receive Exchange subsidies will be no worse off. They can still get community rated, guaranteed issue, comprehensive insurance at a subsidized price. Some people among the low risk groups will move from the ACA Qualified Health Plan (QHP) to underwritten insurance as it is a lower premium and they are healthy enough to take that risk. This decision will be a function of county specific pricing strategies, individual incomes and individual risk tolerance. And if someone drops out of the community rated pool in the first year and then becomes high risk during that year, they can cheaply re-enter the community rated pool at the next open enrollment.

People who make too little to qualify for an ACA subsidy have mixed results. Some will be no worse off as they can stay on Medicaid in Expansion states. For people in non-Expansion states, the High Risk people will be no worse off as they won’t be able to afford an underwritten plan so they are either staying with their current full price ACA plan or are not covered. It does not make these people worse off. For Low Risk people who make too little to be subsidized, they are better off as some can afford a donut design bare bones, underwritten plan. Most people in this group won’t see an improvement, but some will.

The big distributional consequences are for the people who make over 400% Federal Poverty Line (FPL) and are either uninsured or in the individual market. Right now they are the only group of citizens who get no help for their health insurance. QHP coverage is expensive because it is community rated and guaranteed issue.

Individuals who are prospectively low risk are far better off. They can get much cheaper coverage in an underwritten pool solely due to group composition as there are no individuals with recurring million dollar claims. Premiums can be even lower if benefits become skimpier. I am at a stage in my life where my family could handle a super high deductible plan with no maternity coverage. If I did not have coverage through work, underwritten plans would be good for my family compared to QHPs.

However underwritten plans make high risk people who make too much for a subsidy worse off. They still have access to full price, no subsidy guarantee issue, community rated insurance. However the premiums for those plans will be higher. Most of the healthy non-subsidized population will have left the pool and a segment of the low risk, low cost subsidized population will also have left the pool. Individuals who make just over the subsidy threshold of 400% FPL will have very strong incentives to engineer their income to look like they make just 399% FPL. Other individuals will be facing implicit confiscatory marginal tax rates for every dollar they earn above 400% FPL. This groups will be worse off as they either face higher premiums or dump income until they qualify for subsidies.

So what is the political theory behind these changes? It is a simple theory that we can look at from a single graph. The graph below is old data, from 2002 but recent updates confirm the data.

Most people in most years have below average costs. This is especially true when we limit the population to people who are not covered by Medicare or Medicaid as those act as de facto limited high cost risk pools already by covering those who are old, those who are disabled, and those who need long term skilled care.

Most people are low risk and the Exchanges can hold most of the high risk people harmless especially if states actively manage their exchanges. The people with political power who are prospectively hurt under this proposal are people with significant pre-existing conditions (including age) and who make more than 400% FPL. The pain that these people feel will be real but they are already in pain due to their current non-subsidized coverage while they lose allies of low-risk high income individuals who are now better off in underwritten markets.

Fred Fnord

…donut design?

TK

I anxiously await the slew of lawsuits GOP Attorney’s General will file to challenge the illegal rule making of this administration with regard to this law.

rikyrah

thanks for the info, Mayhew

MomSense

Part of the problem when dealing with this topic is that it is so complicated. As soon as you start talking about actuarial values in a persuasion call people lose interest fast. I keep trying to come up with language to explain these concepts.

Bobby Thomson

I’m confused. This isn’t absurd on its face and I’m not understanding how rich people can gain the system to get richer.

dr. bloor

@MomSense: People are typically less interested in understanding the Big Picture and just want to know how it will affect them personally. And, as David points out, this design minimizes the number of people who will be highly motivated to break out the torches and pitchforks.

daveNYC

FYI:

2017 FPL Guidelines: 48 Border States and D.C.

(For households with more than 8 persons, add $4,180 for each additional person.)

Persons in Household 2017 Federal Poverty Level Medicaid Eligibility (138% of FPL) Premium Subsidy Threshold (400% of FPL)

1 $12,060 $16,643 $48,240

2 $16,240 $22,411 $64,960

3 $20,420 $28,180 $81,680

4 $24,600 $33,948 $98,400

5 $28,780 $39,716 $115,120

6 $32,960 $45,485 $131,840

7 $37,140 $51,253 $148,560

8 $41,320 $57,022 $165,280

Good job with the formatting there WordPress.

Fair Economist

Having healthy people move off the exchanges while the sick stay is going to raise the government’s costs. Do you have any estimates of the budget implications?

Another Scott

Isn’t the big problem, though, the (apparent to me) issue that this is a “camel’s nose” that is part of changes designed to break Obamacare? Without community ratings, what’s to keep insurance companies from greatly expanding the definition of “high risk” and shrinking the definition of “low risk”? What’s to prevent the “no worse off” groups from actually being worse off (no contraceptive coverage, etc., etc.)?

I’m having trouble seeing any sort of long-term silver lining here.

Making affordable universal health care access less affordable and less universal (for even a subset of the population that can’t afford it) is not the way to go.

(I do understand that you’re not advocating these changes, just saying how they would play out in a rational world….)

:-/

Cheers,

Scott.

David Anderson

@Another Scott:

For people who are eligible to receive subsidies on the Exchange and buy a QHP, they are no worse off as their benefit packages are secured by Title 1 which requires 60 votes in the Senate to re-open. For people who make over 400% their current options are an subsidized QHP, a healthcare sharing mininistry with Pre-ex and benefit limitations, short term coverage with significant limitations or running naked. Underwritten coverage with limitations expands the option space. I am making a strong prospective rational choice assumption that adding to the option space does not make people worse off in and of itself.

The biggest political challenge for the ACA is the cluster of people who don’t have pre-ex conditions and make more than 400% FPL, especially in a world where half the states are going to Gold Gap in 2018 which helps the 200-400% FPL population a lot. These are the people who generate the “They pay $40,000 premiums for a $15,000 family deductible plan” headlines (and those cases are real and can be found) . This would make this group much better off. The big losers are the over 400% FPL with pre-ex conditions or high risk. They are even more SOL but it is incremental SOL instead of brand new SOL.

Another Scott

@David Anderson: Thanks.

While browsing LOLGOP on Twitter, I came across Gaba’s take (which mentions you). For others out there:

Emphasis added.

Anyone willing to bet that the Teabaggers won’t demand cuts in “unaffordable Obamacare subsidies” as soon as they start rocketing skyward?

:-/

Cheers,

Scott.

dr. bloor

@David Anderson:

Within three years, you’ll be reading a story about some upper-middle class guy who went naked, and is putting the squeeze on his life insurer to cover treatment costs for some serious, life-threatening illness.

Downpuppy

@Another Scott: I figured that the “No Worse off” high risk subsidized meant the US would have to pick up the tab. Thanks for bringing the confirmation.

Matt

@David Anderson:

The really messed up part is that any member of that first group can transform into a member of the SOL group just by stepping off the wrong sidewalk at the wrong time.

sharl

Ain’t that the truth! I’m convinced that getting the details right without sucking the enthusiasm out of the room is extremely difficult at best, made more difficult by the fact that the various political and policy components are constantly moving targets.

I’ve been following young leftie health policy activist Tim Faust, who has the enthusiasm bit down cold, but isn’t on the same page as David for a couple* of reasons (*at least), one of which being that his focus is more on the long term goal of getting single payer.

He’s basically a big fan of Sanders’ approach, while noting that he thinks it needs some improvements. [He was an ACA enrollment volunteer in Florida in 2013 – a Medicaid non-expansion state – and having to tell people “sorry, you’re not poor enough to be eligible” ultimately radicalized him in favor of what he is now supporting.]

He explains the basics of what he is doing in this hour-long podcast with Ana Marie Cox (note – a few long commercial breaks in that interview). I found it pretty informative, and I don’t think it would be as irksome for B-J folks as some of the other forums where he shows up (e.g., the Chapo Trap House podcast).

I still need to dive into the tall weeds on this topic myself, as well as more into Faust’s stuff – like his recent post in Jacobin – but in the meantime I wonder if there are lessons that can be learned from his activist/evangelical approach toward health care reform. His target audience is younger people, who inherently/subconsciously make different risk-reward calculations than older folks like me. As such, I don’t know whether his message and approach would be usable for older folks even with massive rhetorical retooling. As I noted, I still need to sit down and dive into his stuff (and more into David’s writing as well, for that matter).

Hard, hard stuff…

sharl

@sharl: As a side note on Tim Faust, I just remembered how I first came to know about him. He was the creative genius behind the “Ted Cruz is the Zodiac Killer” t-shirts. Proceeds from the sale of those shirts went to fund abortions for poor women in Texas (via the El Paso-based West Fund). That was a pretty successful campaign as I recall.

Jerry

Question for those that would know:

A friend of mine up in Michigan really should go see a doctor because of something going on with him, but he claiming that since he’s on “the Obamacare Medicair extension,” the doctor won’t perform any tests to find out what is wrong with him. Is this factual?

sharl

@Jerry: Unfortunately I’m no help on your question, but David – and maybe some of the other commenters who are wise in the ways of our effed up health insurance system – will hopefully be able to answer, or at least ask the kind of questions necessary to get any missing key information.

David typically posts every week day, early through late morning, so if you are able to repeat your question in one of his new posts there’s a better chance he’ll see it. If I’m available when he has just posted anew, and you are not around, I’ll copy your inquiry and repeat it in that new post. Otherwise I’m afraid the odds of it being seen in this (now) old thread are pretty low.

David Anderson

@Jerry: First pass, it sound extremely unlikely. What the research shows is that usually a Medicaid patient will have a harder time getting an appointment to see a doc but once the doc seems them for an acute event, insurance does not matter much on diagnostics. This will change for chronic events and high cost events.

But on first glance, this smells fishy to me

Jerry

Thanks David. My first thought was that he was lying. Then it occurred to me that his doctor is an asshole.