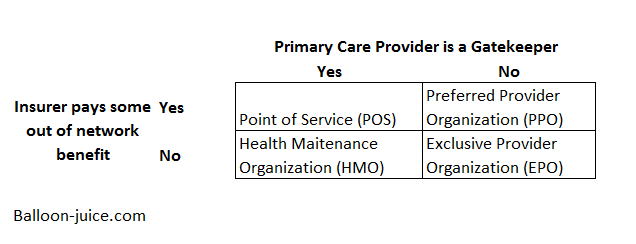

During the open enrollment periods that many people either are in or will soon be in, plan types will be offered. There are four primary plan types that are commonly offered and knowing the trade-offs in these designs would be useful. Fundamentally each of the four plan types is a unique answer to two questions: Does the plan require a Primary Care Provider (PCP) to act as a gatekeeper AND does the plan pay some non-emergency out of network benefits? The directional answers to those questions will define plan types.

Point of Service (POS) plans require patients to go through their PCP for referrals to specialists and elective procedures. There is an established network of contracted providers that will take payment in full from the insurer’s contracted rate but the patient can go out of network and at some point, the insurer will pay some proportion of the out of network claims costs.

Health Maintenance Organizations (HMO) are the most restrictive plans. There are no out of network benefits and patients are expected to go through their PCP before they see any expensive entity.

Exclusive Provider Organizations (EPO) remove the gatekeeper requirement from patients. If someone wants to see a specialist, they can call and get an appointment in the network without worrying about denial of payment due to the lack of a pre-authorization. EPOs don’t pay for non-emergency out of network care.

Preferred Provider Organizations (PPO) are the least restrictive plan types. There is no gate-keeping requirement. Out of network benefits are also available. The out of network benefits tend to be far skimpier than the in-network benefit structure.

These are ideal archetypes. Some insurers will offer HMOs that function a lot like EPOs with very light pre-authorization and gatekeeping requirements. There are also PPOs that look a lot like POS in practice. Finally, I am not mentioning indemnity plans which are network agnostic and pay out fixed fees for services. Those plans are rare.

These four plan types are functional objects. Any network can be attached to any plan type. A narrow network could be attached to a PPO while a national network can be attached to an HMO or vice versa. The same network can be attached to both the POS and HMO offered by a particular insurer. An HMO, an EPO and a PPO can all have identical in-network benefit structures of identical deductibles, co-pays, co-insurance, service limitations and out of pocket maximums.

A policy is effectively a combination of a plan type, a network and a benefit design. PPO and POS plans will have more complex benefit designs as they must have some type of out of network benefit in addition to the in-network benefits that all four types of plan need. There are an almost infinite combinations that can be assembled between these three elements. This increases the complexity of choice during Open Enrollment as individual preferences vary and the trade-offs between an HMO and a PPO will vary dramatically between individuals. The trade-off between a higher deductible and lower premium HMO may be worthwhile for one person while a lower deductible and higher premium PPO is more attractive to a person who wants the option value of going anywhere in case they get hit by a meteor.

PST

Interesting post, as always. Table needs fix on EPO abbreviation.

raven

So, I’m going to outline out situation again. I’m less than a year from retirement and my wife and I are both on BCBSGA HMO. When she broke her arm in Florida we learned that going anywhere but the ER was a big mistake when we were out of state. When I retire my organization gives us a set amount of money to buy insurance and I have to go through AON to purchase insurance. My wife stays on BCBS until she reaches 65, 5 years from now. I’m wondering if I should look at one of the other options we have during open enrollment so she’d be on a better plan. I don’t really know if she’s stuck on what we have when I retire or if she selects during open enrollment.

David Anderson

@raven: First advice — go talk to a broker; some states will allow brokers to charge you an advice fee where they are not selling you anything but you are buying their time and expertise for an hour. That should be your first stop.

Secondly, figure out how valuable out of network coverage is to you and look into the trade-offs.

Butch

So, David, when I lost corporate insurance last June I went on the Exchange looking for coverage; the Bronze plan here basically amounted to buying a premium so I found an underwritten plan. However, for some reason a month later I started getting bills for Bronze plan coverage that I had neither requested nor approved, and it took a lengthy appeals process to get the bills to stop (and protect my credit rating). I’d really prefer a policy that complies with the ACA over this underwritten one, but after that experience I’m a little shy about going on the Exchange and am not sure the price could have dropped enough to make the visit worthwhile. (Bronze plan was $700 a month per person with a ridiculous deductible; the underwritten plan is $350 with a much more reasonable deductible. It excludes mental health and drug addition coverage but we don’t need either.)

raven

@David Anderson: Great, we actually have a Council on Aging with counselors available as well. Nest stop! thanks

raven

Nows that I look at our choices it seems lioke it’s BCBS or Kaiser HMO and folks in these parts aren’t crazy about Kaiser.

rachel

Quick question: is there an authoritative site that tracks changes and rates of changes in health insurance rates pre-and-post-ACA?

Aurona

I continually look for the right plan for my good health 7.1 decades in, and this Medicare year in Seattle, it’s a PPO from Humana with $0 premium, $0 primary doctor, $3600 maximum out of pocket (MOOP), my current PolyClinic, but with no Rx attached. I pay separately for EnvisionRxPlus for about $16 monthly, and I take no drugs. Also this plan has a drip of other benefits (gym, some eye, dental, hearing), but the moop did it for me. I don’t find the preventive dental good enough for me, so I do have a separate Delta Dental plan ($50 premium, $2000 max/beginning 2nd year, $0 copay). So for $66 a month, I feel this is the best plan for me. Thanks for keeping me aware and on alert for the changes to both the plans and to my health needs.

David Anderson

@rachel: Charles Gaba at ACASignups.net is pretty close to the go to source

Kaiser Family Foundation is a fountain of knowledge as well.

Humdog

I wish I could find an explanation as to why we have such a doctor shortage. My husband needs a doctor as he let his prior relationship lag for 8 years but there is no doctor in the county accepting new patients regardless of insurance coverage. He is recording crisis level blood pressure readings and his only option is emergency room, when all he needs is a few minutes to write a prescription.

U.S. docs supposedly pull in big bucks so why don’t we have a surfeit of them like we do lawyers? We are importing doctors from outside the US and still not enough GPS. Why aren’t the PTB opening more med school slots? I simply don’t understand.

rachel

@David Anderson: Thanks.

debbie

There are two options at my work. Lower cost / higher deductible vs. higher cost / lower deductible. I choose wrong every freakin’ year. I’m going to stop even trying.

debbie

.