Last night, the Journal of Health Economics published our recently accepted article on zero premium effects in the ACA individual health insurance markets. Coleman Drake was the lead driver of this project, and I had the pleasure of working again with Sih-Ting Cai and learning a lot from Dan Sacks. We asked a very simple question — does seeing a zero premium plan change plan choices and enrollment choices?

Coleman and I had first started thinking about this idea in November 2018 due to a Balloon Juice post on Oklahoma’s weird pricing configurations in twelve counties — gold plans were free. Our first crack at the problem used county level enrollment and pricing data to get a directional estimate. We published in Health Affairs a study that estimated a 14% gain in enrollment for households earning between 151-200% FPL group. We did not detect changes outside of that income bad. A Harvard team using Massachusetts data found that zero premium plans were really important for renewal and retention. However we did not know what was happening at the household level.

Thankfully, the National Institute of Health Care Management (NIHCM), funded Coleman and I to get data from Connect for Health Colorado and Ideon to examine what happens when people are just exposed to zero premium plans or just missed being exposed to zero premium plans. We wanted to use Colorado as they were both happy to share data and there were a lot of policy changes that created a lot of variation in exposure as they went from normal CSR payment, to Broad Loading in 2018 to Silver Loading in 2019-present.

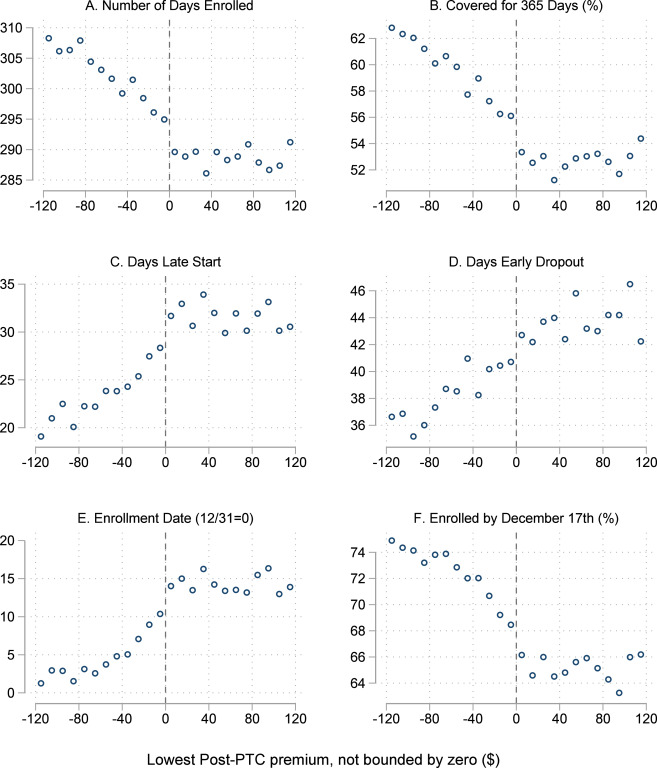

We used a technique called regression discontinuity. We estimated the net of subsidy premium everyone faced. We made a well supported assumption that net premiums varied among relatively similar people as if it was mostly random-ish. We assume that people whose cheapest plan was (before truncation) negative one dollar looked a lot like people whose cheapest plan was $1. We basically compare the outcomes of people whose cheapest plans were just under $0 and people whose plans were just over $0. We’re not looking at people and their choices when their cheapest plans were -$100 or whose cheapest plans were $100 or $300 a month. We’re looking at a very localized effect estimate.

So what did we find?

- We did not find substantial differences in what plans people chose when they saw a zero premium plan.

- Zero price is not particurly special

- Lots of people choose zero only because lots of people choose the cheapest plan possible

- We did not find substantial differences in the characteristics of plans chosen

- We do find a lot more covered days

- Most of this gain is from coverage starting on January 1st for zero premium buyers

This was the big finding for us.

We found a notable change in the percentage of people who had 365 days of coverage (full year coverage) at the zero premium cut-off. We found less mid-year drop-out as well. We found substantial differences in the probability of enrollment by December 17th. The effect was strong for lower income enrollees. This was the key oddity that made us go hmmmmm….

Our original hypothesis was that zero was fundamentally weird and special. It is but not in the way that we thought. What makes zero special is that it substantially reduces transaction costs. People who want to be insured have to pick a plan, make the initial payment and then start the plan. Zero eliminates the middle step.

We think that we did not detect an enrollment effect in Colorado because Colorado always had an open enrollment period that always extended into January. People who made a mistake in December in not setting up a payment had a second chance in January. This was not the case in periods of time of the Healthcare.gov data set that we had used for the initial aggregate effect estimate in Health Affairs. In that situation, there were not always a second chance to correct a mistake.

Administrative burden is big and it is real and it keeps some people who want to be insured from being insured.

CaseyL

Is setting up a payment plan that much of an administrative burden?

Or is it that, for people who have to literally count their pennies to make it to the end of the month, even the smallest premium means they drop the policy? (And possibly more so as they year goes on.)

Keaton Miller

Great work! The zero premium threshold is very interesting. Roughly half the plans in Medicare Advantage are offered at a zero premium (modulo the mandatory Part B premium). For a long time I thought it surely must be demand driven, that there would be strong behavioral effects for consumers wanting to be at that threshold (especially since the kinds of subsidies you are talking about here don’t apply in the MA space I work in). After much exploration, I wasn’t able to confidently/consistently identify any demand effect. I don’t have the detailed day-of-enrollment data you do though. I like your administrative burden story, which would apply to MA.

lee

This is some timely information for me.

My eldest is probably going to get insurance from the marketplace (I’m not sure her new employer offers health insurance). I’m pretty sure if there is a zero premium plan offered in her area (Austin, Texas), she will probably go with it.

lee

@CaseyL:

I can sort of answer this with my kid. She’ll more than likely go with the zero premium plan (if offered here) simply because she won’t have to remember to pay it.

David Anderson

@CaseyL: That story you’re telling would hold true if the people who are exposed to a $-1 plan and the people who are exposed to $1 plans are meaningfully different — we don’t think they are because the rules that generate this exposure are opaque as fuck to the consumer and it is a quasi random assignment to etiehr side of the divide that changes over time, street and .12 cent an hour wage differentials

lee

This thread got me wondering:

Is there a way to view the plans offered in an area without going thru all the initial setup of Healthcare.gov?

lee

@lee:

Found it.

healthcare.gov/see-plans/

Pretty easy to do as well.

David Anderson

@lee: HealthSherpa.com and healthcare.gov/see-plans

are how I poke around for exploratory and confirmatory purposes.

David Anderson

@Keaton Miller: the other story is that $0 is an attention hack as quite a few markets display things in price order so landing at the top of the display results in probably pretty valuable.

Coleman and I have something in progress that we should be submitting soon that plans with this a bit.

billcinsd

How does the 5th Circuit ruling on covering preventative care affect this?

David Anderson

@billcinsd: That is the paper coming out on Monday :)

TLDR: This won’t change the zero premium behavioral patterns we’re finding here. It may change premiums or benefit structures if it is not stayed by either the appeals court or the Supreme Court while the Feds appeal the decision.