Earlier this week Ceci n’est pas mon nym asked a great question in comments:

Looks like it’s flattened out at 10%. Who are those last 10% uninsured that ACA isn’t reaching?

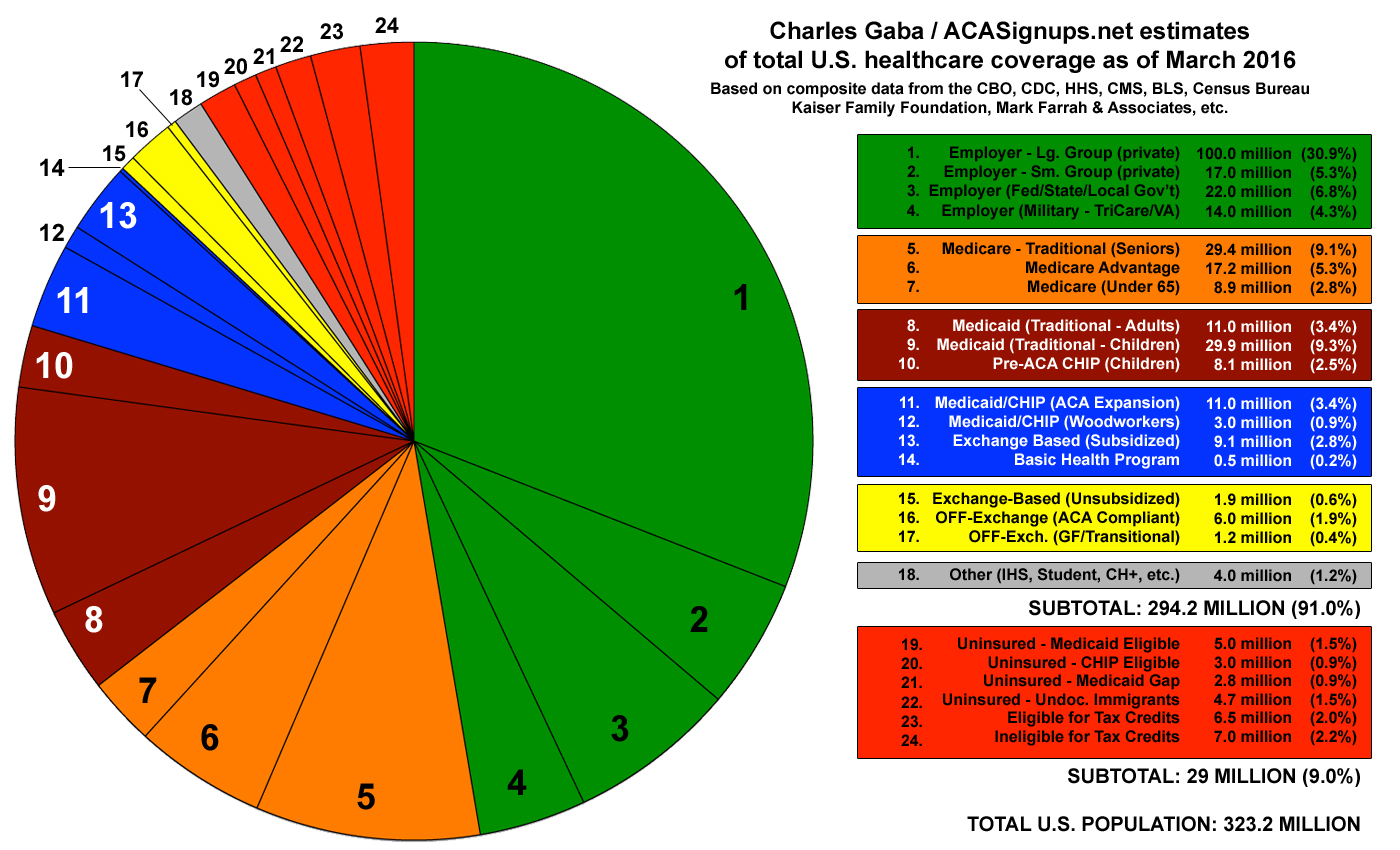

Charles Gaba at ACASignup.net looked into this in 2016 and this is what he has with a little bit of wiggle room.

We can break this 10% down into a couple of groups.

The hardest to cover group are immigrants who either don’t have papers or don’t qualify for one reason or another. This is about 15% of the uncovered population.

The next group are people who either need significant outreach to get into the individual market or they need better deals. This is some combination of the people who don’t qualify for subsidies and are uncovered and people who qualify for subsidies but don’t use them. Here the policy response would be to up subsidies, create auto-enrollment features and otherwise make it easier for people to get in. This might be 25% to 40% of the remaining uncovered.

Woodworkers of a variety of stripes are the next group. These are people who qualify for high actuarial value, low premium insurance through Medicaid, Medicaid Expansion, kids in CHIP, and subsidized exchange policies. They probably make up 35% to 40% of the population. Presumptive eligibility, auto-enroll, auto-renewal, and coordinated benefit qualifications would be appropriate policy responses.

The final group is roughly 10% of the uncovered. This group are the people who make too much for Legacy Medicaid and too little to qualify for Exchange subsidies in Medicaid non-Expansion states. The policy solution is to expand Medicaid to at least 100% FPL.

msdc

David, is “woodworkers” some kind of health insurance parlance I’m not familiar with, or are there really that many uninsured woodworkers? And if so, why is that particular trade singled out?

smintheus

@msdc: I’m puzzled by that too. Is it like code, as “the greeting card business” was in Get Smart?

Or maybe it’s just an autocorrect.

satby

@msdc: I wondered that too ?

Another Scott

Gaba on ‘woodworkers’:

HTH.

Cheers,

Scott.

smintheus

@Another Scott: Ok, so they’re not really people who work wood, they’re more like The Borrowers, tiny folk with mores and needs much like our own, only tiny.

OzarkHillbilly

@msdc: @smintheus: We’re everywhere, and we’re going to get you and your little dog too.

smintheus

@OzarkHillbilly: We have an ominous looking snake out by the stream you can help yourself to…very pretty markings.

Vhh

@msdc: woodworkers are those ppl not easily identified, ie hidden in the woodwork.

OzarkHillbilly

@smintheus: I like snakes, even the poisonous ones.

msdc

@Another Scott: #themoreyouknow

Thanks!

smintheus

@OzarkHillbilly: Well I think you’d love this one. It was sitting there fat and sassy in the middle of road yesterday.

Matt McIrvin

The people trapped in the Medicaid hole in non-expansion states are actually a much smaller fraction of the uncovered than I thought–I figured they’d be the majority.

Matt McIrvin

…I was a little confused by his use of “woodworkers” because previously he’d used it to mean people who had already come out of the woodwork–these folks haven’t yet.

OzarkHillbilly

@smintheus: What was it’s coloring?

smintheus

@OzarkHillbilly: Hard to describe. Series of large almost oval shapes running down both sides, in alternating colors…seemed to be a rust background with green (?) and maybe yellow ovals. I thought it might be a water moccasin.

OzarkHillbilly

@smintheus: Does not sound like a water moccasin, to me, no green and yellow on them. Ours are mostly the dark colored variants with no discernible patterning. Does not sound like any of the north American venomous snakes to me. If it was a pit viper, it would have a triangular head.

Another Scott

@smintheus: When I was a kid in Georgia, I was taught that water moccasins were black, but their coloring varies.

A Mississippi Green Watersnake, perhaps?

Dunno where you are.

Cheers,

Scott.

(Who is constantly amazed how easy it is to search for stuff like this with just a couple of words these days.)

rikyrah

Thanks for the info.

PS- do you think Medicaid for all is better than Medicare for all?

smintheus

@OzarkHillbilly: It does have a triangular head.

@Another Scott: We’re in PA, but this doesn’t look like any of the Pennsylvania snakes I’m aware of.

OzarkHillbilly

@smintheus: Than it is a pit viper. Did you look at the pics on the wiki page? This one is of a lighter variant and shows small dark circles in pairs on it’s side.

Sam Dobermann

@rikyrah: Yes Medicaid much much better.

Incidentally, Medicare has only 95% of seniors even after all the years. 5% will likely not ever be covered. The Amish, etc and the really rich. Some don’t wa to mix with the.commoner

Ceci n est pas mon nym

Wow, I got quoted by a FPer, I can die happy now!

That flattening was one of the first things that jumped out at me. By nature when presented with charts or big tables I start looking for the stories it tells.

Very interesting stuff, thanks. Sounds like all of these groups are hard to crack and we may never get much below that 10% floor. 8% perhaps.

p.a.

David how does one code a snakebite caused by online i.d. efforts?

Mike J

How’s the foot?

Central Planning

Anecdotal, but my dad’s wife said one of her kids (with a family) decided to pay the penalty for not having insurance than paying the $900/month they would have to pay. I don’t know where they fall in relation to the FPL, but I do know they prefer to buy $9 gallons of organic milk. I think it’s a question of priorities.

Certainly, if they do have a catastrophic event they are royally screwed.

Another Scott

@p.a.: It’s probably in here. Let’s see…

W59.19 Other contact with nonvenomous snake

W59.19XA is a specific ICD-10-CM diagnosis code W59.19XA …… initial encounter

Maybe?

>;-p

Cheers,

Scott.

Sab

@Another Scott: I thought you were from Oh-ho-ho? Georgia? Really?Nothing wrong with Georgia, but I thought you were from Dayton.

Another Scott

@Sab: Moved around a lot as a kid. ;-) In Cobb County, GA and Dayton, OH (and other places) off and on.

Cheers,

Scott.

(Born in MI, lived on Long Island as an infant, also too.)

Matt McIrvin

@Ceci n est pas mon nym: It seems like the Medicaid gap (specifically, the fact that people in it are not eligible for exchange subsidies) is trivial to plug given a political environment in which it’s possible to pass anything at all. The only reason it still exists is that Congress refuses to make any fixes to the ACA so it will die. Of course that may just transform many of them into “woodworkers” who don’t get insured anyway, but at least they’d have the option and some would take it.

Most of the rest would be covered by any reasonable single-payer program, with the exception of the undocumented immigrants, who are probably uncoverable unless their status is regularized or a major (favorable) change occurs in the way people in the US think about immigration.

Ohio Mom

Does any developed nation have 100% coverage? I’m thinking that just about every place must some undocumented aliens, and odd groups that choose to stay on the fringes, such as cult-like groups, or maybe Roma? Cranks who live on the woods?

Obviously the US could do much, much better, if only we would all agree to spend a little more. I’m just wondering what an excellent percentage would be.

FlyingToaster

I can’t speak to the country as a whole, but I do know some anecdata from here in the Commonwealth (and my sibling in another state):

Roughly half of the uninsured population is religiously or philosophically opposed to health insurance. Boston is the home of the Mother Church of Christian Science; we have a significant number of people who won’t buy insurance because it won’t cover their “practicioners”. This overlaps with the Waldorf-School families; they won’t let their kids be vaccinated but they’ll drive out to Western Mass to buy organic or raw milk. This tends to include the libertarian gun nuts.

Another 4-5% are folks with dubious or no eligibility; if you’re working for cash because you don’t want any paperwork that can be discovered by, say, the police, you don’t have a permanent address due to addiction or mental health issues, or you’re undocumented, you won’t be getting insurance, because any paperwork involved is likely to be more of a threat than insurance can cover.

The last percent is singles in the gig market; I was in that boat in the ’90s, and dumped my insurance because it didn’t cover the shit I actually used, and wanted to charge me 4800/annum for the privilege of not covering me. My sibling is in that boat; self-employed, generally healthy for someone in their 50s, and the networks on the exchange in her backwater won’t cover her doctor for what she can realistically afford. She makes ‘way too much for subsidy, but the available Silver network is too effing narrow. I also know some younger folk (singles, tech contracting after age 26) who are in that boat as well.

I think the guesstimate that 92% coverage would functionally be full coverage is correct.

David Anderson

@FlyingToaster: Massachusetts in 2016 covers just north of 97% of its residents:

https://www.bostonglobe.com/metro/2016/09/17/rate-uninsured-mass-reaches-all-time-low/2adsq1tTALnZot6TVarC2L/story.html

The last 1% or 2% are the most difficult to enroll/cover unless there is presumptive eligibility when they show up at the hospital as de facto coverage. But getting to 96% or more coverage is eminently feasible on technical but not political grounds.

Brachiator

@Ohio Mom:

.Not necessarily. From the analysis and commentary here, some groups are very hard to reach, and current options may not work for them.

Also, I saw a news story suggesting that Trump wanted to cut ACA marketing and outreach by 90 percent. If this is true, it says that they current administration doesn’t even want to try to do better. Just vile and disgusting. They are willing to see people hurt just because Trump can’t get his way.

patrick II

David, if you are still around. I was talking to an owner of a local golf course yesterday. He said he had been a member of a group that had lobbied in person against the health insurance law because it was too expensive for his employees. I said Obamacare had brought costs down relatively, and he said he wasn’t talking about individual market, but the market for business groups and that prices have gone up (evidently enough to get him to go to DC).

Anyhow, if I owned a working man’s public (but nice) bare bones golf course with (estimate) maybe thirty or forty employees, am I suddenly paying significantly more for health insurance for my employees than I was a few years ago? This guy seemed very sure he was.

David Anderson

@patrick II: That really depends on a lot of details.

There is a decent chance that if the demographics of the group are young, male and healthier and proportionally fewer dependents that they are paying more as the small group market is no longer medically underwritten for the fully insured segment but is now community rated for the FI group.

That story passes my smell test.

patrick II

Thank you.

So the trade off is, he might have had a smaller but healthier group of golf course employees before, but now small business members are of a potentially larger, older group, so more expensive. However (if I remember pre-Obamacare correctly) if one of your small group of healthy people suddenly gets a very expensive disease, then your rates could go up quickly.

DLG

There are also asset restrictions on Medicaid that are very tight (e.g. value of a functional car or “in case of emergency” savings) in many states. I’ve seen numerous discussions of the income hole in opt-out states, but no mention of the asset qualification conditions.