Catastrophic coverage within the ACA framework are plans which are guaranteed issue, community rated plans that exist in parallel to the metal plans in the ACA individual market. Catastrophic coverage is not subsidized. People are eligible to buy Catastrophic if they are under 30 or if they receive a hardship exemption.

Catastrophic plans tend to have a significant pricing advantage over similar Bronze plans. Structurally, a Catastrophic plan is effectively a funny looking Bronze plan in its benefits and actuarial value. The premium differential is due to the combination of a much younger risk pool, a healthier risk pool as the very high deductible acts as a health sorting mechanism and a risk adjustment play.

the ACA there are two distinct risk adjustment pools. The catastrophic pool shifts money between catastrophic insurers. The money is mostly covering healthy and young people. The other risk adjustment pool is the Metal pool. Bronze, Silver, Gold and Platinum buyers are all shifting money amongst the plans. Typically Bronze plans will send a significant proportion of total premiums into the risk adjustment pool while Gold and Platinum plans will be net recipients of risk adjustment funds.

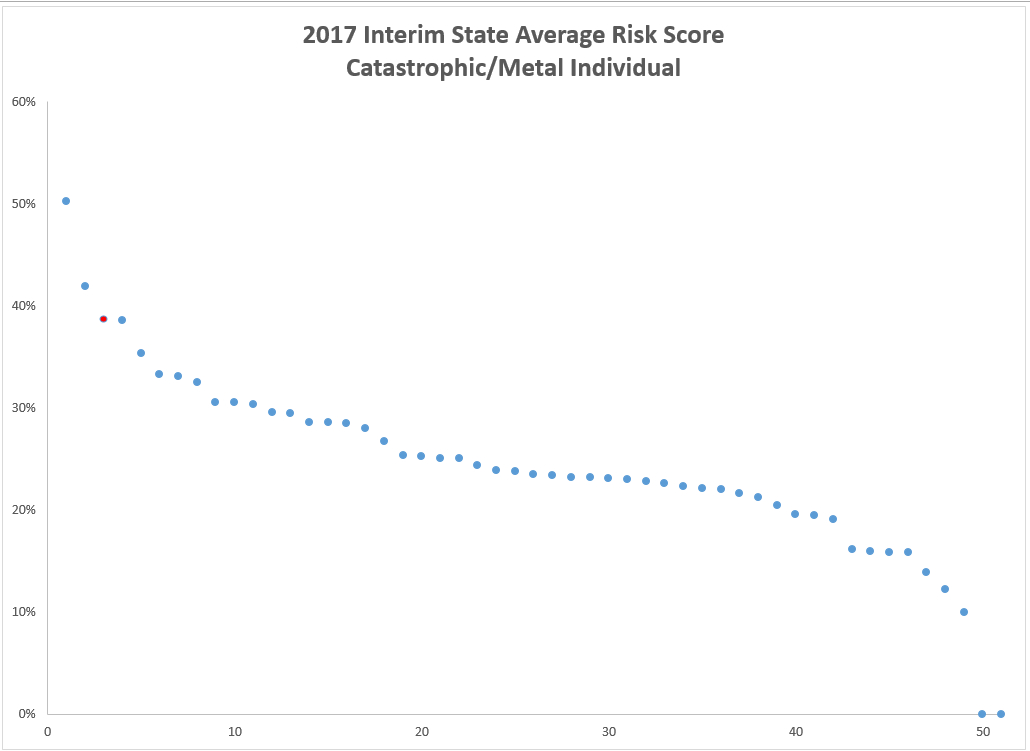

Using the same interim risk adjustment data as yesterday’s post, we can see the states’ ratios of risk scores for the catatastrophic market to the individual metal market.

The most important thing to note is that all state average risk scores for Catastrophic plans are significant below the average risk score of the metal plans. Since Catastrophic and Bronze plans are functionally similar, Catastrophic plans enjoy a significant risk adjustment pricing advantage as they don’t ship money out to cover some of the claims for Silver, Gold and Platinum buyers unlike Bronze premiums which cover all of their own claims and sends money into the risk adjustment pool.

Colorado’s legislature recently sent a bill to the governor’s desk that would fund an actuarial study to see if opening up Catastrophic plans to all ages would have a positive impact on premiums. And if the study found a positive impact, the bill would require a 1332 waiver to be submitted with the go-live date of January 1, 2020. Colorado’s catastrophic score is 38% of the metal score and it is highlighted in red.

(1) (a) THE COMMISSIONER SHALL CONDUCT AN ACTUARIAL ANALYSIS TO DETERMINE IF THE SALE OF CATASTROPHIC HEALTH PLANS TO PERSONS THIRTY YEARS OF AGE AND OLDER WHO DO NOT MEET A HARDSHIP REQUIREMENT WOULD RESULT IN A REDUCTION IN THE TOTAL AMOUNT OF ADVANCED PREMIUM TAX CREDITS RECEIVED BY COLORADO RESIDENTS OR WOULD INCREASE THE AVERAGE PREMIUMS OF INDIVIDUAL HEALTH PLANS IN COLORADO. IF THE ACTUARIAL ANALYSIS DEMONSTRATES THAT THE TOTAL AMOUNT OF ADVANCED PREMIUM TAX CREDITS RECEIVED BY COLORADO RESIDENTS WILL NOT DECLINE AND THE AVERAGE PREMIUMS OF INDIVIDUAL HEALTH PLANS IN COLORADO WILL NOT INCREASE, THEN THE COMMISSIONER SHALL APPLY TO THE SECRETARY FOR A FIVE-YEAR STATE INNOVATION WAIVER IN ACCORDANCE WITH SECTION 1332 OF THE FEDERAL ACT AND 45 CFR 155 TO WAIVE SECTION 1303

This is going to be a tough set of criteria to meet. Catastrophic plans should have a significant non-subsidized pricing advantage over Bronze plans. Bronze plans probably have a pricing advantage over Catastrophic plans for folks who receive advanced premium tax credits. This will be more notable as Colorado is switching from a Broad CSR load to Silver-loading their CSR costs in 2019. The target buyers for Catastrophic will be non-subsidized healthy buyers who are currently ineligible for Catastrophic due to age. They are currently buying minimal Bronze coverage.

If these current Bronze buyers shift to Catastrophic, they will increase the average risk score in the metal pool as they are some of the lower scored individuals in that pool. That will increase premiums for the metal buyers. It will increase the premium tax credits as the aggregate index rate for the metal pool will increase as well but it will make the remaining non-subsidized buyers worse off.

I am having a hard time seeing how an actuarial evaluation of this plan will come back with a recommendation to expand Catastrophic access given the policy constraints the Colorado legislature has placed on a potential 1332 waiver.

EMedPA

I wonder how many people buying these plans know how much they’d be on the hook for if they ever got sick or injured. My suspicion is that they have no idea.

Wag

Here in Colorado we have a divided legislature, with the Senate controlled by the GOP, while the House (and the Governor) are Dems. The House leadership has been very careful to safeguard important causes such as access to affordable healthcare This sounds like a good case in point. They have taken a major GOP talking point and diluted it with enough safeguards such that there should be little damage long term.

E

One of the challenges in comparing catastrophic to metal risk scores is the truncation of the catastrophic risk pool. With only people 30 and under, the risk adjustment model is going to score lower simply based on demographic scores alone.