The Affordable Care Act’s individual markets are predicated on choice as a means of discipline. Individuals are assumed to be able to sort through complex insurance contracts, networks and estimates of their likely future healthcare needs and choose optimal or near optimal plans. Individual choice, thus aggregated, is supposed to provide a very strong signal to the markets to provide more of a desirable set of characteristics and less of undesirable attributes. It assumes a high degree of rationality.

Yet at the same time, we know that humans do a decent job of faking being rational over a fairly limited choice environment. We are hopped up East African Plains apes whose brains are overclocked. We, as a social animal, have built up tremendously complex social structures to help us make mostly rational choices more often than not, but we are not particularly good at it. We have flaws that are known, predictable and exploitable. We are prone to inertia in choice. We are prone to not being able to effectively evaluate time varying and competing attributes well. We are prone to anchoring. We are prone to latching onto a shiny object. We are also prone to being overloaded.

Insurers in the ACA have very few rules that govern what they need or could offer on any county’s market. If an insurer is an on-exchange insurer, they must offer to everyone at least one silver plan. They also must offer in a rating area at least one gold plan but that offering does not need to apply to everyone in the rating area. Plans are bounded by fairly wide actuarial value bands. Beyond that, there are few restrictions. Insurers are supposed to offer plans that are “meaningfully different” but those differences are defined by regulation to be nearly meaningless. An insurer in a county can offer one plan (a silver)(Holmes County, Ohio 2019) or it can offer forty four plans in Rock County, Wisconsin in 2021.

When there are more insurers in a county, the county is more likely to have more plans on the choice menu.

The Eastern Aleutians in Alaska have 5 on-Exchange choices this year. There is a single insurer offering plans in this market which is offering a below benchmark Gold and dirt cheap Bronze plans but is not aggressively offering a discounted silver plan.

The other extreme is Seminole County,Florida (just northeast of Orlando). Ten insurers offer plans in this county. There are 174 subsidy eligible plans being offered on Healthcare.gov. The least expensive bronze plan is only modestly discounted relative to benchmark and the cheapest gold plan is well over benchmark.

174 plans is a lot of choice to sort through.

Research from the Medicare Advantage space found that choice quality went downhill fairly quickly when there were more than thirty choices on the choice menu. Medicare Advantage has a simpler choice environment as there is less variance in actuarial value while the out of network calculations are easier to make as Medicare has strong caps on OON charges unlike private insurance. The popuations are different but this is suggestive evidence that leads to a hypothesis that choice overload in the ACA marketplaces is plausible and could be significant in the quality of choice that people make.

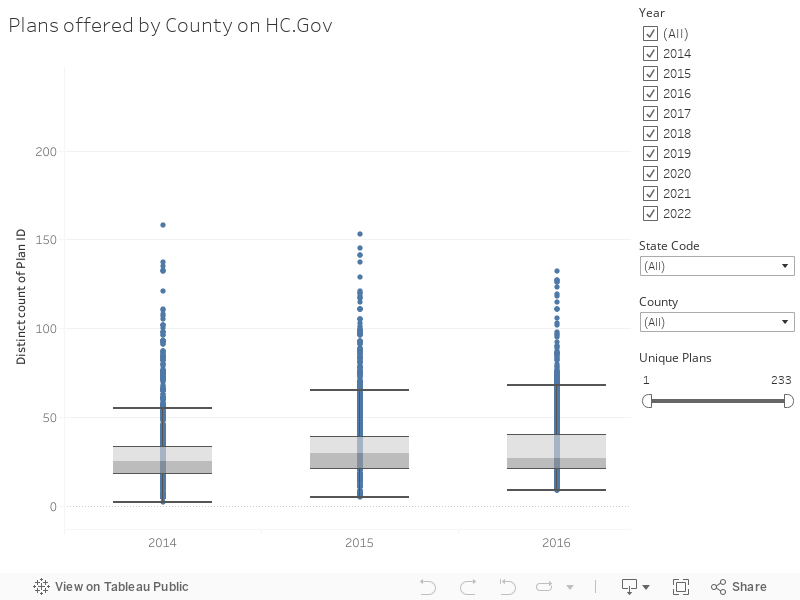

Below the fold is a Tableau on the number of plans per county over time.

WhatsMyNym

Here in WA, the state has started implementing their new Cascade Care program. I don’t know all the details, but we already have 2 new insurers in our county and many more options from all of the insurers. For me, it means I have the choice of a plan with a more open network and I can go back to seeing my old specialist. A lower deductible and max out-of-pocket, for a price slightly more than last year.