The ACA Open Enrollment Period (OEP) is going strong.

It ends on December 15th for Healthcare.gov states.

Insurers have few boundaries as to how they can design their plan offerings on Healthcare.gov. Plans can not exceed a fixed maximum out of pocket limit. Plans must fit into a metal band that is determined by an actuarial value calculator that the government issues every year. Some benefits can not have cost sharing attached to them. Some plan designs may qualify for enhanced tax benefits. Those are the legal and regulatory boundaries that constrain plan design. They aren’t much. Insurers have habits. Some insurers like deductible heavy designs. Other insurers love co-pays. Insurers just have to mix and match deductibles, coinsurance and co-pays to make the sums work.

A silver plan with zero deductible has meet de minimas actuarial value of 66% to 72% just like a silver plan that is only deductible. The actuarial value, which means the cost-sharing,

has to be made up somewhere else. Zero deductible plans that are coinsurance and co-pay heavy with higher maximum out of pocket limits are attractive to individuals who don’t think that they are going to be using a lot or any services. An individual in a zero deductible, 50% co-insurance plan who only uses a single urgent care visit is coming out ahead (assuming premiums are equal) than if they were in a deductible plan. For a given actuarial value, deductible heavy plans are likely to be more attractive to the highly likely to be expensive population while coinsurance and co-pay plans are likely to be more attractive to low users. Zero deductible can be a means to splitting and segmenting a population.

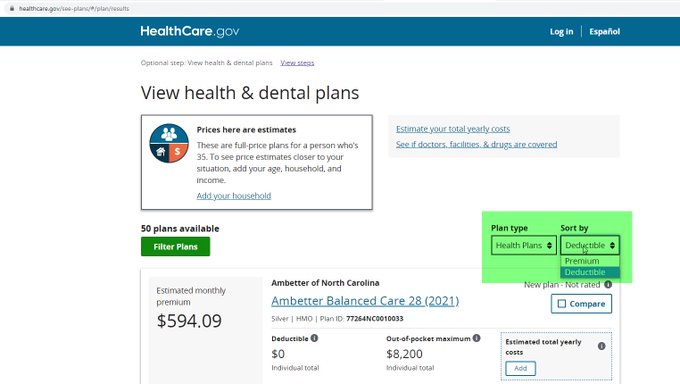

Healthcare.gov and many of the private broker websites allow for a search and sort based on deductible with the lowest deductible at the top of the search result list:

At some point, I have to wonder how much a zero deductible is market segmentation instead of a search engine optimization strategy? I would be shocked if SEO considerations are not at play for at least a few insurers.

Below the fold is the Tableau of all zero-deductible plan offerings by metal level on Healthcare.gov for 2021:

NotMax

Therein lies the tale. It’s a massive tournament of Dragon Poker.

Frank McCormick

Comparison shopping is all well and good. But when I had to choose my plan for 2019 in December of 2018, there were really only two Silver plans, one from Blue Cross/Blue Shield of Texas and a plan from a no name company.

Even at that, I received a release form from BCBS/TX later in the year (that I never signed) stating that their plan didn’t meet the requirements of Healthcare.gov.

daveNYC

There’s something fundamentally wrong that part of buying health insurance is trying to predict how much you’ll use it. I guess it’s great if you have some sort of serious chronic condition, but the whole point to any sort of insurance is to cover your ass in case something happens. Setting up a system where there’s an incentive to cheap out on coverage is going to lead to catastrophic situations for some percentage of the population.

BethanyAnne

That’s really good info, thanks. I’m trying to pick my plan this week, and a couple of zero deductible plans have looked pretty good. But I use a fair bit of healthcare, so they may not be my best option.