Charles Gaba at ACASignups has been digging into President Biden’s American Rescue Plan for ACA related items.

Depending on how you look at it, this is really three provisions:

- Temporary COBRA subsidies

- Killing the ACA’s APTC 400% FPL Subsidy Cliff

- Beefing up the ACA’s APTC Subsidy Formula below 400% FPL

The COBRA subsidies are important but would be temporary. The other two, however, would presumably be permanent, and are my main focus of course.

COBRA is a bridge based on the assumption that most people who are currently out of work are only temporarily out of work and reducing transition costs is a desired goal.

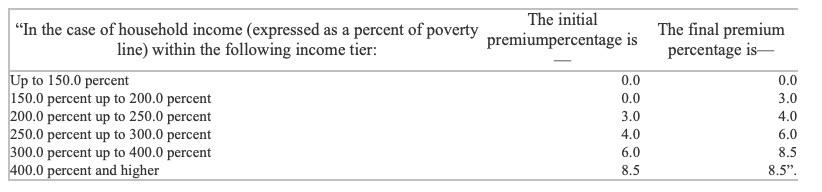

Charles did some digging with Rep. Underwood’s (D-IL) office for the proposed subsidy schedule:

Given this language, there is a strong chance that Medicaid Expansion will be rendered irrelevant in the states that have not yet expanded. But that is an aggressive interpretation of what “UP TO” means.

I want to focus on the 0% applicable percentage for people who earn up to 150% Federal Poverty Level (FPL) means. This is a big change. It means that the benchmark plan, currently a silver plan with a 94% actuarial value, would have a monthly premium of $0. Currently a single individual earning $18,500 pays $59 per month for the benchmark silver plan. This is a reduction in premium of over $700 per year. Notably, this $700 a year reduction in premium also applies to any plans priced above the benchmark. Someone who earns 200% FPL would see their benchmark premium be cut by more than half (6.49% income now to 3% income proposed)

Zero premium plans are quite valuable in that they reduce administrative friction. I’m part of a research team that has looked at plan effectuation and duration effects in Colorado. We found that zero premium plans significantly increased enrollment duration. Adrianna Macintyre and her co-authors at Harvard found that switching people to zero premium plans instead of nominal premium plans led to significant retention of enrollment. Administrative costs are significant in the ACA and other individual insurance markets. Furthermore, zero premium benchmark plans for people who earn under 150% FPL and highly likely zero premium below benchmark CSR silver plans for people earning up to 200% FPL should significantly decrease the probability individuals choose significantly inferior plans that have massive cost sharing but slightly lower premiums.

I’m still scratching my head about the competitive dynamics.

Right now, there is a clean divide in plan choice at 200% FPL. Below that, silver plans are overwhelmingly chosen as they have high CSR and fairly low cost sharing. Above 200% FPL, people get away from silver and towards either gold which is priced near silver and has better cost sharing than baseline silver, or dirt cheap bronze premiums with big cost-sharing. The dominant strategy for an insurer that has a comparatively cheap silver offering is to “compress the spread” where they offer a dirt cheap silver and then a second silver plan to grab the benchmark. This makes every other insurer be comparatively more expensive to cost sensitive buyers. If there is a $30 spread between the benchmark and the first plan offered by a different insurer, that is a big gap when the benchmark premium is $60/month. $90 could be a lot of money for someone earning $18,000. However under the proposed subsidy scheme, that plan would now by only $30/month which is less than the benchmark the person is facing. I’m also stuck trying to figure out what would happen to the strategy of the plan offered below the benchmark. There is little upside to an insurer to offer a very wide gap. This may decrease deductibles for that plan.

I’m still trying to think through the incentives of pricing for the above 200% FPL segments. I’m not sure what the strategy would be there.

This is a complex system. Simpler systems would be better if that is on the choice menu. I think that the proposed subsidy scheme would be a significant simplification as there are far fewer weird income thresholds and inflection points as well as a massive reduction in administrative burden and friction for millions of more people. This system would be quite advantageous to the people of West Virginia where the current average net of subsidy premium level is among the highest in the country as the state has broadloaded. It would also lead to significant financial support of rural hospitals as more people would be covered by insurance that pays above Medicare rates as their net, personal premiums would be lower.

Mike S (Now with a Democratic Congressperson!)

Thanks. I hope we can someday get past this “MORE CHOICES=GOOD” mindset. In health insurance (ACA and Medicare choices especially) and other Government things it is a nightmare of little things that add up to indecision that is planned by marketing experts.

David Anderson

@Mike S (Now with a Democratic Congressperson!): AMEN

Buckeye

So I have a friend who’s become more lefty/socialists. He’s gained a lot of friends who of the socialists/Rose Twitter/Jacobin variety.

And yesterday one of his friends posted this:

“He’s so RIGHT!! Biden has already backtracked on healthcare. He’s going to be gaslighting people that subsidizing COBRA will save people. That’s disgusting. That’s more $$ for insurance.

And the other day he sent troops into Syria.

2022 is going to be worse than 2010!!! What a joke. So sad.”

He didn’t post any links, so I went looking, and found out that the COBRA is part of the pandemic package and not his healthcare proposal (and the Syria bit was BS too).

He responded: “even a temporary subsidy of COBRA is assisting for profit insurers. Joe Biden does NOT have a good track record for helping poor/middle class. ”

So how does one deal with misinfo coming from the lefty side?

taumaturgo

@Buckeye:

Miss Bianca

Going to have to read your paper, David, as I’m one of those “zero premium” babies here in CO. One of the dubious joys of being poor in Paradise…

Chyron HR

@taumaturgo:

“But we’re posting right-wing propaganda from the LEEEEEEEEEEEEEEEFT.” – Mating ball of the Berniebro