Valued reader and friend of the blog, KithKanan passed along an interesting product offering from Anthem for the Colorado small business market. Below is the core pitch of the product for brokers who are trying to sell to small (2-100 covered lives) business groups.

What does all of that mean?

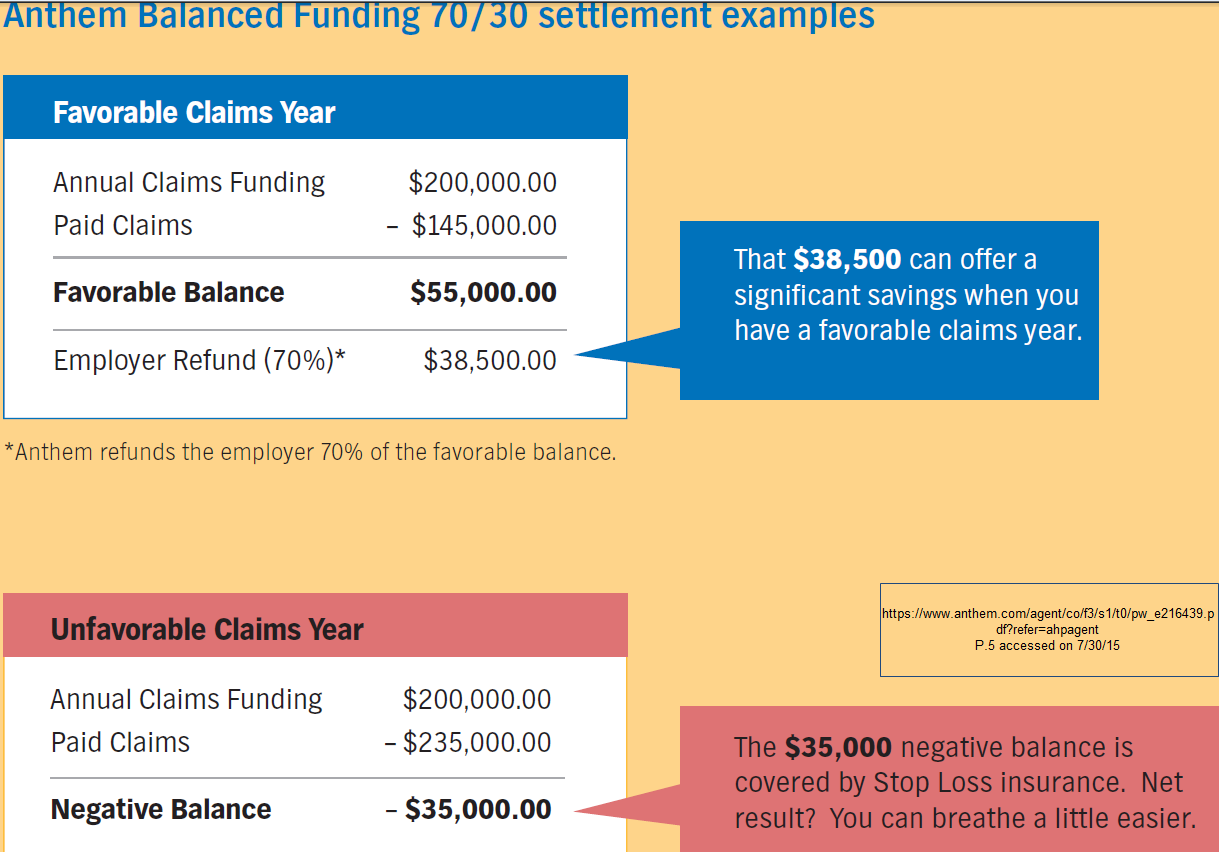

Mechanically, the Anthem plan is being pitched as a hybrid. The insurance company will take on the risk of very high claims through the issurance of a stop loss policy, while the insurer and the company split the difference between projected premiums and actual medical expenses if the medical expenses come in low. This is very different and unusual. It is a pitch to companies that are disproportionally young, healthy and male to avoid PPACA regulations on underwriting.

Last July, I wrote about a possible work-around for some small business groups to avoid community rated small business underwriting:

The change in underwriting assumptions for the small group market only applies to companies that are “fully insured.” Fully insured is a term of art. It means the insurance company collects a premium and takes on all of the risk of claim expenses being higher than projected. If a group of three people have two of the three covered lives go to the trauma center in a benefit year, the insurance company eats a massive loss on the group. That loss should be covered by the thousands of other covered lives in other small groups. If that same group has a total of seven claims for the entire year totalling $800 and that $800 is entirely deductible dollars, the company will have given the insurance company a massive check for peace of mind only. There would be no refund.

There is a loophole for companies that think they want to take on additional risk to reduce their premiums.

The alternative system is to buy an administrative services only (ASO) contract with an insurance company. An ASO arrangement has the insurance company handle the back-end work (pay claims, print ID cards, create provider networks etc) for a fixed fee every month. However, the insurance company does not provide any insurance. The group takes on the risk of paying all the claims.

ASO arrangements are super-common with large groups (more than 500 covered lives) as those groups have enough numbers for statistical smoothing to come into play. Medium size groups (50 to 499 covered lives) can do ASO but outliers are more common. Small group ASOs are offered but they are niche products.

That may be changing for some small companies. I know one regional company is considering offering a small group ASO for at least five covered lives. That is a miniscule risk pool. The target market is for young, healthy and overwhelmingly male companies to opt out of community rating by going to a self-insured model….ASO plus stop-loss is effectively a company wide massive deductible plan. ASO works really nicely when claims for a population are below expectations. It runs into trouble when trouble happens. Big companies use their big risk pools to cover trouble. Small companies have to reinsure…

My worry in 2014 was that a small group would go the ASO route with reinsurance that did not kick in until $50,000 worth of claims were submitted for one person (ie a cancer diagnosis). The small group would have to pay the $50,000 for Person 1 as well as the routine claims for the other eight employees. My worry would be that an ASO small group would not have the cash on hand to actually pay a big claim that would trigger stop loss. The Anthem plan design of integrating stop loss into the base premium precludes that risk while giving the small groups some of the upside of of low claims expenses that typically fully accrue to the ASO sponsor.

From a policy perspective, this is a positive selection play for the small group market. It is designed to cherry pick young, healthy groups and give them good rates. Small groups on the fully insured small group market will be be some combination of sicker, more female, and slightly older. That means fully insured groups will be charged more as the claims cost will be higher than it otherwise would have been. I expect to see more plan designs like the Anthem design to proliferate for cherry picking purposes.

inkadu

And it adds another layer of emotional noise to the employees medical problems. Its one thing to raise the rates of a small company one year; quite another to have them directly paying your medical bills (which also might raise some privacy concerns — how is the money routed to providers?).

MomSense

Couldn’t this lead small companies to change their hiring practices (even moreso) to cherry pick employees that are less expensive to insure? Part of why I appreciate that base coverage includes contraception, pre-natal care, etc. is because there are benefits to society when women are able to plan when to have children and to deliver healthy babies.

Richard Mayhew

@inkadu: That happens to large companies all the time that have always been in ASO arrangements. Big Evil MegaCorp has always seen all of its employees’ claims data as they write the check; actually they can request from the insurance company all of the claims data as the insurance company writes the check and then bills BEMC for the claims for a month.

@MomSense: Yep, this is definately an incentive to cherry pick on hiring/firing.

NonyNony

@MomSense:

I suspect so. Give people a system and they will try to find a way to game it to their advantage.

(Chalk it up as yet another reason that we should have minimum coverage provided to everyone without having to have an employer involved at all except as part of the tax base to pay for it. Employers shouldn’t have to be even weighing the fact that some potential hire is the best software engineer they could hire, but that she’s also a smoker and might cost the company more in health care payouts than another candidate).

Aimai

My husbands company has for years put us in a high deductible plan and then covered the deductible somehow with an hsa or something. Nothing is covered for the first 6000 but i think the costs of stuff above that for someone with cancer etc.. Are good. So we pay a lot out of picket but its reumbursed.

Redshift

OT: Rick Perlstein knocks it out of the park on the uselessness of the coverage of the GOP primary.

Mnemosyne

@Richard Mayhew:

That depends on the state. Here in California, the Giant Evil Corporation I work for is self-insured. They receive the bills to pay, but they do NOT receive identifying information about the employee because state law forbids that. So if I were (for example) getting cancer treatment, they would know that a 46-year-old nonsmoking woman in the Studio division was receiving treatment, but everything else would be confidential.

If it was a small company that was self-insured, there probably would be a way for them to (illegally) figure out who I was, but since it’s a company with 50,000+ employees in the US alone, I feel reasonably secure that they wouldn’t be able to discriminate against me.

Redshift

OT: Rick Perlstein knocks it out of the park on the reality of the GOP primary and the uselessness of the media coverage.

Lee

This is somewhat on a tangent to this topic and I’ve been wanting to get this off my chest.

Here at work we think someone was terminated because of the cost of their healthcare. The former employee was completely average in all other ways and great to work with. His pay grade was probably even on the low side. His manager was told by upper management to grade his evaluation a certain way that was not correct (I know the manager personally so I know this is true).

Both him and his wife have a myriad of health issues. The company I work for is usually very good to work for so this is a somewhat troubling turn of events if true.

Another aspect of the termination might just be that the CEO has stated he wants to lower our average age and time employed. The ex-employee was both older & with the company for quite awhile. The average length of employment here was 14 years as of a couple of years ago.

bluefoot

@MomSense: I’ve certainly seen this both in hiring and in layoffs. Especially layoffs. One company I worked at, it was pretty obvious that one of populations laid off were people who had had largish claims. Not necessarily missed work, mind you, but (for example) a torn ACL from a weekend basketball game, chronic autoimmune disease, etc.

gene108

We’ve been in a hybrid plan for the last 6 years.

We had a couple of catastrophic claims, when we were fully insured, which doubled our premiums and this hybrid space is what we could afford. The carriers medically underwrite the plan, so they have more confidence in setting up their risk corridors. This does not always work out, but they have more data to go on than a fully insured competitor.

Even in our group, which is no longer young and healthy, this space is manageable to occasionally get a good year in claims and manageable premiums.

gene108

@inkadu:

My experience in this set-up is you get claims data aggregated by procedure / diagnosis. It is not employee A had this type of surgery.

You will see a line item for maternity care, for example, or a line item for people being treated for hypertension.

Unless you know what your employees are up to, you do not know, who has had what procedure or has what diagnosis.

Also, insurance companies track your medical history and to determine what’s wrong with you and what type of risk you may pose. They do a pretty good job diagnosing people based on prescriptions issued, doctors visits submitted (i.e. with specialists), and procedures the doctor has you tested for.

It’s weird when you go into renewal and the insurance company basically says you have a couple of heart attacks waiting to happen, so we are raising your rates, and you wonder how they pieced this stuff together.

JGabriel

Richard Mayhew @ Top:

Perhaps a tax or penalty on plans with a skewed male to female ratio would be a good idea to keep this sort of system-gaming in check. I’m not sure anything can or should be done with respect to plans/groups that skew young though – except to ensure that they meet the standards set for exchange plans. Younger employees tend to get screwed enough as it is.

gene108

@JGabriel:

How many of the males are young and married? If the spouse is on the insurance he is not advantageous versus a slightly older male.

Why?

Young married couples tend to pump out babies and maternity care adds up.

You can have a mostly male plan, but if a lot of spouses / families are enrolled you are not coming out ahead in the demographic game.

So the incentive is to make any non-employee benefits prohibitively expensive for dependents.

chris9059

Doesn’t this type of plan encourage employment discrimination against women and older workers?

If I am an employer with this type of plan I have a very clear financial incentive not to hire qualified women and older workers simply to save on premiums.

JGabriel

gene108:

Gene, did you even read the article above? I mean, we can specify single males, if you like, but the point was that these plans are cherry-picking low cost demographic groups to increase costs for people who, you know, actually need the help.

Well, in addition to the above mentioned cherry-picking, an employer whose workforce skews, say, 85% male, is clearly not making an effort to create equal opportunities for women, and is probably making an effort to exclude them. I don’t see why we should be rewarding a company for such behavior with cheaper health plans.

JGabriel

@chris9059:

Yes, exactly.

Richard Mayhew

@chris9059: Yep, but the more basic is it discriminates against anyone who looks sick. If I am hiring for a position which is 90% + computer work and the remaining 10% is going to meetings, and I have this type of plan in place, my incentive structure is to find a reason not to hire the candidate who walks in with a cane, especially if they are young.

One of my neighbors is a younger guy who has MS, he uses a cane a couple of times a month. The last few times he has had to interview for positions, he leaves the cane in the car.

Fred Fnord

Not that this is anything new. There was a nice article 5 or so years ago about a woman who was (unusually honestly) taken into the boss’s office the year after she developed a major health problem and told, ‘Well, our insurance has told us that they will put a $1M surcharge on our policy [in a company of ~10 people] for next year, and hinted that if we got rid of a certain employee it would magically go away. And nobody else will insure us at all. So I either have to let go of you or discontinue health insurance for all my employees.’

This is the days before Obamacare, so most of them would not have been eligible to get insurance at all. The article pointed out that this was illegal in California but essentially said there was no way to actually enforce the law as long as insurance companies maintained a tissue-thin layer of deniability.

As I always said, the real measure of the ACA will come when the insurance companies figure out how to route around it. We certainly won’t see any fixes on the Federal level, and most states won’t either.

Richard Mayhew

@JGabriel: Depends on the sector — the B-level minor league soccer team 2 hours from my house has an 80% male workforce (of the non-playing workforce, the male/female split is 5-4)

The knitting store/collective/co-op/vast money pit that my wife frequents employs an 80% female workforce. The lingerie shop that has the bras my wife prefers has a 100% female staff. The 12 person tree removal service that a neighbor works for has 11 guys for strong back/weak mind type of work.

At the small business level which is what this plan is being pitched at, there are really good reasons for skewed gender balances. I don’t think skewed gender ratios per se at very small firms are a pressing policy problem unless there is strong corrobarting evidence of discrimination.

Brachiator

@Richard Mayhew: I wondered if you had seen or had any comments to the news that in California, the health care rates are projected to rise by only 4 percent?

http://www.latimes.com/business/healthcare/la-fi-obamacare-rates-20150727-story.html#page=1

gvg

Companies tend to prefer healthy anyway. When someone is sick, other employees have to pick up the slack, often without extra pay. This may cause resentment and a tendency to get rid of the sick employees. It depends on how smart at imagining their own turn at poor health the management and fellow workers are plus the personality of the sick person and the non sick employees interactions. Also the actual business makes a difference. some types of business or jobs make it more of a problem when someone misses a lot of work than others.

I used to see a lot of financial aid college petitions about family financial circumstances. There was an observed pattern. One year a family was petitioning because of much higher than average family medical costs. The next year they were petitioning for parent loss of income due to being let go.

Quite a few years ago their was a woman who got a brain tumor cancer. Prospects were pretty much certain death soon. She did not face that and was in denial. She had not worked there long-about a year I think. The management called the rest of us together and explained it and said we would all have to cover some of her work without pay, that we couldn’t hire someone else without letting her go which they weren’t going to do, and that the employee did not recognize the situation so we would have to act like she was going to get better and check her work in case she made mistakes. She was making mistakes too, lots of pain and lots of meds made her skills go way down. they had looked up our insurance rules and the Directors told us that if she worked one half hour per 2 week pay period, her medical insurance would keep coverage so she had to keep dragging herself in. In addition certain self chosen employees were going by her house checking on her and making sure she had groceries. It was a lot of extra work for all of us and it clearly would have been easier to let her go. She was making mistakes but we didn’t even tell her. I have remembered that when considering job searches in the years since. The management has its flaws…they are too cheap about raises in ways I don’t think the higher levels care about but 2 years ago I had cancer after years of no problems. I had no employment or insurance problems at all. That is not a typical work experience. This was after watching the ACA fight finally get passed and all through my illness I was thinking other people still don’t have this. The Docs offices and the hospital have specialists that help guide people in getting special medical grants and cheaper meds….they asked if I needed their help but I didn’t. I was able to write $40 copay checks and 1 $100 surgery fee…it didn’t even add up to make it nessesary to itemize deductions that year (about $100 short of that). The bosses make a big difference. This is a huge University. Other departments under the same insurance are run differently from what I hear, but it matters. In a smaller department, it might have been impossible to carry a situation like that though. A small company with maybe 5 employees will have a real problem surviving if 1/5 their workforce is not really working. This also affects the armed force reserves called to active duty. Employers are supposed to save their jobs for them.

pseudonymous in nc

@chris9059:

Or people with chronic conditions that can be managed without affecting performance but incur relatively high recurring costs. Type 1 diabetics are an obvious cohort here. Feels like an ADA claim waiting to happen, and I’d be very happy if it did to shut down cherry-picking plans.