I contend that monopolistic insurers in the ACA market are able to shape their risk pool. They have multiple means to implement a strategy. They can use networks. They can use benefit design. They can use formularies.

In Mississippi, you cannot play a lot of the games that can be played with a healthy pool in other places. Is a narrow network going to eliminate your town’s only hospital? Are people really driving to Children’s Hospital if they do not live near it or have a child with cancer or some other major issue that can only be addressed there?

Really good comment, and I want to highlight one strategy an insurer can use. They can play spread games. I will make the simplifying assumption that actuarial value correlates to premium level and we’re using a single unified actuarial value scale instead of metal specific scales. I am also assuming a single network and the same plan type for all plans (it could be an EPO, HMO or a PPO, does not matter). I am isolating on plan designs.

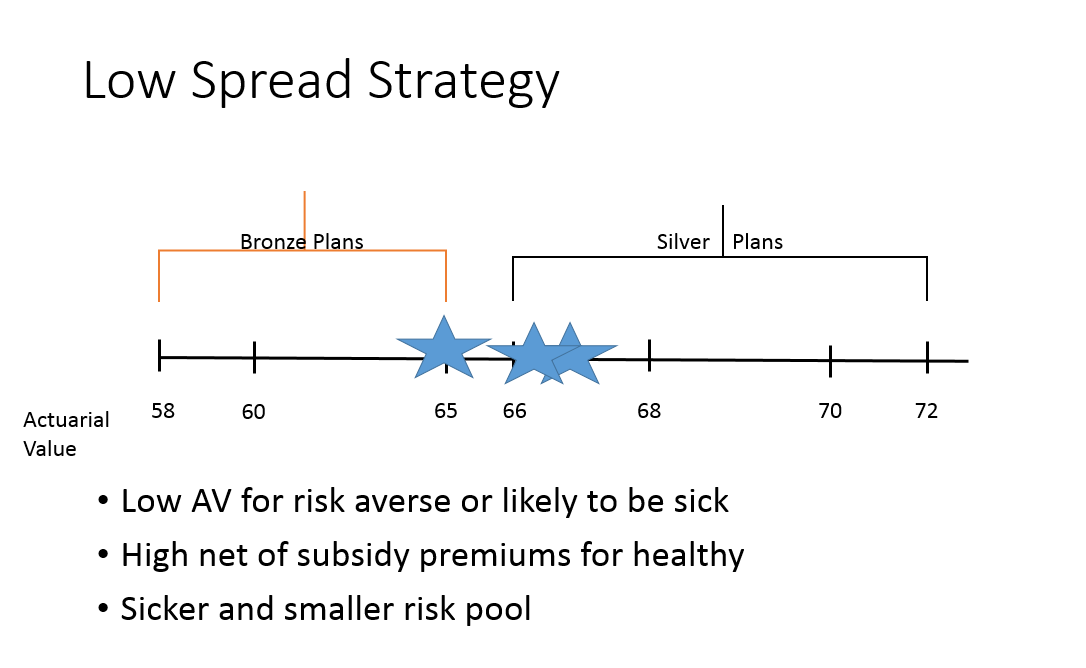

The first strategy is a low AV and low spread strategy.

Here the benchmark Silver Plan is near the bottom of the allowable actuarial value range for Silver plans. The cheapest Silver is barely below the benchmark while the insurer is only offering a single Bronze plan. Since we are looking at a monopolistic insurer, there is no competetive pressure that dictates these choices. These choices result in high out of pocket costs for everyone, and since subsidized premiums are predicated on premium spreads, the lowest actuarial value plans won’t be too much cheaper than the benchmark. The healthy and risk embracing won’t see too many good deals.

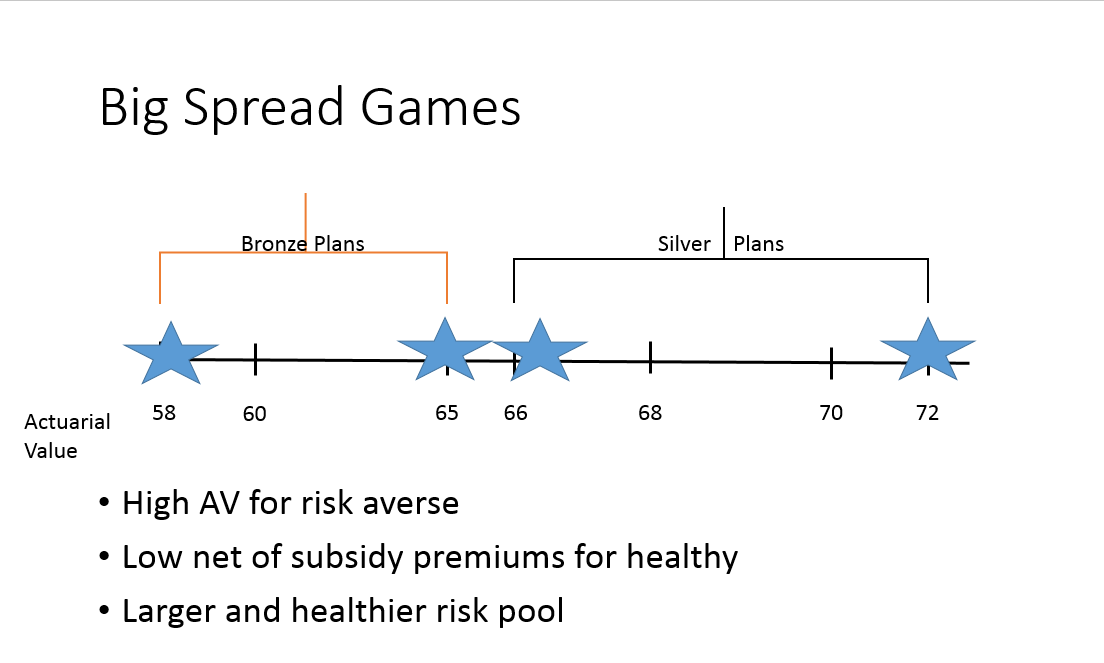

The other strategy stretches everything out.

Here, the benchmark Silver is near the top of the allowable range. The cheapest Silver is near the bottom of the allowable range. There is a big spread here which means the Silver Gap is large. More importantly, the carrier is offering two Bronze plans. One is still near the top of the Bronze range. The other is near the bottom of the Bronze range. This means that there is a huge actuarial value gap between the cheapest plan offered and the benchmark. Consequently, the healthiest and most risk taking folks will see very low to no dollar premiums if they qualify for subsidies.

It does not matter if the insurers are Silver Loading or Broad Loading their CSR response. It does not matter if they are offering an HMO or a PPO. It does not matter if they are in a high cost state or a low cost state. A single insurer state can strategically choose the premium spreads between the benchmark and least expensive Silver and non-Silver plans.

Wyoming has chosen a big spread strategy. Mississippi has chosen a small spread strategy. These are deliberate choices.

| State | County | Metal Level | Maximum Benchmark Spread |

|---|---|---|---|

| MS | Neshoba | Bronze | ($60.00) |

| MS | Neshoba | Silver | ($59.00) |

| MS | Neshoba | Gold | $93.00 |

| WY | Laramie | Expanded Bronze | ($265.00) |

| WY | Laramie | Bronze | ($236.00) |

| WY | Laramie | Gold | ($136.00) |

| WY | Laramie | Silver | ($6.00) |

On the Road and In Your Backyard

On the Road and In Your Backyard

currants

Had to read this through twice (had I read carefully the first time, once might have done it!) and think about the chart to understand the “Meth Laboratories of Democracy” tag. I’d hate to assume the worst, but … yeah, probably should.

Mike S (Now with a Democratic Congressperson!)

I like the graphics showing these spread strategies very much. Thanks!

StringOnAStick

Can we discuss why this different strategy for each state is intentional? I know that Wyoming has a much smaller population and that MS is both larger and as I recall tends to be in the lowest group as far as ratings of general health markers goes. Does the Wyoming spreads have to do with how low density the population is or that as an oil and gas based economy it tends to have lots of job churn?

David Anderson

@StringOnAStick: It is an insurer’s choice. I think the Mississippi strategy is leaving a lot of money and a lot of covered lives on the table. I can’t suss out intent here.

Another Scott

@David Anderson: Maybe this story from the Atlantic has some clues? (Sarah Varney from 2014):

Given all that, it’s not surprising to me that Mississippi insurance companies don’t want to make the plans appealing – the political establishment wanted to minimize the number of people covered.

FWIW.

Cheers,

Scott.

David Anderson

@Another Scott: If Wyoming was a flaming blue state, or even a purplish state, I could buy the partisan composition argument. But it is not. Other deep red states like Wyoming, Nebraska, Alabama and South Carolina have had single insurer state wide monopolies with different strategies.

Something is funky in Mississippi.