In the spring of 2017, the Center for Medicare and Medicaid Services (CMS) announced new rules that broadened the allowable de-minimis variation in actuarial value. Silver, Gold and Platinum plans were allowed to be up to four points under the nominal target instead of the previous two point cushion. They were still restricted to being two points above the target. Bronze plans were allowed to bounce from two points underneath the nominal target of 60% actuarial value. Bronze plans were allowed to go over the nominal target by five points.

| Old Rules | Current Rules | ||||

| Target AV | Low | High | Low | High | |

| Platinum | 90 | 88 | 92 | 86 | 92 |

| Gold | 80 | 78 | 82 | 76 | 82 |

| Silver | 70 | 68 | 72 | 66 | 72 |

| Bronze | 60 | 58 | 62 | 58 | 65 |

The goal was to provide more flexibility and to allow for slightly less expensive off-exchange premiums and perhaps slightly lower federal subsidies if the acturial value of the second least expensive Silver plan went below the previous 68% AV floor.

I was playing around with the 2019 CMS Actuarial Value calculator to determine how much $100 changes in deductible buys in actuarial value. That is a post for a different day. While I was doing that, I noticed something very interesting in plan design.

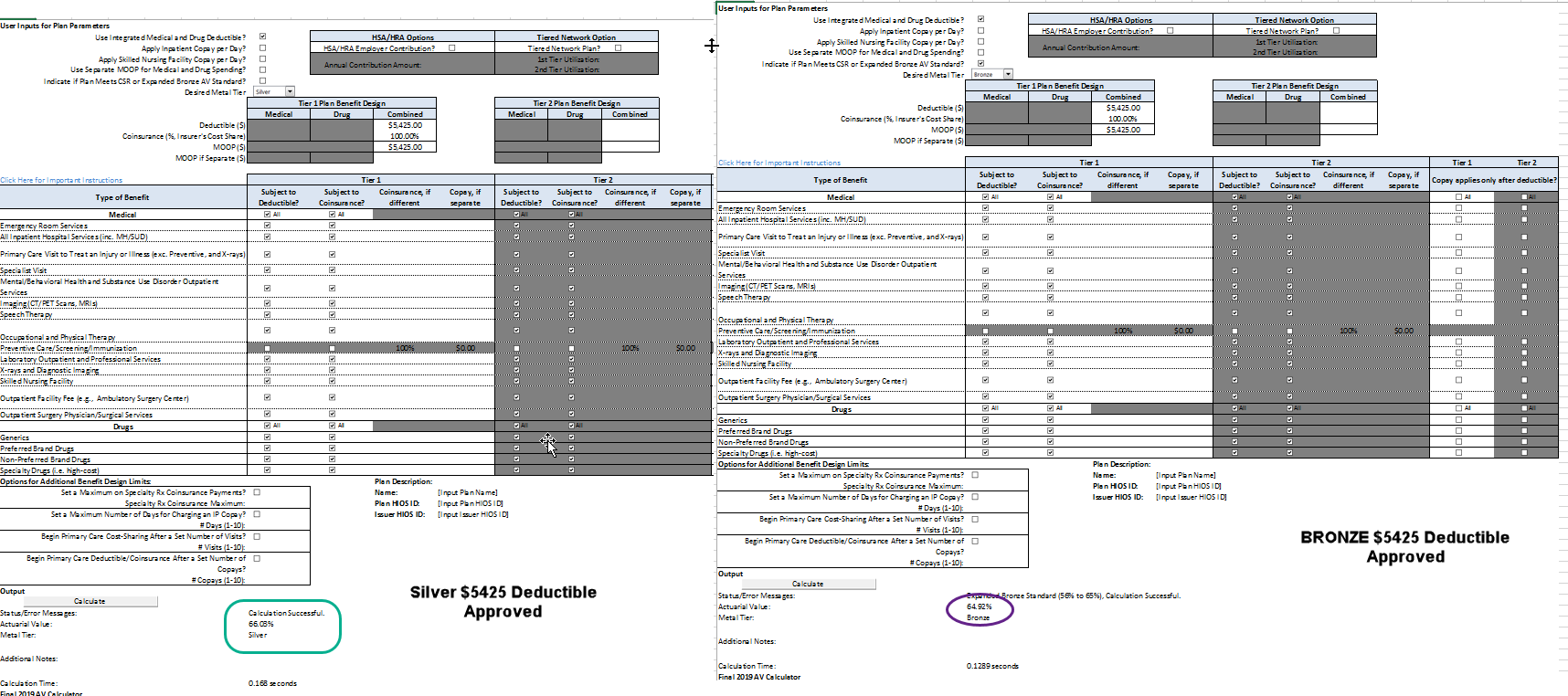

If you take a bare bones plan with a $5,425 deductible where everything besides the required preventative care services are deductible eligible, that plan can be both a Silver plan and a Bronze plan. There is a good mechanical reason for this mirroring.

CMS’s actuarial value calculator draws on different cost distributions for each metal plan. The actuaries assume that individuals with identical health profiles will use more services in a higher actuarial value band than in a lower band. This is “induced demand.” The model uses a step function for induced demand as a plan at the low end of the band is assumed to have the same induced demand as a plan at the high end of a band. So when a plan is right on the edge, it can draw against two different cost profiles to produce two slightly different actuarial value calculations. And in this corner case, the same plan design can qualify as two different metals.

This is interesting. There is nothing nefarious about a weird little corner case based on a step function and two different data pulls. But it offers up interesting strategic choices to call a plan that prices the same as either a Silver plan or a Bronze plan. Let’s assume that plans price in direct relationship to the actual underlying actuarial value with a continuous induced demand function once we hold network and plan type constant for a single insurer. This plan would then price the same for a Silver or a Bronze designation.

So what would an insurer do? I’m speculating wildly now.