Justice Anthony Kennedy is retiring effective July 31, 2018.

— SCOTUSblog (@SCOTUSblog) June 27, 2018

Open thread

![]()

Come for the politics, stay for the snark.

I am a student in the doctoral program at the Duke University Department of Population Health Sciences. I am working towards my my doctorate in Health Services Research with a policy focus. I am fundamentally fascinated by insurance markets, consumer choice and the navigation of complex choice environments. I'm currently RA-ing at the Duke Margolis Center for Health Policy.

I used to be Richard Mayhew, a mid-level bureaucrat at UPMC Health Plan. I started writing here and have not found a reason to stop.

Conflicts of interest: Previously employed at UPMC Health Plan until 12/31/16. I also worked full time as a research associate at the Duke University Margolis Center for Health Policy. I have received direct funding from the National Institute for Healthcare Management, and I have been on projects funded by the Rockefeller Foundation, Kate B. Reynolds Charitable Trust, Gordan and Betty Moore Foundation, Duke University Health System, CMMI, and various value based payment consortiums. I serve as a consultant on a grant from the Commonwealth Fund and have acted as a consultant to several ACA insurers.

Research Production is here: https://scholar.google.com/citations?user=zof9b4IAAAAJ&hl=en

David Anderson has been a Balloon Juice writer since 2013.

Justice Anthony Kennedy is retiring effective July 31, 2018.

— SCOTUSblog (@SCOTUSblog) June 27, 2018

Open thread

High actuarial value is better, right?

Well it depends.

It really depends on what you assess your prospective personal health risk to be and how much of a hit you can absorb. And from there, it is a matter of interrogating the benefit design of plans.

Let’s look at two Gold plans I designed using the 2019 actuarial value calculator to tease this out a bit.

| Plan A | Plan B | |

| Deductible | $500 | $2,000 |

| Coinsurance after deductible (you pay) | 30% | 0% |

| Maximum Out of Pocket | $6,000 | $2,000 |

| PCP Sick Visit | No cost sharing | Deductible applies |

| Generic Drugs | No cost sharing | Deductible applies |

What plan is more attractive if we assume same insurer with the same network?

What plan has the higher actuarial value?

Which plan is better?

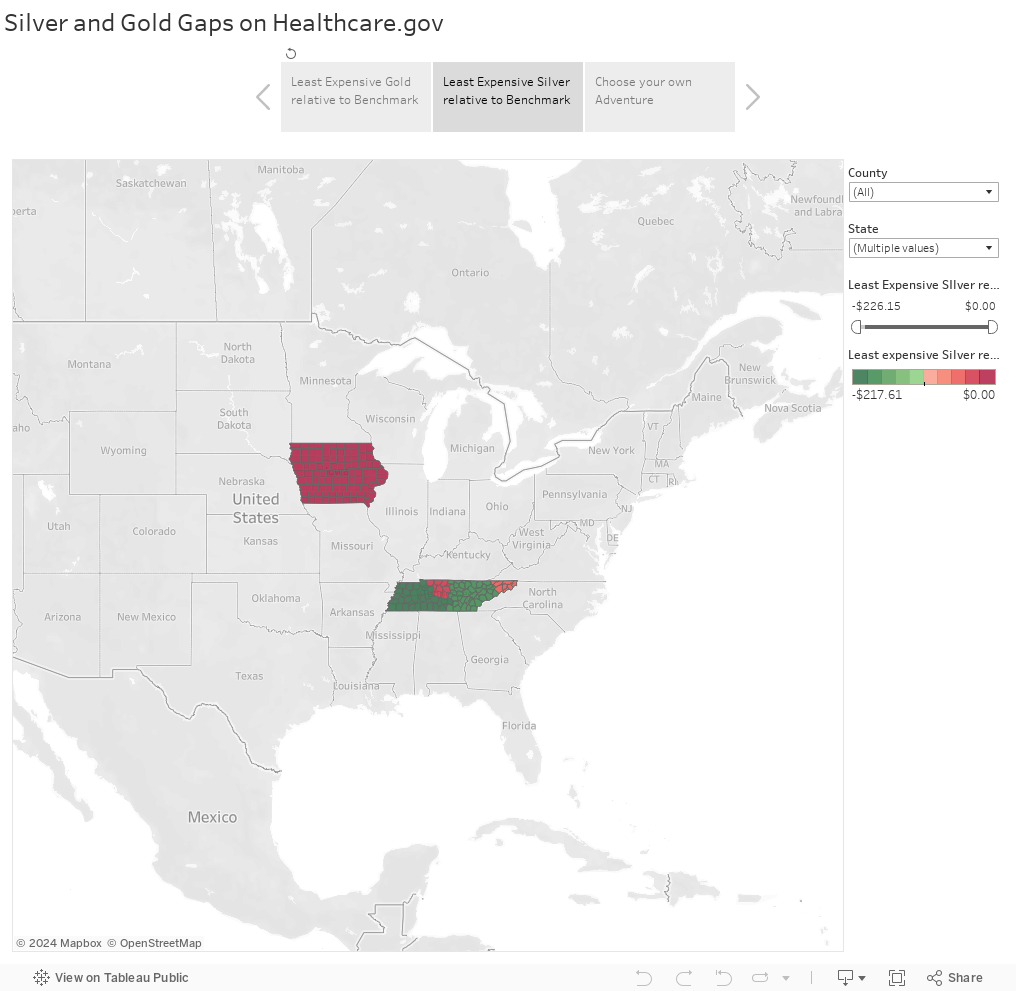

Iowa and Tennessee are, in some ways, very similar states regarding the ACA. They are both mostly rural and their political elite has worked hard to create numerous “outs” for healthier and prospectively low risk individuals from the ACA. They both have very high premiums and comparatively high risk scores.

Yet, in 2018, they were very different. Tennessee had some multi-insurer regions (Nashville and Memphis) while the local Blue Cross affiliate offered plans in most of the state. BCBS-TN aggressively Silver Gapped with some of the biggest premium spreads in the entire country between the least expensive Silver and the Benchmark Silver.

Iowa had a single insurer for the entire state. Wellmark, their BCBS affiliate, exited the market. Medica offered a single Silver plan for every county so there was no cost advantage to buying a less expensive Silver plan.

In 2019, Wellmark is re-entering Iowa’s market. Several insurers are expanding in Tennessee so Nashville, Memphis and Knoxville, and the northeast Tri-city region will have multiple insurers. This will lead to significantly different on the ground realities for subsidized buyers.

Non-subsidized buyers will directly benefit from increased competition. They can elect to stay in their current plans or see if there is a better deal elsewhere.

Subsidized buyers will likely be worse off in most of Tennessee. This is especially true for healthy buyers who are very price sensitive. I am assuming that the new entries think that they can price at or below the current very high Silver Benchmark plans offered by BCBS-TN. If they price at the same point as the benchmark plan, there will be no change in relative post-subsidy premiums paid by the individual. Far more likely the new Silver plans will be significantly less expensive than the very high benchmark plan. This means that subsidized buyers in these regions will see lower subsidies and higher post-subsidy premiums. Currently some families can earn well over 200% Federal Poverty Line and qualify for a $0 net of subsidy premium Silver plan. Those families will see higher costs next year assuming the new entries offer at least one Silver plan lower than the current benchmark.

Iowa is a single insurer state for 2018. Medica covers all 99 counties with a single Silver plan. Next year, Wellmark, the local Blue, is re-entering the market. Medica only offered a single Silver plan. There is no chance for someone to benefit from the spread between the least expensive Silver and the benchmark Silver as they are the same thing as Brad Wright and I explained in the Des Moines Register last winter.

Competition always benefits the non-subsidized by at least increasing the possibility space. Competition has specific local impacts depending on the decisions of insurers and their strategies from the previous, low/no competition year. We must be aware of those changes and distinctions.

Silver Gapping in Iowa and Tennessee: 2 Separate talesPost + Comments (2)

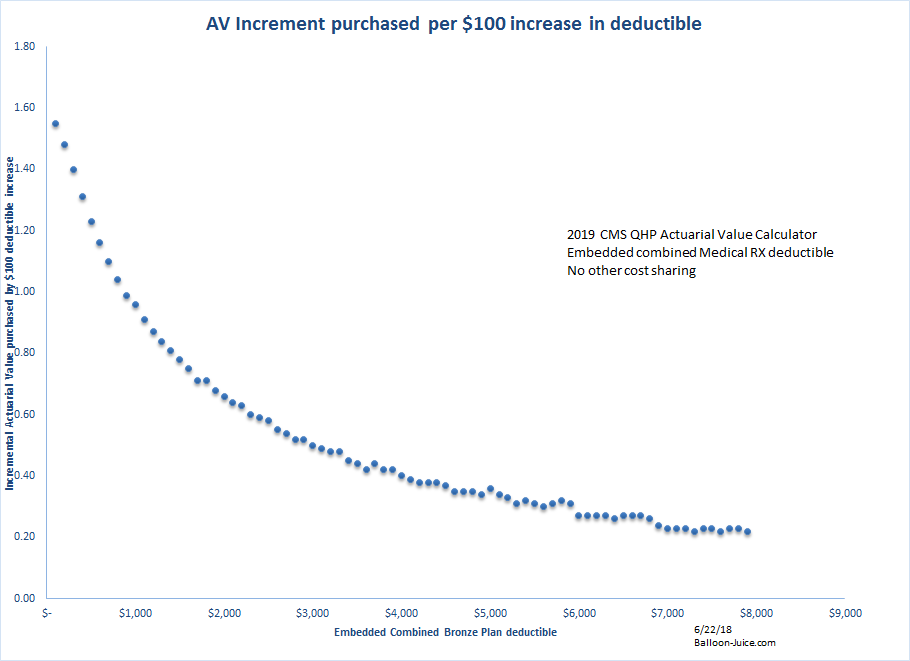

I was curious. What does $100 more in deductible buy in terms of actuarial value?

It depends but the short answer is not much.

The graph below shows how much a $100 increase in deductible buys in terms of actuarial value. I used the 2019 CMS AV calculator with the Bronze tables. Deductible is combined and embedded with no other cost sharing. This is a bare bones plan.

This is because health care costs are so skewed to the right. Half of the population barely touches the system so the first $100 of deductible captures most of their health care spending and the first $500 of deductible is almost entirely their annual spend. The declining marginal purchase of AV per $100 spent on deductible is real and big.

By the time the deductible is going from $3,000 to $3,100, very few people are actually running up charges to that level. It buys half a point of actuarial value for this jump. By the time the last $100 is added to deductible for the skinniest plan possible with a $7,900 out of pocket maximum, the AV bought is .22 points.

The trade-off to buy an extra AV point at the tail end of the distribution is an extra $400 to $500 in deductible. This implies that a Copper plan with a 50% AV could probably see a $12,000 to $13,000 deductible.

An extra $100 deductible does not buy muchPost + Comments (6)

The Kaiser Family Foundation does frequent polling on a wide array of issues. They have a recent poll on politics and they probed a bit on what people actually mean when they say that they are concerned about health care. The key thing was personal costs and not systemic costs:

When asked to say in their own words what specific health care issues they most want to hear the 2018 candidates discuss, health care costs are the top issue mentioned by both Democratic-leaning health care voters (31 percent) and Republican-leaning health care voters (55 percent). The other health care issues vary in importance by partisanship. About one in five (18 percent) of Democratic health care voters say they want to hear candidates discuss universal coverage and about one in ten (11 percent) mention concerns about quality of coverage or care.

This is something that I need to remember as I am focused far more on systemic costs and insurance functionality instead of cost spreading functionality of insurance policies. Most people don’t give a shit that a plan with significant non-preventative services that are pre-deductible is bad insurance that puts significant cost sharing burdens on folks with chronic conditions and one-off catastrophes because most people don’t have a trainwreck of a year. Instead they barely touch the medical system so a $300 claim is a big personal deal or a $1,900 out patient procedure that is mostly going to land on their deductible is a massive expense.

This is just something that I need to keep in mind on the politics and lived experiences of health care financing.

Rate filing season is in full swing. Medica was Iowa’s only ACA insurer for 2018. They asked for a mega rate increase to cover the state and received it. Now they are asking for a much smaller rate increase for 2019.

Last year, Medica said it needed a 57% premium increase – the largest in Iowa history – to remain as the state's sole individual health-insurance carrier. This year, the company is proposing an increase less than one-tenth as big. https://t.co/Q6vcmQH47F

— Tony Leys (@tonyleys) June 20, 2018

What’s going on?

Medica probably overpriced in 2018 is the short story.

Let’s assume that 2018 was appropriately priced. If that is the case, then the following things should be taken into consideration for 2019 rate building.

+5 to +10 points for general medical trend inflation

-2 to -3 points for repeal of the Health Insurance Tax (HIT) for 2019

+10 for repeal of the individual mandate

+ ??? for the proliferation of Farm Bureau and other underwritten plans that should be able to pull good risk out of the ACA pool.

Under that accounting, we’re looking a plausible baseline rate increase of at least twelve points to

twenty or more points. And Medica came in at basically medical trend rates. They overpriced in 2018 because they were a one year monopoly. They overshot their rates and should be very profitable for 2018.

Iowa is seeing the proliferation of Farm Bureau underwritten plans and Wellmark is re-entering the market. Wellmark will have a serious data advantage over Medica. I am still surprised that Medica is planning to stay in Iowa as Wellmark’s ability to legally underwrite via the Farm Bureau makes projecting the remaining guaranteed issue risk pool a high variance exercise:

Wellmark will be effectively granted a de facto monopoly on non-group insurance sales in Iowa. There is currently a single insurer, Medica, offering ACA plans. Wellmark has signalled that it wants to re-enter the ACA market in the state for 2019. Wellmark will be able to strategically offer ACA compliant products that can stick Medica with very high cost individuals without sufficiently high risk adjustment payments to make them whole. At the same time, Wellmark can pick up all of the limited remaining good risk into the underwritten not quite insurance plans while choosing how much and at what price point they want to take on of the remaining highly morbid guaranteed issued pool. Medica has no ability to defend itself or project its exposure. I will be shocked if Medica is still selling policies in Iowa next January.

And here is the repackaged Graham-Cassidy proposal from the Heritage Foundation and Rick Santorum.

TLDR: Don’t get sick

A coalition of conservative groups releases an outline of their Obamacare repeal plan. Presser comes tomorrow.

It tracks with Graham-Cassidy as a grant program. Ends essential health benefits, age ratio and minimum loss ratio. pic.twitter.com/zOqLB3amTd

— Alex Ruoff (@Alexruoff) June 19, 2018

The full plan has not been released yet, but the way that the program is set up is that insurance companies are allowed to underwrite and age rate at whatever level they want. Additionally, eligible individuals can take a per capita allotment to spend as they see fit on health insurance. This is great for the young and statistically likely to be healthy. If you are a 38 year old with Stage 4 cancer (like a friend of mine) taking a $100,000 a year oral chemo that so far is working, good luck as no insurer will cover you and the $241 a month in per-capita allotment is not even enough to be insulting.

So you know what to do: back to the phones and give your Senators and Representatives a piece of your mind.