BREAKING: President Trump says CIA chief Pompeo to become Sec. of State, thanks Tillerson for his service, and elevates Gina Haspel to top CIA post. https://t.co/JqlOHLpp1U pic.twitter.com/AnOuIgyCXZ

— CNBC Now (@CNBCnow) March 13, 2018

Open thread

![]()

Come for the politics, stay for the snark.

I am a student in the doctoral program at the Duke University Department of Population Health Sciences. I am working towards my my doctorate in Health Services Research with a policy focus. I am fundamentally fascinated by insurance markets, consumer choice and the navigation of complex choice environments. I'm currently RA-ing at the Duke Margolis Center for Health Policy.

I used to be Richard Mayhew, a mid-level bureaucrat at UPMC Health Plan. I started writing here and have not found a reason to stop.

Conflicts of interest: Previously employed at UPMC Health Plan until 12/31/16. I also worked full time as a research associate at the Duke University Margolis Center for Health Policy. I have received direct funding from the National Institute for Healthcare Management, and I have been on projects funded by the Rockefeller Foundation, Kate B. Reynolds Charitable Trust, Gordan and Betty Moore Foundation, Duke University Health System, CMMI, and various value based payment consortiums. I serve as a consultant on a grant from the Commonwealth Fund and have acted as a consultant to several ACA insurers.

Research Production is here: https://scholar.google.com/citations?user=zof9b4IAAAAJ&hl=en

David Anderson has been a Balloon Juice writer since 2013.

BREAKING: President Trump says CIA chief Pompeo to become Sec. of State, thanks Tillerson for his service, and elevates Gina Haspel to top CIA post. https://t.co/JqlOHLpp1U pic.twitter.com/AnOuIgyCXZ

— CNBC Now (@CNBCnow) March 13, 2018

Open thread

I’ve been thinking more about the bare county problem and I am not as worried about a state being completely bare but I am very worried about particular counties being bare on a strategic basis.

Let’s imagine that there is a large insurer in a state that is currently mostly bare. That insurer is currently out of the Exchange in most/all of the state. That insurer previously had spent time on the individual market in most of the state. It has covered a significant number of lives in the state through the combination of Exchange, Medicaid, CHIP and employer sponsored insurance. The claims data is not exhaustive but it is big enough, recent enough and clean enough to have a decent signal in it.

There are a few people with persistent million dollar claim years and a population of people with a detectably higher probability of catastrophic claim years in any state. The insurer with deep data has a fairly decent idea of where these people live. Given the risk adjustment system and the limited reinsurance for million dollar claims, the insurer who covers these individuals will not be adequately compensated by risk sharing mechanisms. They will only be able to pay those claims through high premiums.

Some insurers that possess a significant information advantage may look at a bare state and tell the state regulators that they are willing to enter Rating Regions 1, 3, 4, and 5. Rating Region 2 is a black hole of highly likely catastrophic claims and they won’t touch it.

That is the scenario that I think is fairly likely if and when we start seeing bare regions.

Aisling McDonough made a very good point last night:

People should be worried about bare ACA counties in 2019 b/c of GOP sabotage.

Between mandate repeal, short-term plans, health ministries, farm bureaus, etc, the guaranteed $ for the lone ACA insurer is getting smaller. It's not the same calculus as it was in 2017 & 2018.

— Aisling McDonough (@AislingMcDL) March 12, 2018

In 2017 and 2018, the calculus for insurers entering a bare county was that they would have monopoly pricing power which would allow them to choose their own risk pool. High premiums could cushion the risk of the insurer only getting the very sick non-subsidized people in a county while subsidies guaranteed that a reasonably healthy mixture could be attracted below 400% Federal Poverty Level (FPL). There were non-ACA outlets for people but they were fairly restrictive in the health sharing ministries, three month limited duration plans or non-coverage with mandate penalties.

I was never too worried about naked counties because of the logic above. A monopoly insurer should be able to print money as long as their actuaries were vaguely competent.

That might not be the case any more. The outflow channels to year long underwritten plans and no mandate penalty will unpredictably suck out a lot of the good risk in the bare county. The risk pool is going to be very sick for ACA plans. Rural counties are much more likely to have expensive provider contracts so the same person in a rural area will be much more expensive to treat than that person in an urban area where narrow networks are plausible. The big question is how much sicker will the ACA risk pool in potentially bare counties be?

Will they be 20% sicker? Will they be 50% more morbid? Will they be 100% more morbid? This is a huge risk to take for insurers. Some of the last counties to be covered last year had fewer than 1,000 covered lives in them. Insurers don’t like taking big risks for small upsides; it gives them hives. Walking away from bare counties is a viable business strategy especially as there is little political upside to making the ACA work.

Aisling is worried, therefore I am worried.

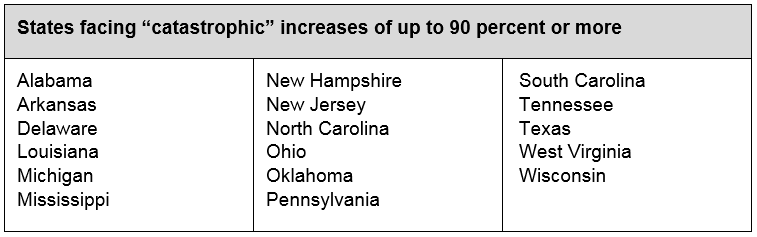

Covered California released an actuarial study on the premium changes for the ACA individual insurance market due to policy changes over the past six months. It is ugly. The premiums will vary greatly by state over the next three years according to this study. I just want to look at the worst states.

Senator Cassidy (R-LA) repeatedly brought up the story of one of his constituents last year. They were a family of four with total earnings in the the six figures. They did not qualify for premium tax credits even as they were spending $40,000 a year in total medical costs. One family member has a chronic, high cost medical condition. This person could never pass underwriting.

This family will face a choice of paying over half their income for premiums by 2021 under the current policy regime or aggressively finding ways to lose enough income to get under 400% FPL to qualify for a premium tax credit that caps their Silver premium expense at less than 10% of their income. Given the much higher premiums, the opportunity cost of financial engineering to qualify for a premium tax credit will go down. Having a family member with an expensive chronic condition under the current policy regime places a huge notch on earnings between 400% and 600% FPL where almost every additional dollar earned would go to either taxes or individual market premiums.

The critical question in any health financing system is how are the people with consistent and known high cost needs treated. Are they left on their own? Are they shunted aside? Are they consigned to a life of poverty? Or is there a system that counter-acts the bad luck that they have so the opportunity space is as broad and deep for them as it is for anyone else.

Right now the health policy proposals floating around Washington for the past year narrows opportunity space for many people

Iowa’s Senate approved a proposal to allow Wellmark and the Iowa Farm Bureau to sell health benefit plans (let’s not call them insurance) on an underwritten and limited benefit basis. The goal is to give healthy people who make too much for strong subsidies cheaper options.

I want to look at the political economy of the play. And for that, we need to look at the single most important chart in US health finance policy. This is the 2015 version from AHRQ:

Think hard about this distribution:

Earlier this week, a pair of papers on opioids came out. One leaned in the direction of my priors (1) and one is making me re-evaluate my priors (2).

The first study is a randomized trial comparing one year outcomes for people in the VA with significant back, knee or hip pain symptoms. One arm received standard opioid therapy while the other arm of the trial received non-opioid pain medication.

Question For patients with moderate to severe chronic back pain or hip or knee osteoarthritis pain despite analgesic use, does opioid medication compared with nonopioid medication result in better pain-related function?

Findings In this randomized clinical trial that included 240 patients, the use of opioid vs nonopioid medication therapy did not result in significantly better pain-related function over 12 months (3.4 vs 3.3 points on an 11-point scale at 12 months, respectively).

A year out, there was no functional, clinical or statistical difference in the treatment arms.

There is a growing body of evidence that opioids are not particulary better pain killers in some common situations than less dangerous alternatives. This is an important but not an amazingly surprising result in this paper. Serious caveats need to be put into place about generalizabilibility but for the relevant population, this is more of a confirmation than a shocking result.

Now the second paper looks at the impact of Naxolone, an overdose counter-acting drug and asks if widespread availability of the drug changes mortality rates?

The Trump Administration released their demands for funding Cost Sharing Reduction (CSR) subsidies. It is either a poison pill list or a complete misreading of leverage. Any CSR deal needs sixty votes in the Senate which means at least nine Democrats need to vote for it and most likely a dozen or more Democratic votes are needed just in the Senate.

Here is the White House memo on the terms they are asking for in exchange for doing anything to bring premiums down for even 1 year.

I will explain the three items below in this thread. 2/ pic.twitter.com/LdqKmpPh5Y

— Andy Slavitt (@ASlavitt) March 7, 2018

The demands for CSR are to enact into law short term plans, restrict female reproductive health care and relever the price band from 3:1 to 5:1**.

There is a deal that could be made in Congress. This is not the deal. CSR funding is not a peculiarly valuable policy outcome for Democrats who are interested in expanding affordable, low out of pocket coverage any more. As I wrote in October:

At least forty states have taken steps to protect all on-Exchange buyers from CSR costs in 2018. The Congressional Budget Office predicts that all states will converge to local regulations that shift the entire cost of CSR to only Silver plans thus lifting the relative price point of the subsidized Benchmark plan…

It is a shift from a narrowly structured, tightly means tested subsidy to a more broadly structured, loosely means tested subsidy. This gives states a lot of flexibility….

These are acceptable long term outcomes for Democrats and liberals. More people get covered. If there are no 1332 waivers, the coverage expansion is expensive and inefficient. If states use 1332 waivers to subsidize off-Exchange individuals with a reinsurance program, more people will get covered and the spending will be more efficient. The transitional year of 2018 will be a scramble but from a political perspective, this is acceptable for Democrats as the public believes that the Republican party should be responsible for health care.

Funding CSR is a massive spending cut on subsidized health insurance. That is a significant policy concession from Democrats in and of itself.

If CSR is not funded, the premium increases that occurred in 2018 will be baked into the baseline premiums for 2019. Those premiums are likely to increase by 15% to 20% or more due to the combination of short term plans and the pragmatic elimination of the individual mandate. Final premiums are announced a few weeks before election day. The headlines of 20% premium increases are far more beneficial to Democratic political chances than headlines that premiums are flat or declined by 2%.

Not doing anything is a viable political and policy option for Democrats. Requiring Democrats to give up even more policy concessions in order for them to give up another policy and political concession just seems convoluted to me.

Now what could an actual deal be?

Trading CSR funding for expanded subsidies or removal of the income cap for subsidies and technical changes on 1332 waivers, outreach, reinsurance and catastrophic plans could make sense. It gives Republicans a political headline, it takes one of the last major pain points of the ACA (the non-subsidization of premiums for families earning over 400% FPL) and it makes the ACA market more stable. It would be a policy for politics trade-off.

An honest examination of leverage and outcome preferences if nothing else happens is a critical analysis to perform.

** On a completely cynical note, a 5:1 age banding is more likely to help Democratic leaning young voters while harming Republican leaning older voters.