From Charles Gaba:

we won’t be offering our Blue Choice PPO insurance plans for our under 65 block of business going forward…..

Currently, we have about 367,000 individual Texas members who will have their PPO plan discontinued in 2016….

Our Blue Advantage® HMO network will remain. We are working to expand the numbers and reach of providers participating in that network.

We only had the first full year of ACA claims data for analysis this year, for 2014 claims. In the individual market segment in 2014, BCBSTX paid out more than $400 million more in claims than it collected in premiums. Losses that high are unsustainable, and we have adjusted our offerings – as many insurers have – to be sustainable in the new market reality.

Why is BCBSTX discontinuing the Blue Choice PPO?

For the past two years, BCBSTX has been the only health insurer offering an individual PPO plan in all Texas markets. BCBSTX found that the PPO is not sustainable at an affordable price due to anti-selection. BCBSTX will continue to offer other plan options in all 254 counties, on and off the Marketplace.

Charles asks a good question

The highlighted question above is the one which I had the most trouble understanding: If HMO enrollees were profitable but PPO enrollees weren’t, why not simply raise the rates on the PPO crowd? I mean, they obviously wouldn’t be happy about it and many might move elsewhere anyway, but wouldn’t that make more sense than dropping the whole PPO line completely.

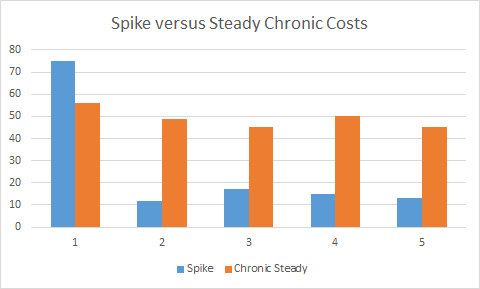

There are a few things going on here from an insurance strategy side. The first is that total claims expense is the product of the number of services billed and the average price per particular service. This the key claims equation and insurers try to do quite a lot of things to minimize one or both components of the equation.