I have never really understood the argument that rate shock would collapse the Obamacare Exchanges (at least as long as the Feds can subsidize all eligible policies). The subsidies are designed to transfer the risk of premium rate increases above the rate of general economic growth to the Federal government and off of the individual. Subsidies are determined as the gap between the second lowest silver and the expected family contribution. The expected family contribution is a function of income as a percentage of Federal Poverty Line so that someone at 101% FPL is expected to contribute 2% of their income for the premium of the 2nd Silver and someone at 399.99% FPL is expected to contribute 9.5% of their income for the premium of a second Silver. If the price of the 2nd Silver doubles, the contribution stays constant. If the price of a 2nd Silver drops in half, the maximum family contribution stays constant. Subsidized buyers are insulated from price changes.

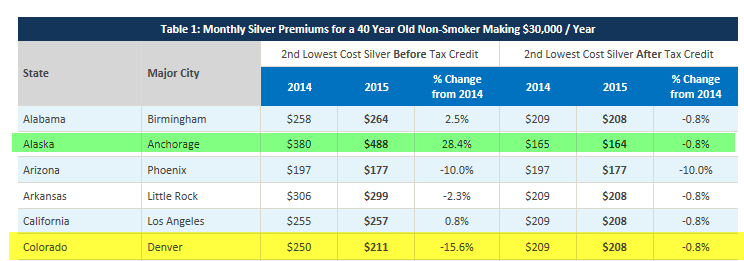

Kaiser has a good chart that I’ve snipped a part that shows this argument:\

Alaska saw a 28% increase in 2nd Silver prices for 2015. The post-subsidy cost for the example decreased by a dollar. Coloardo saw a 15% decline in price for the 2nd Silver. The post-subsidy cost also declined a dollar. The dollar decline is due to inflation bumping up the poverty level brackets slightly so $30,000 in 2014 supports a slightly higher family contribution than $30,000 in 2015.

Arizona is an interesting case. In both years, the example policy holder is not getting subsidy as the 2nd Silver cost is below the maximum family contribution. In this case, the Arizonan saves $20 a month due to increaed competition if they switch policies to chase the lower premiums.

There are two major advantages to this program design. The first is that it provides predictability and security for individuals who make under 400% FPL. Their premiums will only increase as their purchasing power increases due to either more income or fewer dependents in the house. Secondly, and I think more importantly, it transfers pricing risk from atomized individuals who can’t do much about it to a big powerful entity (the Federal government) that can do something about pricing that is getting out of control. What that something is in this political climate is nothing but future political climates, a big buyer who can throw its weight around can get a good deal.

NCSteve

One of the real holes in Obamacare that we will never fix as long as Republicans keep hold of forty seats in the Senate is that if you lose your insurance and a third of your income because you’re over fifty and your old employer decides it is cheaper to toss you over the side and replace you with someone young and cheap after an appropriate waiting period (depending on whether the headcount is above the ADEA threshold), you can end up still way above 400% of the poverty line, but with the expenses you have accumulated at 52 based on the illusion of income security. And those expenses are much higher than they were the last time you made that salary and your insurance costs more because you’re 52.

I’m not exactly unique in being in this position. Fifty somethings are the real, and apparently permanent victims of the Great Recession. Fifty two is the new seventy-two as far as most employers are concerned and millions of them have been left looking for lower-paying jobs to eke out the years between now and (if they’re super lucky, relatively speaking) the age they can tap retirement savings and, if they’re unlucky, the age they shake off this mortal coil.

I’m grateful to be able to get silver-grade coverage period, because it would have been effectively impossible before the ACA. And, at 52, you need more than a bare-bones bronze policy because well, shit happens after 50. A lot. But the reality is that I’m going to be paying 9.2% of my gross for good but not great coverage because I don’t qualify for subsidies and you can only dial back your expenses so far. If something fortuitous doesn’t happen, sometime next spring I will be having to choose between selling my house and once again becoming an apartment dweller or giving up health insurance. Theoretically, I can do that because I’m pretty sure I’m exempt from the mandate, but I can’t give up health insurance because I’m 52 and shit happens after 50. A lot.

There are worse choices to have to make in this world. I mean, I’ve got decent equity, I bought it at the bottom of the market and houses have been turning within a couple of weeks in my neighborhood. The truth is I’ll be able to afford a pretty dang nice apartment as apartments go (much nicer than any house I could afford) and FSM knows, there are many who would kill to trade my problems for theirs. But losing your home, well it’s a bitter choice to contemplate nonetheless.

Julia Grey

Why is my son’s premium going up so much, then? Is it because we’re in a non-Medicare state? He’s barely at the 138% line, so he can get a subsidy on the exchange, which reduced his premium on a very good policy to $75 a month last year, and apparently also helped with the deductible and co-pays.

We just got a letter saying that if he wants to keep this policy, he will be paying $125 a month starting in January. That’s a 67% increase.

He’s technically a self-employed construction worker, and luckily he will not drop into the no-care no-Medicaid zone with his income this year, which will be about the same, but one bad stretch in the construction business, and he’s out of luck.

Mnemosyne

@Julia Grey:

He should go onto the exchanges and look for a new policy. The insurance companies haven’t exactly been honest and forthcoming in their communications with their customers. I remember that last year before the exchanges open, some insurance companies here in California sent letters to their existing customers that said that Obamacare forced them to put everyone on a high-premium Gold plan. Not surprisingly, it was total bullshit, but it panicked a lot of people.

NCSteve

@Julia Grey: Like the prior commenter said. If you have an exchange policy, you need to shop for new coverage every year rather than renew the plan you have. If an insurer prices a plan based on actuarial assumptions that turn out to be wrong, they’re going to jack up the price next time to try to get everyone to leave it. Odds are, however, there’s another plan–and probably from the same insurer–that either guessed better or even one making the same mistake.