Rep. Frank Pallone (D-NJ) is a Congressman to watch if one is interested in health policy. He is the chairman of the House Energy and Commerce committee. This is a key healthcare committee. He introduced HR 5155 last Congress that was a pragmatic set of tweaks and fixed to the Affordable Care Act. His bill is an off-tackle run that is seeking to advance the football without trying to score an eighty three yard touchdown on a single touch. I think a bill like this will be seen as a “minimal 10 day fix” bill if there is a Democratic trifecta in 2021 and that trifecta decides to spend its effort and time on another domain and wants to get a medium sized healthcare bill out during lull times.

One of the sections is the removal of the 400% FPL cap on premium tax credits.

This solves the ACA cliff problem. Someone making 399% FPL has a very strong incentive to not earn another dollar as that dollar could cost them thousands or tens of thousands of dollars in premium subsidies depending on location, age and family size. Cliffs are usually a BAD THING (TM) in public policy.

A side effect of this proposal or any other proposal that removes the subsidy cap is that it makes the Catastrophic plans pointless. This is not a big deal as Catastrophic plans have never been more than a small part of the risk pool. They are a specialized plan which have fascinated me.

Catastrophic plans are currently available to anyone who is younger than age 30 or who has a hardship exemption. A common hardship exemption is that there is no “affordable” coverage available to an individual. “Affordable” means an insurance plan was offered for less than 8.16 percent of income in 2017. In 2019, an additional hardship exemption will broaden catastrophic eligibility as people who live in single insurer counties will automatically qualify for a hardship exemption. Catastrophic plans are not eligible for premium tax credits, which means that buyers pay the full premium without assistance from the federal government.

Catastrophic plans in 2019 have slightly lower actuarial value in comparison with bronze plans. The deducible is set at the maximum allowed out-of-pocket limit ($7,900 in 2019), and after that all costs are covered. Three primary care visits are excluded from the deductible. Currently, catastrophic plans are risk adjusted only against other catastrophic plans.

They have a non-subsidized pricing advantage over Bronze only because they are not in the shared risk adjustment pool.

If there is universal subsidization, then their pricing advantage is highly likely to disappear. Subsidies change the relevant premium numbers for buyers from the price level to the price spreads. Silver gapping matters to catastrophic buyers.

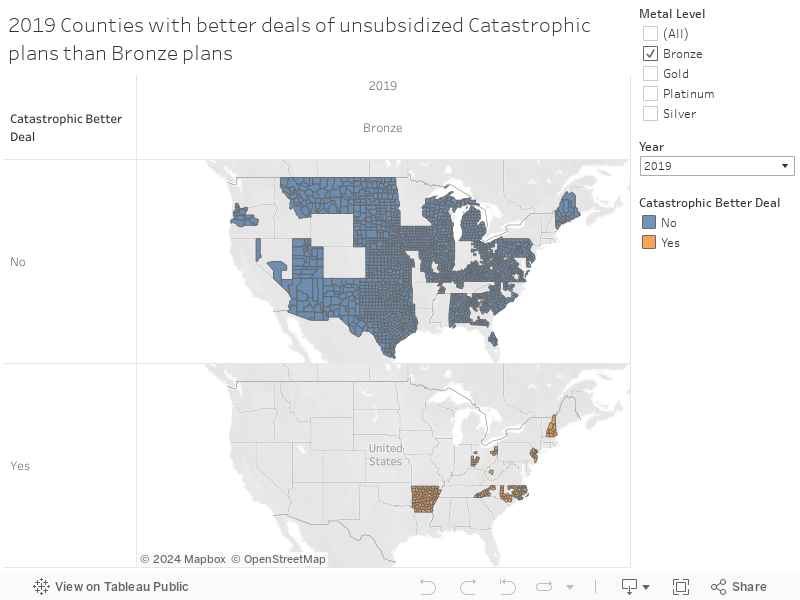

Right now, catastrophic plans don’t receive subsidies. They have similar benefit and actuarial value as Bronze plans. If subsidies are applied to all, then almost all counties where an insurer sells a Catastrophic plan on Healthcare.gov will have at least one Bronze plan that is cheaper (net of subsidies) for a single forty year old.

91% of counties on Healthcare.gov have at least a Bronze plan that is cheaper, net of subsidies than the cheapest Catastrophic plan for single 40 year olds. Some counties (mainly Oklahoma) have Gold plans that would be cheaper, net of subsidies, than the cheapest available Catastrophic plan under the Pallone scheme.

I’m having a hard time seeing how Catastrophic plans make any sense in a plausible future legal environment that extends subsidies up the income ladder. The only population that may see better deals are a very small sliver of 20 to 29 year olds or people earning high six figures in counties where there is a very tightly compressed premium spread.

On the Road and In Your Backyard

On the Road and In Your Backyard

L85NJGT

This is a highly likely outcome. There is a lot of low hanging fruit in ACA tweaking that won’t require political self immolation.

taumaturgo

Peoples lives continue to hang in the balance while the politicos continue to accept bribes from the health industry in order to protect the status quo. Pay more, get less. Don’t befall to an accident or sickness for you may die broke. Is this really the best we can do? Are there any other examples in our known universe of how to make health care a right for the common folks, that is less expensive and delivers better results? Must we really accept the middlemen of big pharma and insurance companies lining their pockets while we convalesce and die?

Rufus Firefly

In a political environment leading to such a trifecta, any Democrat who takes that approach is going to be caught in a crossfire with credible primary opponents from the left and hard right ones in the general plus voters voting 3rd party or not at all— and rightfully so. The zealots of the GOP have used this tactic effectively to get the politicians they think they want; maybe it’s time for the left to come of the bench.

Another Scott

It’s good that they’re figuring out a way to get rid of the cliff. As you say, cliffs are bad.

But 8.5% of MAGI is a lot of money for people who have no savings. Roughly 40% of adults don’t have enough savings to cover an unexpected $400 expense.

Yes, tweak the ACA and get rid of easy-to-fix problems like these. But we need to do much more.

Cheers,

Scott.

Fair Economist

I agree filling in the cliff is a really obvious, and politically easy, fix. Any other changes you think would be really easy wins like that?

Brachiator

This sounds very reasonable. But I wonder how many people might simply and foolishly do without rather than look for a subsidized plan. Assuming, of course, that any bill could get passed and approved.

The GOP still indulges in dishonesty despite clear anger from their own voters. I wonder if the midterms might make them a little more likely to make a bipartisan deal.

Also, doesn’t eliminating the cliff make this fix more expensive?

tobie

This sounds like a good fix and I imagine that there are a number of other fixes that a Democratic majority in Congress and a Democrat in the White House could implement easily and painlessly. Last I checked only 5% of the population purchased health insurance on the exchanges. If we can ever get a full-scale Medicaid expansion nationwide, that number should decrease even more.

Dorothy A. Winsor

The dental hygienist and I were talking about the Oscars this morning, and I said I’d seen only “Black Panther” and “Vice.” She said, “I just love Dick Cheney. I’m a huge fan.” I had no idea what to say since I’ve never met a Cheney fan before. She said she admired how he managed things after 9/11 and loved how smart and competent he is. I still don’t know what to say.

StringOnAStick

@Dorothy A. Winsor: I’m a dental hygienist, and I have to say that dentistry is in general pretty politically conservative. it’s pretty shocking that she went so political in her conversation with you since that’s typically verboten (unless the dentist is also RW too). I never lead the conversation that direction, and only talk about these things if the patient insists; my boss is pretty liberal though and I’m sometimes shocked at what he and a patient he knows well will say to each other, plus secretly very gratified. Most dental offices are places I simply could not stand working because the boss is a winger, and usually with a toxic work environment with extra sexism sauce.

A few years ago my nice liberal DDS boss bought out the practice next door when that DDS had to quit for health reasons. That was a very RW office but my boss gets along with everyone so he hired some of the employees who would have lost their jobs. One was a male hygienist who loves, loves, loves FOX. One day I heard him ranting about how bad unions are to a patient, and then the patient very quietly and firmly stated that “I belong to a union and my union protects my rights as an employee, and I think unions are very important to preserving good paying jobs”; the rest of their time together was very quiet and a bit tense. I really wished at the time that the patient had complained to the boss, but this guy quit soon thereafter and I picked up his hours. Every employee we got from that office turned out to be crap at their job and are no longer with us, and most of the patients are gone too because they were used to and expected crappy, low cost/low quality work plus since that office was never busy they expected to be able to call and get same day appointments for hygiene care. We keep growing in patient population and it takes easily 3-4 months to get back into the hygiene schedule because we’re so booked with loyal patients.

Moral of the story: liberal or even D leaning dentists are rare in such a conservative field, but they can be found. When you find one, tell all your friends and ask them to patronize that practice. If the hygienist is yakking outside her lane, most offices have a website where you can leave comments and complaints, often anonymously.

Dorothy A. Winsor

@StringOnAStick: That’s really interesting. I love the patient who stood up for his union.

ProfDamatu

Removing that subsidy cap would be huge!

One thing that I wonder, @David Anderson or anyone else, really – What kind of fixes might potentially be possible for the fact that, just due to the structure of the law, ACA insurance plans have to get worse and worse every year? By which I mean that OOP maximums and cost sharing have to rise every year, otherwise you have metal tier creep. The reason I’m mulling this over is that we’re rapidly approaching (or have passed?) a point where, for many people with chronic illnesses, it’s becoming financially unfeasible to budget for the expenses, even with insurance. Where I live, for example, the lowest OOP maximum is the approximately $6500 required for plans eligible for HSAs; all the others are at the statutory max. If you’re making, say $40,000 a year, and you need enough chronic illness care to hit your max every year…well, right now you’re looking at spending close to 30% of your income on medical expenses (premiums plus cost sharing), and that’s only going to get worse.

I guess I’m wondering if there is any feasible fix for this, and, as an ancillary matter – are there even enough people in this boat for politicians to care about fixing it? (“People in this boat” would be people covered under ACA plans who have a chronic illness, but are well enough to work and have a salary above the CSR cutoff, but below the subsidy cliff.)