Two of my dissertation aims are “Silverloading” aims. Aim A will look at a state policy on how that state Silverloads and how that changes enrollment at various income levels. Aim B will look at the same state and check out the policy’s impact on market functionality.

One of the challenges I have this week as I am writing my proposal is explaining both Silverloading and how to identify Silverloading through administrative data to my committee. They are all wicked smart but they don’t breathe and dream ACA data and policy like I do.

So I’m writing my initial thoughts here….

Silverloading is an insurer response to the October 2017 policy change that ended direct federal reimbursement to insurers. These direct payments reimbursed insurers for the direct costs of providing mandatory Cost Sharing Reduction (CSR) subsidy benefits. CSR benefits are provided to enrollees with incomes between 100-250% FPL who purchased on-Exchange Silver Plans. Insurers that Silverload starting in Plan Year 2018 placed the incremental cost of these CSR benefits into the premium of Silver plans and only Silver plans.

Does this make sense?

Now how do we identify Silverloading in administrative data? I have to demonstrate that this is a real thing. I propose to look at the ratio of premium between each insurer in each county in each year between their lowest premium gold plan and their lowest premium silver plan. I had thought about doing the same for bronze to silver but bronze plans don’t have to be offered (that is a good follow-on paper in the future extending on Ko and Fang) while silver and gold have to be offered. Cheapest plan is the plan I am picking as that is the likely possibility frontier.

Non-Silverload state-years will have Gold be priced substantially more expensive than Silver. Silverload will have Gold priced near or below Silver.

Let’s show a few examples!

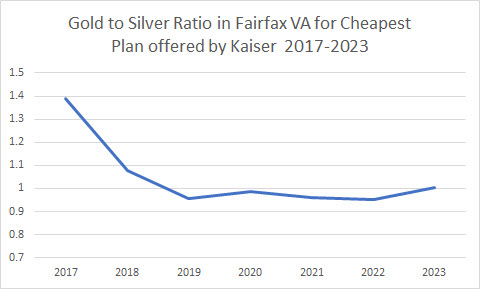

The first is a clean example of Silverloading from Virginia. Virginia had a general Silverload go into effect in 2018.

We see a huge drop in the Gold to Silver premium ratio from about 1.4 in 2017 to about 1 in 2018. This is what we expect. Gold got comparatively way cheaper.

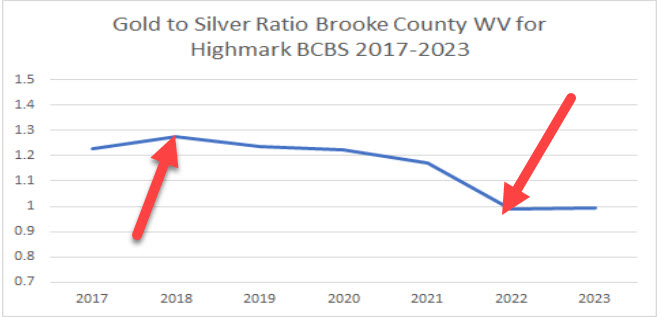

Now let’s look at West Virginia. The state had a different policy regime than Virginia from 2018-2021. Both states had direct federal reimbursement of CSR benefits in 2017. But West Virginia adopted a “Broadload” to pay for CSR benefits where the cost of those benefits were placed into the premiums of all metal levels. If this measure if sensitive to the changing policy regimes, we should see the Gold to Silver ratio to be roughly constant-ish during the Broadload period. In 2022, West Virginia allowed insurers to Silverload. We should expect a big drop in the Gold to Silver ratio. Now do we?

Damn!

It is obvious that there was policy regime change from 2021 to 2022. The Gold to Silver ratio collapses.

I think this is a pretty decent identification of the policy regime for my dissertation.

<b> Update </b> More geeky stuff below the fold

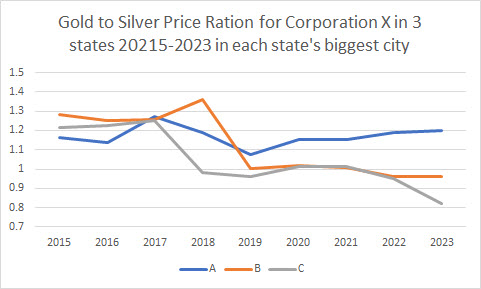

This is the gold-silver ratio for one insurer that operates in multiple states including the state of interest. It is in the county of each state’s largest city. I don’t have raw parallel trends. Giving my subject matter expertise I can tell you what happened in City B in 2018 but the committee and Reviewer #2 will need more than “Dave knows why this is funky because he wrote about it on Balloon Juice years ago….”

I think as soon as I throw in a reasonable set of control variables (cough cough Medicaid Expansion!) I probably will have the conditional trends that the preferred analysis will need. I probably have 40,000 to 50,000 more year-county-insurer combinations of data to throw at this problem instead of the 27 observations that I’m graphing here. If not, I’ll learn all about synthetic controls. JOY!

Old School

Do you want a line chart or a bar chart? A bar chart might make the drop more pronounced.

bbleh

Yay! (And committees love them some real-world data that support one’s Very Clever Ideas. You probably got at least one signature right there.)

And since you appear to have invited nitpicking:

Silverloading is an insurer response to the October 2017 policy change that ended direct federal reimbursement to insurers for the direct costs of providing mandatory Cost Sharing Reduction (CSR) subsidy benefits to individual market enrollees who purchased on-Exchange Silver Plans and

whohad incomes between 100-250% FPL. Insurers that Silverload starting in Plan Year 2018 placed the incremental cost of these CSR benefits into the premiums of Silver plans and only Silver plans.And if there’s any way to break that first sentence in two, I would, eg, “… that ended certain federal payments to insurers. Those payments reimbursed insurers for …” But YMMV.

Will STFU upon request.

David Anderson

@bbleh: that is a much better read.

Thank you!

David Anderson

@Old School: Probably a bar or a dot chart once I throw the data into STATA but quick and dirty in Excel is fine for Balloon-Juice

Fake Irishman

Balloon Juice is now serving as a preprint server/trial registry.

This place really is a dessert topping AND a floor wax.

Is Cole going to start charging his front pagers article processing fees?

Good luck! This sounds like an appropriately focused topic for a chapter.

narya

How are you defining “market functionality”?

David Anderson

@narya: Number of insurers, number of plans offered by each insurer, benefit structure in Gold plans to determine if the insurers are attempting to screen or select for certain populations (building on work by Chenyuan Liu in her job market paper https://chenyuanliu.github.io/files/DesignSorting_ChenyuanLiu.pdf)

My hypothesis for Aim B is that the policy juices certain categories of enrollment (Aim A) but it does so in a way that makes insurers more reluctant to enroll less healthy folks in higher actuarial value plans…

schwhatever

Are you sure silver didn’t comparatively catch-up?

David Anderson

@schwhatever: I care about the differences in premiums as this drives affordability for subsidized buyers. You’re raising a good point about absolute price levels. That drives affordability for folks who don’t get subsidies (see Anderson, Drake, Abraham 2019 Exhibit 2 for a good description of the relationship on affordability) https://www.healthaffairs.org/doi/full/10.1377/hlthaff.2019.00917

dnfree

I can see why you don’t have time to referee soccer anymore.