Milliman has a good paper on the actuarial impacts of Essential Health Benefits(EHB) with actual pricing attached to some of the benefits. Every health plan in 2017 that is offered on Healthcare.gov pays at least 89% of their claims dollars for EHB. The overwhelming majority pay more than 99% of their claims dollars to EHB.

First, here is a good illustration of the relative importance of each category of benefit:

New @millimanhealth paper: “Are essential health benefits here to stay?” https://t.co/KRjuEbZGUx pic.twitter.com/9tOKRQKLVW

— Paul Houchens (@PaulHouchens) March 20, 2017

As you can see, doctor visits (ambulatory patient services), hospitals, presriptions, labs and phyical rehab make up the overwhelming majority of the spending on EHBs. There is not a lot of fat in there unless we allow people to buy “not cancer” policies with specific, high cost disease exclusions. Now let’s look at one of the vulnerable EHB, maternity care:

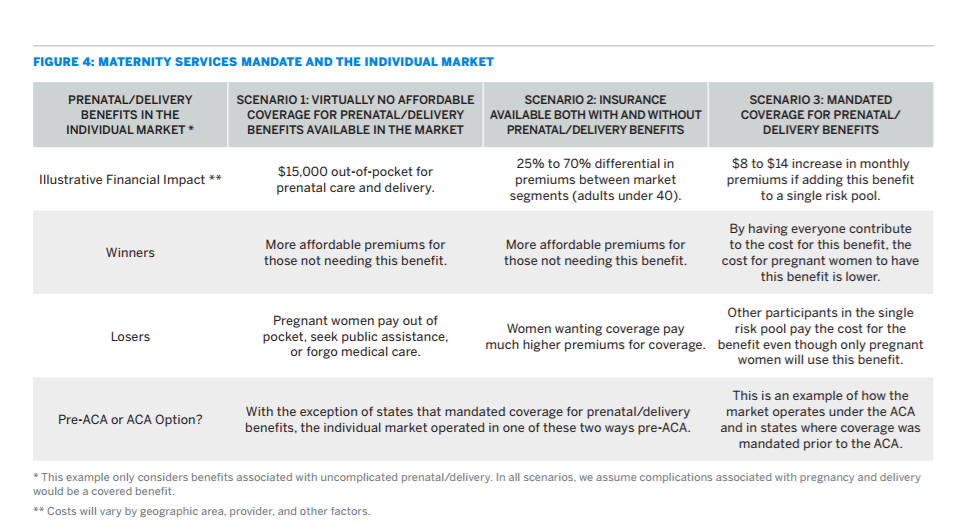

Rolling maternity benefits up into the standard benefit package raises everyone’s rates by the price of a single entree at Olive Garden every month. Splitting the benefit out as an optional benefit makes men better off and concentrates all of the pain on women either through higher premiums and or higher out of pocket limits. The reasonable second order effect is that Medicaid will take on a lot more births that it covers.

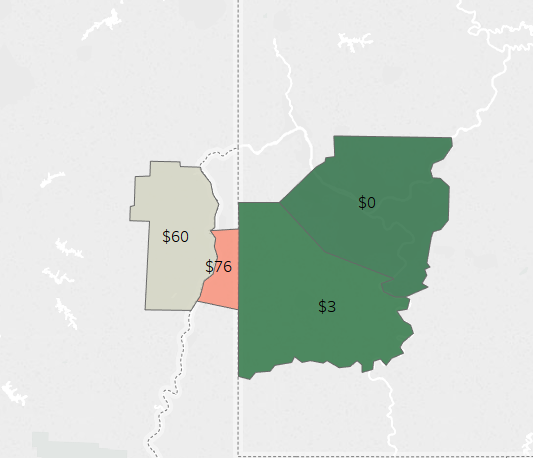

There is only money in the EHB’s and the main EHB’s are fairly well protected in my opinion. So the EHB’s that are not well protected (maternity, mental health, child dental/vision) just don’t have a lot of money attached to them.