Zachary Tracer at Bloomberg recently reported on Oscar’s first quarter results. They are mixed. They are only losing $25 million dollars this quarter instead of almost $50 million dollars.

The privately held health insurer, created to sell plans under the Affordable Care Act, lost $25.8 million across three states in the first three months of this year, compared with a loss of $48.5 million a year earlier, according to regulatory filings Tuesday. The company is beginning to get a handle on its medical costs, as the premiums it collected exceeded what it spent on health services…

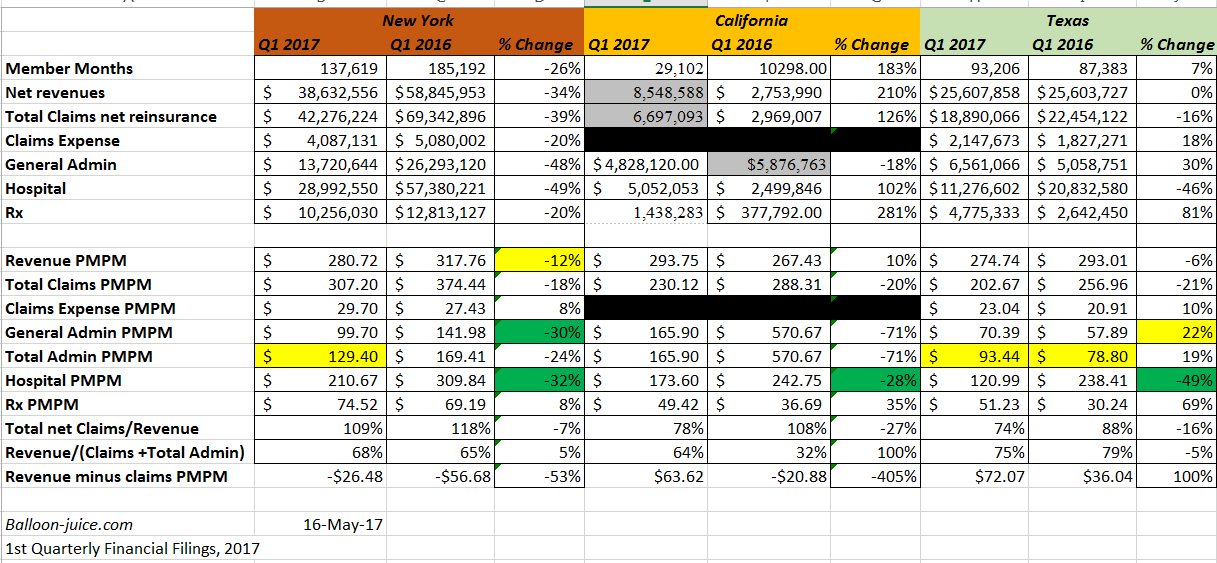

The company’s membership fell this year to 90,171 people as of March 31 from 106,000 across the three states a year earlier, weighing on revenue. The decision to exit markets including New Jersey and part of Texas also slowed growth. Here are the company’s results in its three states:…

Let’s look at what the financials are telling us. All are first quarter 2016 and 2017 with my own calculations.

The overall picture is still Meh. But looking deeper there are two distinct stories. Texas is a pretty good story for Oscar.

Texas is a story where I can see the combination of a narrow network with lower provider rates and increasingly effective admin cost control leads to at least break-even in Q1 2018.

Oscar Texas seems to have their hospital expense under control. Their MLR is under 100% so their premiums are contributing to the actual cost of running the plan. The admin expense is still high and it increased to $93 per member per month (PMPM). A $93 PMPM admin implies a premium of $465 PMPM for an 80% Medical Loss ratio. Their current premium supports an admin cost of $59 PMPM at 80% MLR. Admin has to come down. I would be very curious as to what is going on with their pharmacy expenses as well.

California is still a start up market. Their story is closer to to Texas than New York’s story, but it is too early and too small to say much.

New York now is still scarily unimpressive. Revenue does not cover claims. It is improving but Oscar is still giving away medical care at a loss and has been for four years in a market where they should have some ability to stabilize. They have adapted a narrow network strategy that their Comms Director claims is truly unique (I’m not convinced) where they get lower rates and more data control. But their cost per hospitalization is still extraordinarily high at $195,000/hospital admission (Q7) despite having slightly fewer days per hospitalization than Texas.

The good news for Oscar New York is their hospitalization PMPM and admin PMPM are decreasing but the bad news is their admin PMPM is still ungodly high.

Furthermore, there is something very interesting in the trend in revenue per member. It went down in New York and Texas. This is odd as Oscar asked for and received significant premium hikes for 2017.

Last summer Oscar received approval to increase their premiums by roughly 20% in New York state.

Oscar Health, the insurance startup and Silicon Valley darling, and Independent Health Benefits Corporation, will have individual rates increase by about 20 percent, also in line with what they had requested.

So the sticker price went up but PMPM revenue went down. How could this happen?

There are two mechanical points that could do this. They could be independent or operate in conjunction. The first is the average age of Oscar buyers went down dramatically. A 21 year old replacing a 45 year old would produce this type of effect given a 20% index rate premium hike. This could explain part of the story in Texas but not in New York. New York has strict community rating with no age banding.

The other mechanical solution is to drop actuarial value. This makes a good deal of sense. As I mentioned in March, Oscar is shifting its membership composition towards an off-exchange strategy. An off-exchange member is more likely to buy a lower actuarial value plan. Andrew Sprung estimated off-Exchange actuarial value at just under 69% while, Kaiser Family Foundation estimated that the actuarial value of plans sold off Exchange is just under 66%. On-Exchange actuarial value from these two sources is approximately 79%.

Why does this matter?

A younger population on lower actuarial value plans means very high risk adjustment outflows. Oscar New York already was sending 25% of revenue out the door for risk adjustment. That number will probably increase. If Oscar projects the increased risk adjustment outflow right, they’ll be fine but this could be a source of surprise for them.

Overall, I still don’t see anything special in what Oscar is doing. Their best story is still a money losing with a reasonable probability of near term profitability story. Their story in the market they have been in the longest still has incredibly high administrative costs and an MLR over 100%. All of this is after moving towards a lower cost and narrower network.

Q1 New York financials are linked here:

Q1 Texas filings are linked here:

Steve in the ATL

I have nothing substantive to say about this post, but I didn’t want David to feel unloved!

sheila in nc

So risk adjustment means, if I’m an insurance company with older/sicker patients, I get help, but if I’m an insurance company with younger/healthier patients, I have to pay extra? Is this a feature of the ACA? Does it continue under the various AHCA proposals? And how does it relate to the CSR issue?

Sorry to be dense, just trying to make sense of it all.

David Anderson

@sheila in nc:

Sheila — that’s about right on how risk adjustment works. There are a couple more twists and turns but the idea is solid.

AHCA does not spell out what risk adjustment applies, to whom, and how. No one knows.

ed

Ok, I’m hoping this is close to topic: Obamacare Helped Americans Detect Cancer Earlier