ACA open enrollment is starting at the end of the week. The 2020 Open Enrollment Period will be one with more choices than the past couple of years with significant premuium swings. There are no major changes in outreach activities budgeted for by Healthcare.gov. The advertising and navigation budget is very low but not too different from their 2019 Open Enrollment Period budget. Beyond insurer entry and exit and plans being terminated and created, the big source of variation will be in the post-subsidy premiums. Subsidized buyers, and more importantly, the marginal subsidized buyer who is flipping a coin as to whether or not they will be covered next year, are primarily concerned about the premium that they pay every month and little else. This means that they care about the spread between the cheapest plan available to them and the benchmark plan. This is the “Silver Gap” game I’ve been talking about for years now.

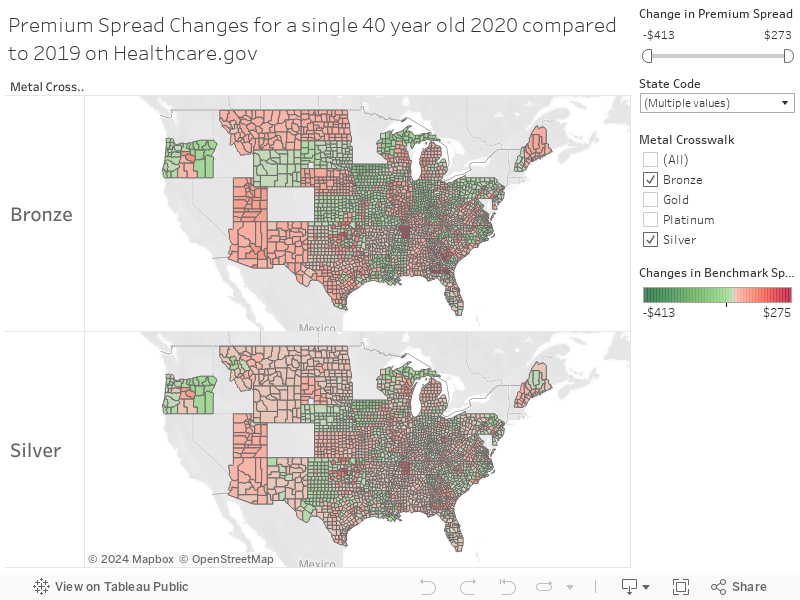

There is significant variation. The maps below show the difference in premium spreads between the cheapest Bronze and Silver plans to the county benchmark for 2019 and 2020. Green shows that a county has a cheaper net of subsidy plan now available in 2020. Red shows that the premium spread has shrunk and therefore the cheapest subsidized plan in that metal level for that county is now more expensive net of subsidy. Bronze plans will be the cheapest plans, while silver plans will have high Cost Sharing Reduction (CSR) enhancements added which makes these the overwhelmingly dominant choice for people earning between 100-200 percent of the Federal Poverty Level (FPL).

All else being equal, we should expect to see enrollment overperformance in northern Iowa, Oregon, the Upper Pennisula of Michigan. We should expect to see enrollment underperformance in parts of Oklahoma, most of Utah, Appalachian Kentucky, Western Tennessee, Southern Ohio, the coast of Wisconsin among other areas. These are rough directional estimates. There are twelve counties in Oklahoma that have seen their bronze to benchmark gap be reduced by over $150 for a single forty year old. That would, naively, lead to expectations that enrollment for healthy individuals earning over 200% FPL would crash. However the 2020 bronze to benchmark spread is still large enough to make a zero premium plan available.

However, as a first rule of thumb, big changes in premium spreads between the cheapest plans and the cheapest silver plans relative to benchmark will give us a good intuition as to which counties will see significant changes in enrollment for 2020.

Testifying Today – Lieutenant Colonel Alexander Vindman

Testifying Today – Lieutenant Colonel Alexander Vindman

Butch

The Upper Peninsula (where I live) will once again have the “choice” of one provider, Blue Cross of Michigan, and I’ve already received a notice that the premium for our Bronze plan is going up. I’m going to investigate catastrophic coverage since BCBS finds an excuse to deny everything that’s submitted anyway.

stinger

We want to see the T-shirt!

Raven

My insurance posts never seem to get any response here but what the hell! My official retirement date was October 1 and on the 15th I got two messages telling me that as of the 1st my wife was no longer covered. We have a system where I get a subsidy for Medicare supplement and my pre65 spouse stays on the regular system health care until she reaches 65 the she gets the subsidy as well. None of my HR folks have ever seen this happen and I finally got her on a plan

David Anderson

@Raven: Congratulations on retiring. If there is anything I can do to help, e-mail me at the Balloon-Juice e-mail.

taumaturgo

M4A is past due and it is the most sensible answer. Speaking about answers, I saw an excellent suggestion as an excellent answer for Warren to answer the fake deficits hawks “how are you going to pay for it?”

…”How can Elizabeth Warren address the major savings workers can win by shifting to Medicare for All? My friend Steve Tarzynski, who’s president of the California Physicians Alliance, suggests something like the following:

Right now, you and your family pay $18,000 a year in premiums for employer-sponsored insurance that doesn’t even cover everything and that you could lose at any time. Plus another $2,000 in deductibles before it even kicks in and another $1,000 in co-pays. That’s about $21,000 every year for a basically defective product. That’s the “private tax” you’re paying right now. And your choice of doctor is restricted and you can even lose access to your doctor at any time. All that would go away with Medicare for All—no more premiums, no more deductibles, and no more co-pays. And all the care you and your family need will be covered and can never be taken away. You can choose any doctor you want. Yes. You’ll pay $5,000 more in taxes for all of that. But it will put $16,000 back in your pocket. And it doesn’t even include the share of the premium that your employer pays now that you could get back in wages and salary. Would you settle for that?

And to my fellow Democrats on the stage here who oppose Medicare for All, who are you really working for? Because what you propose is exactly what the insurance industry wants.”

David Anderson

@taumaturgo: Please see what Sen. Simena said this morning on the filibuster. Best case scenario for 2021 is that whatever Senator Manchin wants is what will pass.

Ohio Mom

One thing that has occurred to me in my current Medicare research is that for many years, as I acquired one preexisting condition after another (don’t worry, they are very amenable to treatment), I looked forward to turning 65.

Then I would never have to worry about losing any coverage for any reason. I could have a big sigh of relief.

Now of course, the ACA has taken away worries about coverage for pre-existing conditions (even though we still have to worry that this guarantee will be revoked). It makes slogging through the fine print about Medicare a little less sweet.

I know the slogan, “MedicAID for All” wouldn’t get any traction, but that is what Ohio Son has and it is pretty hassle-free fee-for-service for him, in our particular circumstances (I am well aware that isn’t true for everyone on Ohio MedicAID). I’d like to have something similar.

West TN guy

Thank you David for explaining exactly why here in West Tennessee that the “bronze” plans are not being fully covered by the tax subsidy in 2020. As a healthy guy in his 40’s, it was okay to have the crappy aca policy when it was fully subsidized but there is no way I’m paying out of my pocket for this high deductible junk. Bye-bye ACA!!!!