The ACA plan offerings and premiums have been released.

Window-shopping has started on Healthcare.gov.

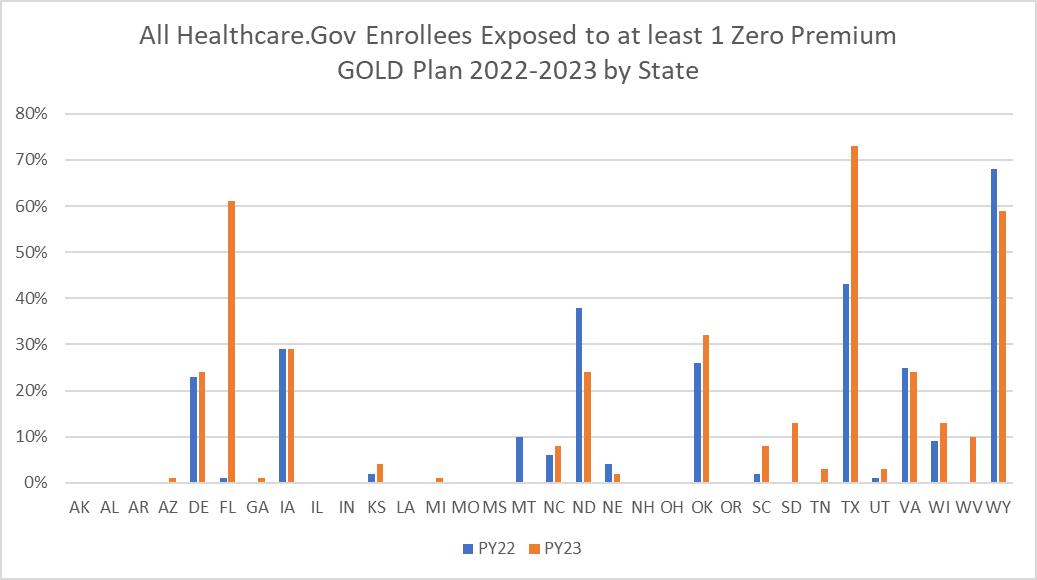

Texas is having a massive affordability shock as most current enrollees in the state will now be exposed to a zero premium GOLD plan. Texas changed state law on how they priced Silverloading so Gold and Bronze plans became comparatively less expensive relative to Silver.

Now not everyone should want to be in Gold. People earning under 150% Federal Poverty Level (FPL) qualify for zero premium plans with massively less cost-sharing. People earning between 151% and 200% FPL can buy Silver plans with less cost-sharing and a bit more premium than a zero premium Gold plan. At this income level it is a risk-reward trade-off that is a matter of individual preferences.

Over 200% FPL, Gold likely dominates Silver where Gold from the same insurer on the same network has both lower premiums and less cost-sharing than the comparable Silver plan. Dominated plan choice is inefficient and expensive to the consumer. There can be softer/weaker superiority scenarios where most elements of Gold are better than Silver where the decision gets fuzzier again.

My co-authors and I have always looked at this problem from a consumer angle. People pay more to get less. That is bad.

We also need to think about this from the federal perspective. If a dominant plan is zero premium for a given individual but that individual is either automatically re-enrolled or actively chooses the dominated plan, there is “excess premium subsidy” from “metal tier selection.” In the case where the dominant plan is zero premium, but the federal government is subsidizing the dominated plan, the federal government is spending a lot of extra money to buy an objectively inferior product.

That is bad.

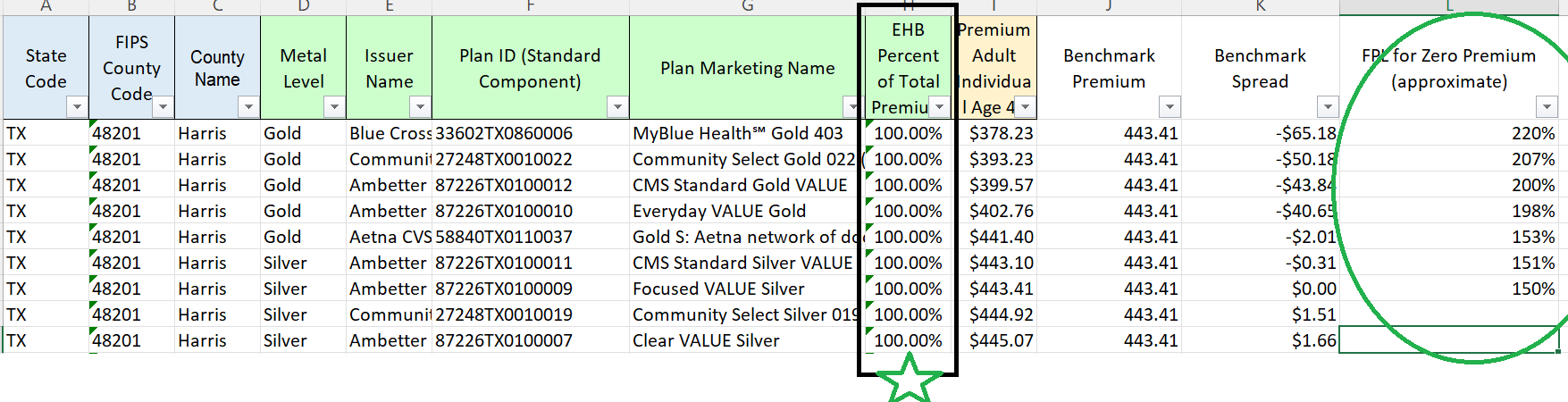

Let’s take an example from the Houston market for 2023. Our target individual earns 202% FPL and are enrolled in 2022 Community Health Plans Community Select Silver plan.

Under the current automatic re-enrollment system, they would be defaulted to plan ID 27248TX00100019 which is the same plan that they chose from last year. They would pay a premium of $49/month if they do nothing for a plan with a $3500 deductible and a $7200 out of pocket max. The federal government pays a subsidy of $396 per month for this plan.

If the default is to place people in zero premium plans with higher AV than the current year plan from the same insurer with the same network, this individual would be placed in the Gold plan with plan ID 27248TX00100022. This plan for this person has a $0 premium. It has $2200 deductible and a $9100 out of pocket max so this is not strict domination as the Silver CSR 73 plan has a lower OOP but under most spending scenarios, Gold is better than Silver. The federal government would only pay $393/month in subsidy for this plan. The individual saves $49/month and the feds save $3 a month for the default.

In a static simulation, improved plan defaults to higher AV but zero premium plans likely saves the federal government money. In a dynamic scenario where we assume zero premium plans reduce administrative friction and thus increase enrollment duration and retention, total federal spending may not decrease. But this should be investigated.

Betsy

It’s really good work you are doing. I hope they listen to you!

Gin & Tonic

This is kinda OT, but now that we’re in Medicare open enrollment and every second TV ad is about that, I’m left wondering how private insurers can offer what appear to be better benefits for the same or sometimes less money, while still making a profit. Is there some form of cream-skimming going on, where only the people with more expensive needs stay on Federal Medicare? This does not seem viable in the long term.

Ohio Mom

@Gin & Tonic: They cheat. A few days ago, the NYT had an article on this: ‘The Cash Monster Was Insatiable’: How Insurers Exploited Medicare for Billions

Advantage plans are basically HMOs, with limited numbers of doctors in their networks. That works if you are relatively healthy but as you age and collect medical conditions, you might want to see specialists who aren’t in your plan. The catch is, if you want to switch to traditional Medicare. you may not be able to find a Gap plan which will underwrite you and your pre-existing conditions, at least not at a rate you can afford.

David Anderson

@Gin & Tonic: tomorrow I will reply to a great question

Gin & Tonic

@David Anderson: I look forward to it. I have decisions to make.

Ohio Mom

From https://www.ehealthinsurance.com/medicare/enrollment/can-i-switch-from-medicare-advantage-to-medigap/

“Once you’ve left your Medicare Advantage plan and enrolled in Original Medicare, you are generally eligible to apply for a Medicare Supplement insurance plan. Note, however, that in most cases, when you switch from Medicare Advantage to Original Medicare, you lose your “guaranteed-issue” rights for Medigap. You generally have guaranteed-issue rights for six months when you are both 65 or older and enrolled in Medicare Part B. Guaranteed-issue rights ensure that you can buy any plan sold in your state, and that you won’t be charged higher premiums based on your health status.

Without guaranteed-issue rights, your insurance company may require medical underwriting before it sells you a plan. During medical underwriting, the insurer looks at your past medical history and current health status. If the company determines the risk of covering you is too high, it can refuse to sell you the plan you want, or it may charge you much higher premiums for the coverage.”

frosty

@Ohio Mom: Medicare Advantage (HMO as you said) doesn’t work at all if you live in one state and all your doctors are across the state line in another one, which is what happened to us when we moved just over the Mason-Dixon line 20 years ago. We went with Medigap.

It also doesn’t work too well if you travel a lot. We’ve needed Urgent Care at least once on all of our road trips. We could probably have gotten out of network coverage but it would have involved more work than walking in the front door.

@Gin & Tonic: Re: decisions to make. It took me a month of going back and forth with my primary care to figure out that Medicare Advantage wouldn’t work. I never got a straight answer from the office or corporate whether I could get covered O-O-N and I finally just gave up. I’m happy with the Medigap we signed up for.

AliceBlue

When I was first eligible for Medicare, I attended a seminar for new enrollees. The thing I most remember is the guy telling us over and over “DO NOT GET MEDICARE ADVANTAGE.”

Kristine

Two different advisors, including a friend who handled benefits for a college, advised signing up for trad Medicare instead of Advantage (I know there are some situations where that isn’t possible). I heard a few horror stories about people being unable to seek treatment at leading hospitals that weren’t in their Advantage policy’s network unless they picked up the tab themselves.

To me, Advantage just means a continuation of the usual insurance company bs. Even with offerings of dental, vision, and health club coverage-which I am sure all have exceptions hardwired–it’s not worth it.

Almost Retired

I’m glad I’m not in Texas (a statement I can make in many circumstances).

Because of a gap between our retirement and reaching Medicare age, my wife and I signed up for the ACA through Covered California, selecting a PPO bronze plan. It was all very simple and well-explained, although it was hard to see why anyone in reasonably good health would sign up for the more expensive Silver plans unless they were getting a hefty subsidy. At any rate, it was surprisingly affordable and a better deal than COBRA. Blue State soshulizm at its finest.

Gin & Tonic

@frosty: I appreciate this and the other responses. I’m in a slightly different situation, though, as I am eligible for both “traditional” Medigap and a new Medicare Advantage plan through my former employer, which takes care of its retirees very well. The Advantage plan they offer is BC/BS, which seems to have a very wide network of providers.

Lobo

To tackle this problem would it be helpful to have an “out of pocket” number to help with comparing. People often fixate on premiums, but out of pocket can move them from anchoring on that. For example, for any offering there would be three pieces of info involving average out-of-pocket expenses.

What can be used to turn an apples to oranges comparison to a type of comparison of a citrus to another type of citrus understanding apples to apples is not possible.