Earlier this week, I noted that the ACA risk adjustment program is highly likely to overpay for Hep-C anti-viral prescriptions this year and next year due to list price reduction shocks. The price that insurers pay will be significantly below the prices used to determine risk-adjustment co-efficients.

We had briefly talked about a great NBER paper by Geruso, Layton and Prinz in June 2017 about how risk adjustment and reinsurance mostly worked on the ACA to remove cherry picking incentives. My thought when I read the paper was that this was a profit-making opportunity for positive risk screening for certain small groups of drugs:

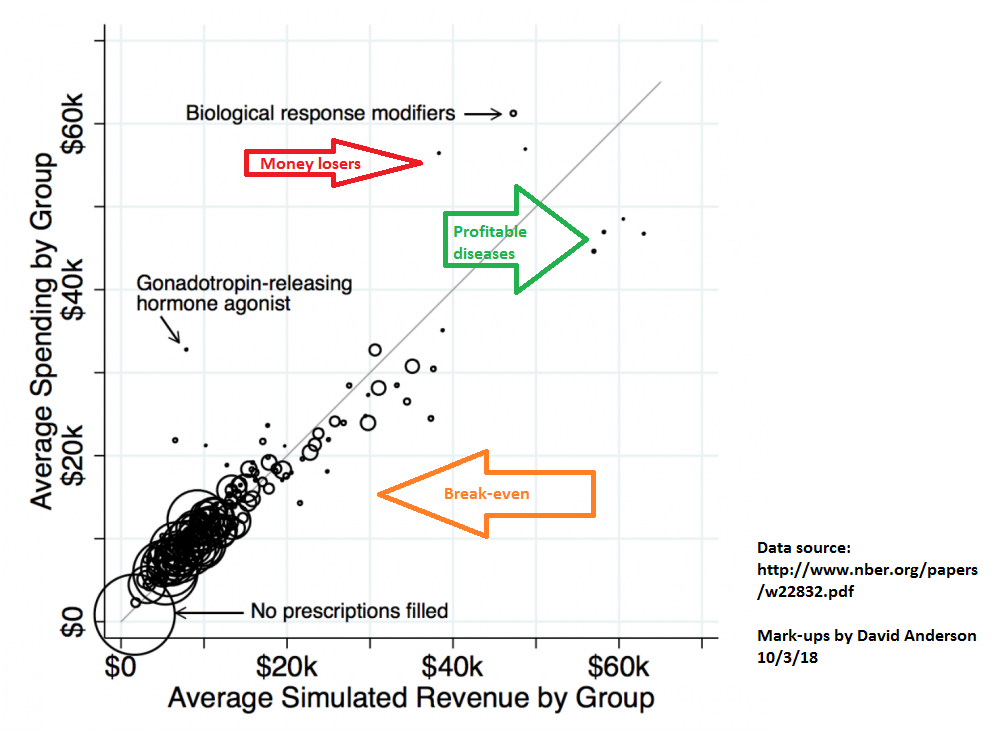

I had my cynical bastard insurance company plumber hat on as I looked at that graph. There are several drugs in that lead to a total cost of treatment between $45,000 and $50,000 but bring in between $55,000 and $65,000 in revenue. They are the massive beneficiaries of risk adjustment.

My big operational question is whether or not insurers were actively designing formularies to attract these patients?

I want to repost a slightly modified version of the graph that I referenced in order to talk a bit more about this idea of attracting profitable risk:

Every circle near the gray line is risk adjustment and reinsurance working close enough to right; total net incremental revenue is close enough to total net incremental costs. The dots that are noticably above the gray lines are risk adjustment and reinsurance problems where total net incremental revenue is significantly below total net incremental costs. The dots below the gray line and near the green arrow are profitable drug classes as the net revenue (premiums plus reinsurance plus risk adjustment) is significantly more than the incremental costs of care.

Every circle near the gray line is risk adjustment and reinsurance working close enough to right; total net incremental revenue is close enough to total net incremental costs. The dots that are noticably above the gray lines are risk adjustment and reinsurance problems where total net incremental revenue is significantly below total net incremental costs. The dots below the gray line and near the green arrow are profitable drug classes as the net revenue (premiums plus reinsurance plus risk adjustment) is significantly more than the incremental costs of care.

I think that the ACA risk adjustment formula with the currently lagged data is moving Hep-C cures into this group for a couple of years. Insurers should have strong incentives to make it very easy for anyone that they cover in the ACA individual market to get easy access to the Hep-C cures as it will be very profitable for the insurers to do so. I think one of the first tests that we should expect to see will be if there is a drop in tiering and pre-authorization requirements for at least one of the drugs in the Hep-C anti-virals therapeautic class. If that is the case, then we can probably infer that an insurer is more willing to pay-out on Hep-C risk.

p.a.

Do insurers have people watching? i.e. “drug x is coming up on 20 years, any knowledge/rumor of a generic in the pipeline, and can we prep a plan to gain formulary advantage for a few years?”

Are there any advantages to this process for less expensive drugs that for whatever reason provide a similar formulary gap? ‘Volume’ drugs (Say widely prescribed but small price difference vs big gap low demand drugs (the hemophilia exception for example))

PAM Dirac

Seems like this would be a very good thing. Was this something that was seen as a possible secondary effect of the way the risk adjustment scheme was designed? In general, I would suspect that discontinuous changes in cost/benefit for a particular treatment would take a while to be incorporated into treatment decisions and providing financial incentives to speed up the adjustment could be very useful. Does the same mechanism provide disincentives for treatments where the cost/benefit gets worse?

David Anderson

@p.a.: There are numerous people who watch both the trials pipeline and the generic approval pipeline. As to what insurers do with that knowledge for risk adjustment purposes is up in the air.

David Anderson

@PAM Dirac: To your last question first — yes, treatments that have high cost and low incremental revenue from risk adjustment or reinsurance tend to be placed on more expensive tiers (higher co-pays etc) or have more arduous pre-authorization hoops to jump through.

I don’t think that this is an intended design effect but that is pure speculation on my part. I agree with you that in this particular use case, it is probably a good thing on first order although secondary incentive challenges remain.

Naive Bayesian

Interesting to see significant across-the-board gaps between the risk adjuster cost estimate and actual expected costs for insurers on these items. Back in 2012/2013 I was part of a project to help a client determine the marketing profile of individuals with higher-than-average federal risk adjuster scores that our client insurer could treat at below the estimated cost (iirc they were especially effective at helping people manage diabetes, for example).

It’s been a while since I’ve been in the actuarial space now, but I honestly expected to hear more about stuff like this where insurers had real incentives to grab individuals with conditions they could treat at below the expected cost, either where the risk adjuster appears to overstate the cost in general, as here, or where particular insurers had deals with providers or other systems in place to treat specific conditions cheaply relative to the market.

swiftfox

I’ve done a fair amount of reading on GnRH use to suppress contraception in deer. Doesn’t work well in free-ranging deer populations so I’m not surprised it is a money-loser.

Bob Hertz

David, I know this sounds naïve, but if insurers have risk adjustment programs with this level of detail and support, why have so many left the ACA market? Why have so many come in with severaly narrow networks, all the better to avoid problem patients? thanks