In the ACA market, there are four metal bands of increasing actuarial value(AV); bronze plans pay about 60% of claims through premiums, silver pays about 70%, gold pays about 80% and the rare platinum plans pay about 90%. There are also three common variants of silver for cost sharing reduction (CSR) subsidies where people earning between 100-250% Federal Poverty Level (FPL) and who buy a silver plan see the insurer pay 73%, 87% or 94% of claims through premium dollars.

CSR-87 and CSR-94 plans squeeze the Platinum 90% AV. They are similar, as platinum plans are allowed to be between 86% to 92% AV while a CSR 87 is actually anywhere from 86% to 88% and a CSR 94 is between 93% and 95% AV. Structurally all of these plans are similar. This similarity has led the Center for Medicare and Medicaid Services (CMS) to allow insurers to use the Platinum experience tables to design these three plan variants. Insurers have to submit their benefit designs to CMS and have the acaturial value land within the target zone outlined above. CMS provides insurers an expected utilization table that is partially built from individual market experience and partially built from other private, commercial contracts.

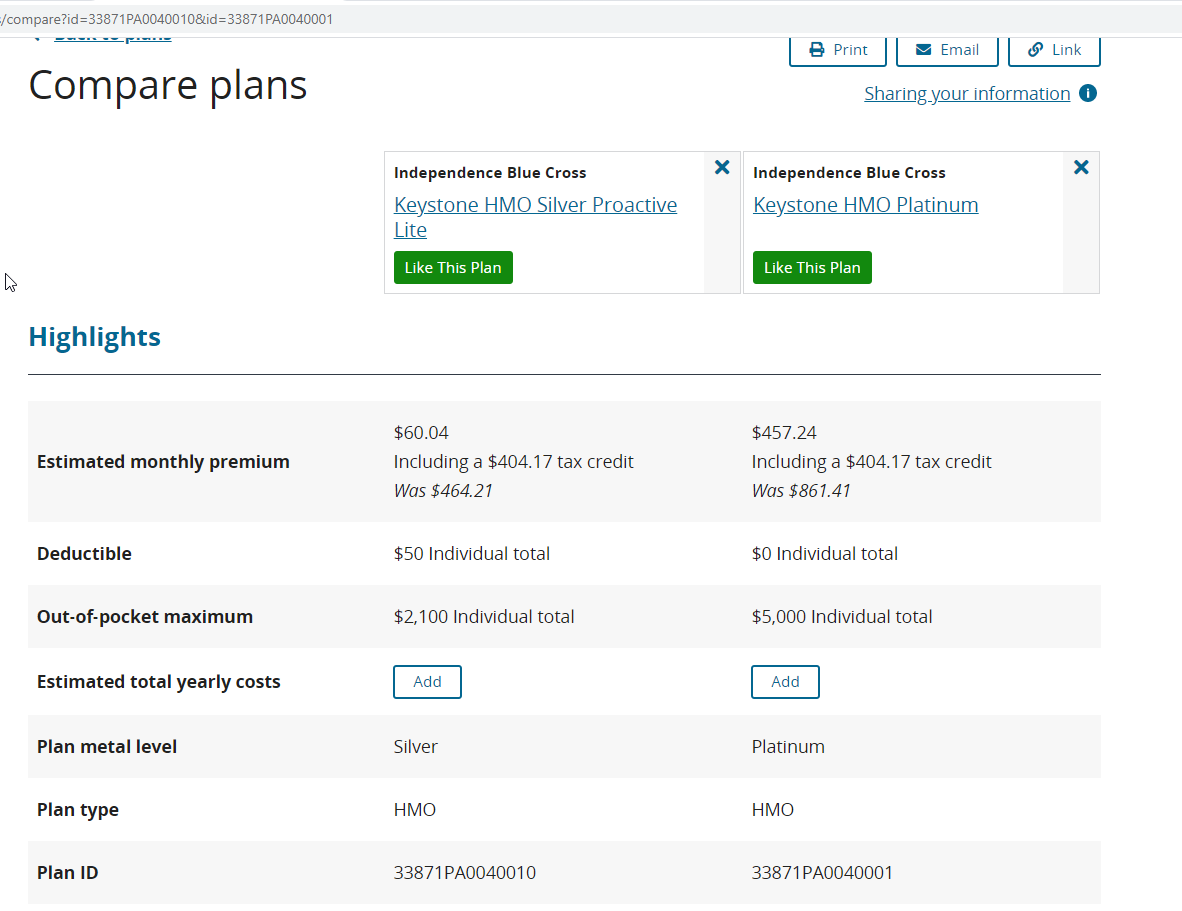

The platinum table is built mostly on the claims experience of individuals with higher incomes. The picture below is the premium and benefit structure of a single 40 year old living in Philadelphia and earning $18,000:

Someone earning $18,000 per year will not buy a platinum plan when a CSR-94 plan is both cheaper and higher actuarial value. This Philadelphia platinum plan would have a premium, net of subsidy, of 30% of annual, pre-tax income while the superior plan has a premium of 4% of income. The platinum plan is grossly dominated by the CSR-94 plan for someone making $18,000 while in some circumstances it is a better plan for someone making more than $50,000 and therefore subsidy ineligible.

The point of cost sharing is to either merely to shift costs onto the sick or to create enough pain to deter low value care or make people try cheaper options first. A $500 out of pocket charge for someone making $18,000 per year is 2.7% of annual income while that same charge for someone making $50,000 per year is 1% of income. A basic precept of economic analysis is that the marginal utility of a dollar decreases as income goes up. A $500 expense is way easier for someone earning $50,000/year to bear than it is for someone earning $18,000.

$500 worth of cost sharing could conceivably have very different behavioral effects for someone who is CSR-87 or CSR-94 qualified compared to someone who is buying a non-dominated platinum plan.

CMS currently uses the same experience tables to design plans for two very different populations. I suspect that the actual deterrant value of increased cost sharing for access to care is significantly higher for the CSR eligible silver buying population than it is for the platinum population. If my inkling is right, then the cost sharing for CSR variants for people earning under 200% FPL may be too high. The solution would be for CMS to generate a CSR variant utilization table using only ACA individual market data for either the 2022 or 2023 plan years.

* For my own sake, I needed to write something that was not COVID related at least once this week.

Starfish

I am excited that someone is talking about this. When people are talking about failures of the ACA, this is exactly what they are talking about. We need to do better by the people who cannot afford both their monthly payments and their cost-sharing.

Jerry

Are you able to quantify your inkling to prove it? Is that something that can even *be* quantified?

Bodacious

Oh man! I used to follow your posts like a hound, and then life got crazier with a new job that had fantastic benefits. Time was just too short to read everything. NOW, I’ve got my life back and suddenly all this stuff is so much more critical to my next 5 years (and beyond). So, I guess on this rainy day I will be going back on your posts and try to catch up! At the last point of ACA research, all plans were so geographically restrictive that I wondered if we were to be prisoners of our own town. With no insurance coverage (beyond life saving) beyond 20 miles of my door, life looked pretty cloistered.

Oh well, I’m back and ready to absorb your words. Thanks for doing this!!!

David Anderson

@Jerry: It is quantifiable.

I would need a state’s claim database and probably 6-12 months of dedicated research time plus a few good co-authors.

I will be circulating this through my networks over the next year to see if I can assemble a team and funding.

Jerry

This would be really important to know. I’m sure your inkling is correct, so we should start pushing our elected officials to act accordingly.

ProfDamatu

It’s great to know that there are dedicated people working on these issues! I confess, though, to a certain amount of frustration. As a scientist, I completely understand the necessity of compiling thorough data and doing the analysis; however, there’s a loud voice in my head screaming, “We don’t need a detailed study to know that a $3,000 deductible and $8,150 OOP maximum is *way too high* for someone making $40,000 per year to afford!” Well, it might be okay if insurance were truly only used for the hit by a meteor scenario, but in a world where ongoing monitoring and chronic condition care amount to a meteor’s worth of expenses (if you’re below median income) every year….not so much.

Apologies for going off-topic; I know the subject here was the narrow issue of how much cost-sharing is too much for those receiving CSR subsidies, but being a selfish jerk, I always like to try to raise the issue of cost-sharing for those who are too “rich” to get CSR subsidies, but who nevertheless are not “rich” enough to actually afford the cost-sharing required from most plans on offer. Several years ago, it was almost do-able; you could get a Silver or even Gold plan with a deductible around $2k and OOP max of maybe $3500-$4k (still too much, but not outright impossible to swing), but thanks to metal tier creep, not anymore.

David Anderson

@ProfDamatu: I COMPLETELY AGREE ON ALL POINTS YOU MAKE

Within the context of what can be done within the context of technocratic tinkering, that is where this effort lies.

ProfDamatu

@David Anderson: Totally get it! :-)

Bob Hertz

If the 40 year old in your sample is male, healthy, and makes too much for a signficant ACA subsidy, they are going to recoil in horror at a monthly premium of $861 for an HMO plan.

Not your fault, but this is a perfect illustration of where guaranteed issue will get you.