The Cost Sharing Reduction Sword of Damocles hanging over the Exchanges for 2017. If CSR blows up in before December 2017, the Exchanges are destroyed for 2017. However if insurers assume that CSR will not be paid in 2018, they might have a very strange incentive set that hacks the exchanges in the direction of the 2009 House bill.

I’ve gone back and forth with a couple of experts on plan pricing. One of them does not believe my ramblings is plausible while another thinks it would be an interesting legal question. This is rank speculation as I am not a lawyer. It is based on p.8 of the 2017 Universal Rate Review Template:

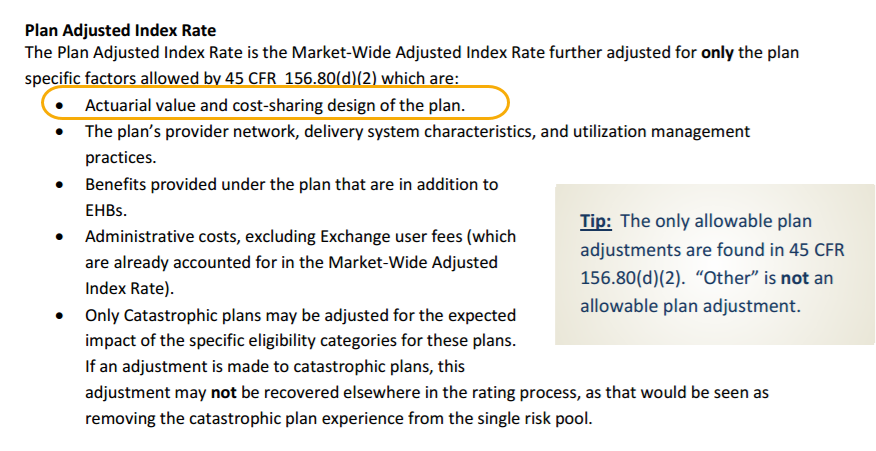

The circled section allows for different pricing due to de minimas variation in actuarial value within a band. All else being equal, a Silver plan at 68% AV should have a lower premium than a Silver plan with a 72% AV.

And here is the possibility of a CSR repricing. If a carrier assumes that they are still to be obligated to offer CSR compliant plans but that they are not to receive CSR subsidies for those plans, they have to price the cost of CSR into their Silver plans. This would be a significant increase in premium as estimated by Kaiser.

If ACA cost-sharing subsidy payments end, insurers would have to raise marketplace premiums for silver plans by 19%.https://t.co/LR4GkIkjvB pic.twitter.com/rfNgFGkuX5

— Larry Levitt (@larry_levitt) April 6, 2017

Effectively, the average actuarial value of the Silver band would go from 70% to somewhere in the mid-80s. Now this is where my completely uninformed speculation comes into play:

CSR non-payment and a silly Silver Gap ideaPost + Comments (11)