Some problems have no good solutions as the rest of today’s blog-wall will illustrate. But one of the minor problems in post-racial America (my ass) is how do health insurance policies on the federal Healthcare.Gov exchange get auto-renewed.

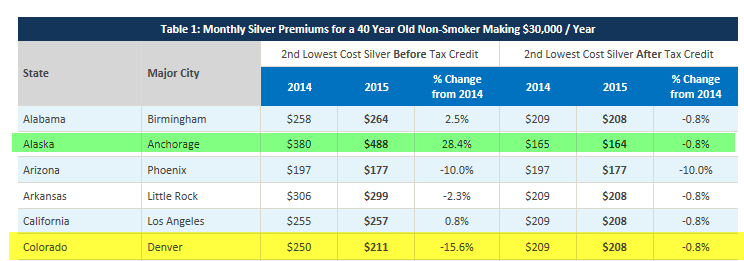

Right now the auto-renewal feature is that on December 15th, any one who has a still active 2014 policy and has not selected a 2015 policy will be auto-renewed. The hierarchy of automated choices is the same policy by the same company, then a similar policy by the same company. This is a good 80% solution, but there are plenty of obvious hang-ups. The biggest problem is that the same policy in 2014 will have a dramatically different subsidy most of the time in 2015. Subsidies are calculated by the difference between a family’s expected income as related to the federal poverty line as that produces the expected family contribution, and the price of the second least expensive Silver plan in the market. The gap is the subsidy amount.

The second Silver plan has often changed between 2014 and 2015. The second big problem is that this process assumes no change in income or family size for the 2015 subsidy calculation. That is an unreasonable assumption. Auto-renewed policies will be giving people wildly divergent subsidy amounts. People will be over-paying, and people will be underpaying and the under-payers will get hit with a big tax bill in 2016.

As Adrianna McIntyre fears, this is a significant political problem:

Consumer tendency toward inertia could mean that a lot of subsidized enrollees could see unexpected premium hikes that only materialize when subsidies are reconciled. It’s the reason you’ve (hopefully) read that exchange beneficiaries should shop around during open enrollment…..

Call me a skeptic, but I’m hard-pressed to believe two-thirds of exchange enrollees fully understand the volatile nature of subsidies and want to keep their current plans anyway.

And yes, I worry about political blowback, too. Not only is the underlying problem difficult to explain, it’s also likely to be an unhappy surprise for affected enrollees. For some, that will happen during open enrollment (when there’s still an opportunity to change plans); for others, this issue won’t become clear until taxes are filed. The assumptions implicit in auto-renewal—that an enrollee’s income hasn’t changed, and that she’s entitled to the same level of subsidy

There is no good way of making a universal default decision. The optimal situation is for everyone who has a current policy from Healthcare.gov to go back into the system and make a new choice after they updated their family and income situations. But that will not happen, so then choices have to be made, and negative trade-offs will be incurred. I’ll outline some of the other options and their trade-offs.